Advertisement

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:2360

Best Mart 360 Holdings (HKG:2360) Is Paying Out A Larger Dividend Than Last Year

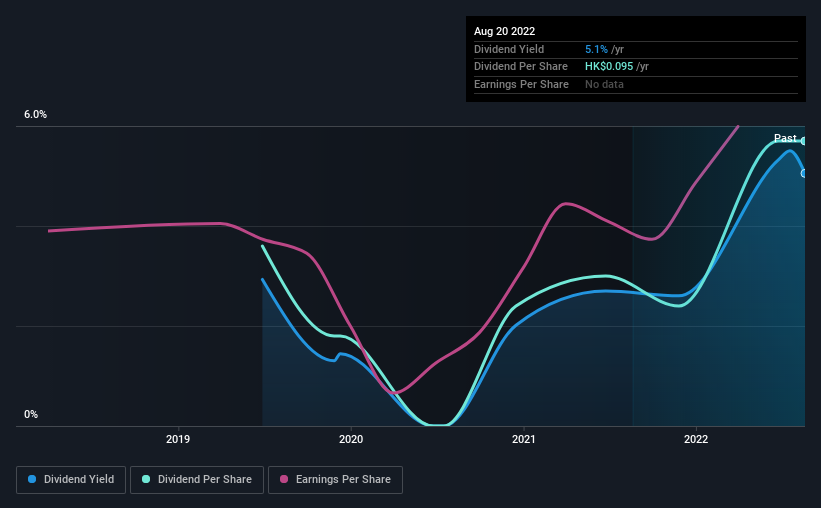

Best Mart 360 Holdings Limited's (HKG:2360) dividend will be increasing from last year's payment of the same period to HK$0.08 on 7th of September. This will take the annual payment to 5.1% of the stock price, which is above what most companies in the industry pay.

Check out our latest analysis for Best Mart 360 Holdings

Best Mart 360 Holdings' Earnings Easily Cover The Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Prior to this announcement, Best Mart 360 Holdings' dividend made up quite a large proportion of earnings but only 36% of free cash flows. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

Earnings per share could rise by 13.9% over the next year if things go the same way as they have for the last few years. If the dividend continues along recent trends, we estimate the payout ratio could reach 76%, which is on the higher side, but certainly still feasible.

Best Mart 360 Holdings' Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. The annual payment during the last 3 years was HK$0.06 in 2019, and the most recent fiscal year payment was HK$0.095. This works out to be a compound annual growth rate (CAGR) of approximately 17% a year over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Best Mart 360 Holdings' Dividend Might Lack Growth

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. It's encouraging to see that Best Mart 360 Holdings has been growing its earnings per share at 14% a year over the past three years. Recently, the company has been able to grow earnings at a decent rate, but with the payout ratio on the higher end we don't think the dividend has many prospects for growth.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for Best Mart 360 Holdings that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Best Mart 360 Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2360

Best Mart 360 Holdings

An investment holding company, engages in leisure food retailing by operating chain retail stores under Best Mart 360 and FoodVille brands in Hong Kong, Macau, and the People’s Republic of China.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor