Advertisement

These 4 Measures Indicate That Xtep International Holdings (HKG:1368) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Xtep International Holdings Limited (HKG:1368) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Xtep International Holdings

What Is Xtep International Holdings's Debt?

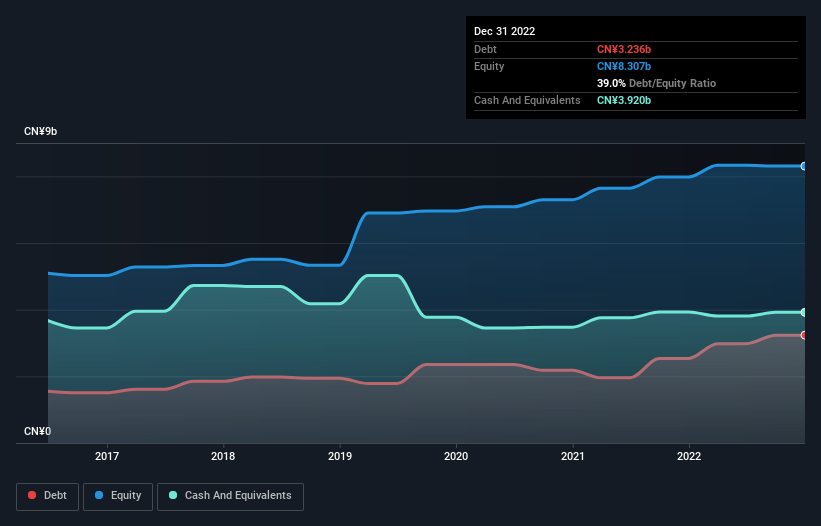

The image below, which you can click on for greater detail, shows that at December 2022 Xtep International Holdings had debt of CN¥3.24b, up from CN¥2.54b in one year. But on the other hand it also has CN¥3.92b in cash, leading to a CN¥684.2m net cash position.

A Look At Xtep International Holdings' Liabilities

According to the last reported balance sheet, Xtep International Holdings had liabilities of CN¥6.64b due within 12 months, and liabilities of CN¥1.54b due beyond 12 months. On the other hand, it had cash of CN¥3.92b and CN¥4.21b worth of receivables due within a year. So these liquid assets roughly match the total liabilities.

Having regard to Xtep International Holdings' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the CN¥20.1b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Xtep International Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely.

The good news is that Xtep International Holdings has increased its EBIT by 7.2% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Xtep International Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Xtep International Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Xtep International Holdings created free cash flow amounting to 18% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Xtep International Holdings has CN¥684.2m in net cash. On top of that, it increased its EBIT by 7.2% in the last twelve months. So we are not troubled with Xtep International Holdings's debt use. We'd be motivated to research the stock further if we found out that Xtep International Holdings insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1368

Xtep International Holdings

Designs, develops, manufactures, markets, and sells sports footwear, apparel, and accessories for adults and children in Mainland China.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor