Advertisement

- Hong Kong

- /

- Consumer Durables

- /

- SEHK:1412

Is Q P Group Holdings Limited's (HKG:1412) P/E Ratio Really That Good?

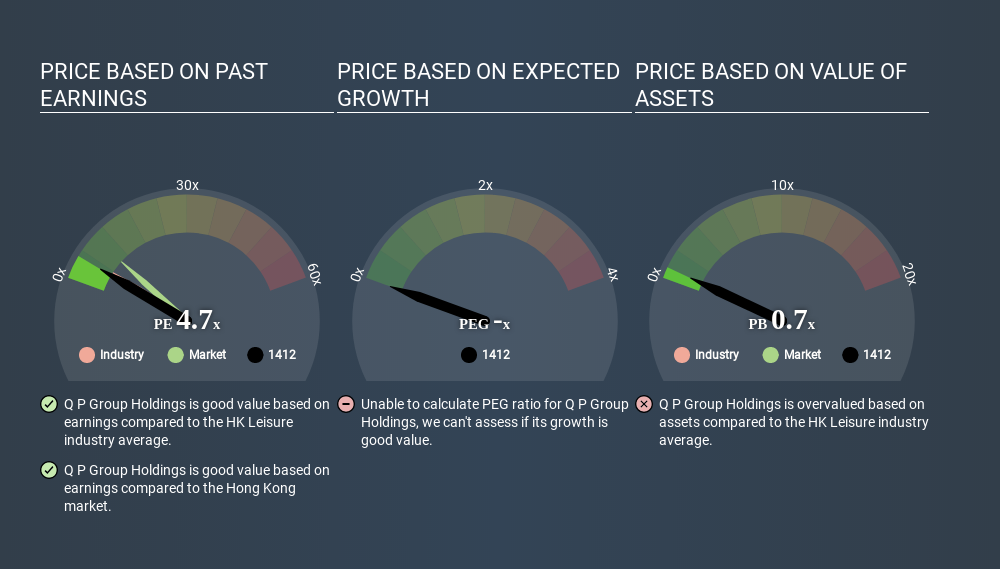

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll show how you can use Q P Group Holdings Limited's (HKG:1412) P/E ratio to inform your assessment of the investment opportunity. Based on the last twelve months, Q P Group Holdings's P/E ratio is 4.69. That means that at current prices, buyers pay HK$4.69 for every HK$1 in trailing yearly profits.

View our latest analysis for Q P Group Holdings

How Do You Calculate A P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Q P Group Holdings:

P/E of 4.69 = HK$0.990 ÷ HK$0.211 (Based on the year to December 2019.)

(Note: the above calculation results may not be precise due to rounding.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each HK$1 of company earnings. That isn't necessarily good or bad, but a high P/E implies relatively high expectations of what a company can achieve in the future.

Does Q P Group Holdings Have A Relatively High Or Low P/E For Its Industry?

The P/E ratio essentially measures market expectations of a company. We can see in the image below that the average P/E (5.6) for companies in the leisure industry is higher than Q P Group Holdings's P/E.

Q P Group Holdings's P/E tells us that market participants think it will not fare as well as its peers in the same industry. Since the market seems unimpressed with Q P Group Holdings, it's quite possible it could surprise on the upside. If you consider the stock interesting, further research is recommended. For example, I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means unless the share price falls, the P/E will increase in a few years. Then, a higher P/E might scare off shareholders, pushing the share price down.

Q P Group Holdings saw earnings per share decrease by 17% last year. And over the longer term (5 years) earnings per share have decreased 14% annually. This growth rate might warrant a below average P/E ratio.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. So it won't reflect the advantage of cash, or disadvantage of debt. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

So What Does Q P Group Holdings's Balance Sheet Tell Us?

Q P Group Holdings has net debt worth 16% of its market capitalization. This could bring some additional risk, and reduce the number of investment options for management; worth remembering if you compare its P/E to businesses without debt.

The Bottom Line On Q P Group Holdings's P/E Ratio

Q P Group Holdings trades on a P/E ratio of 4.7, which is below the HK market average of 9.5. The debt levels are not a major concern, but the lack of EPS growth is likely weighing on sentiment.

When the market is wrong about a stock, it gives savvy investors an opportunity. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. We don't have analyst forecasts, but shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

You might be able to find a better buy than Q P Group Holdings. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:1412

Q P Group Holdings

An investment holding company, manufactures and trades in paper products in the People’s Republic of China, the United States, Europe, and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor