Advertisement

Why We Think Best Linking Group Holdings Limited's (HKG:9882) CEO Compensation Is Not Excessive At All

Key Insights

- Best Linking Group Holdings to hold its Annual General Meeting on 6th of June

- CEO Yuk Chan's total compensation includes salary of HK$842.0k

- The overall pay is 60% below the industry average

- Best Linking Group Holdings' EPS declined by 44% over the past three years while total shareholder return over the past three years was 26%

Shareholders may be wondering what CEO Yuk Chan plans to do to improve the less than great performance at Best Linking Group Holdings Limited (HKG:9882) recently. They will get a chance to exercise their voting power to influence the future direction of the company in the next AGM on 6th of June. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

View our latest analysis for Best Linking Group Holdings

Comparing Best Linking Group Holdings Limited's CEO Compensation With The Industry

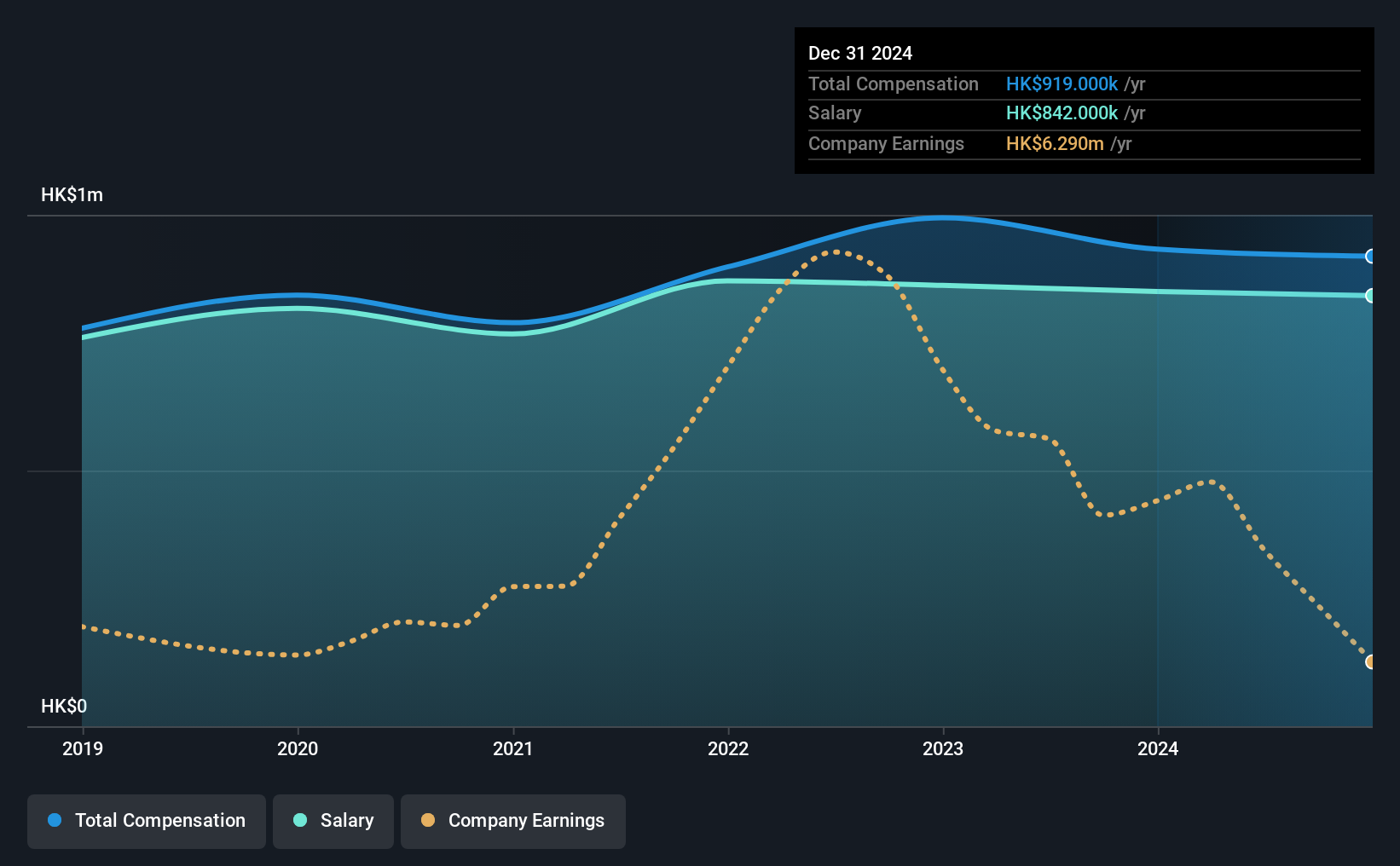

At the time of writing, our data shows that Best Linking Group Holdings Limited has a market capitalization of HK$528m, and reported total annual CEO compensation of HK$919k for the year to December 2024. This means that the compensation hasn't changed much from last year. In particular, the salary of HK$842.0k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the Hong Kong Machinery industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$2.3m. Accordingly, Best Linking Group Holdings pays its CEO under the industry median. What's more, Yuk Chan holds HK$396m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$842k | HK$850k | 92% |

| Other | HK$77k | HK$83k | 8% |

| Total Compensation | HK$919k | HK$933k | 100% |

On an industry level, around 77% of total compensation represents salary and 23% is other remuneration. It's interesting to note that Best Linking Group Holdings pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Best Linking Group Holdings Limited's Growth

Over the last three years, Best Linking Group Holdings Limited has shrunk its earnings per share by 44% per year. It saw its revenue drop 20% over the last year.

Few shareholders would be pleased to read that EPS have declined. And the impression is worse when you consider revenue is down year-on-year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Best Linking Group Holdings Limited Been A Good Investment?

Best Linking Group Holdings Limited has generated a total shareholder return of 26% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about the stock keeping up its current momentum. Shareholders might want to question the board about these concerns, and revisit their investment thesis for the company.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 2 warning signs for Best Linking Group Holdings that investors should look into moving forward.

Important note: Best Linking Group Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Best Linking Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:9882

Best Linking Group Holdings

Manufactures and sells slewing rings, machinery, and other mechanical parts and components.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor