Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Wing Fung Group Asia Limited (HKG:8526) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Wing Fung Group Asia

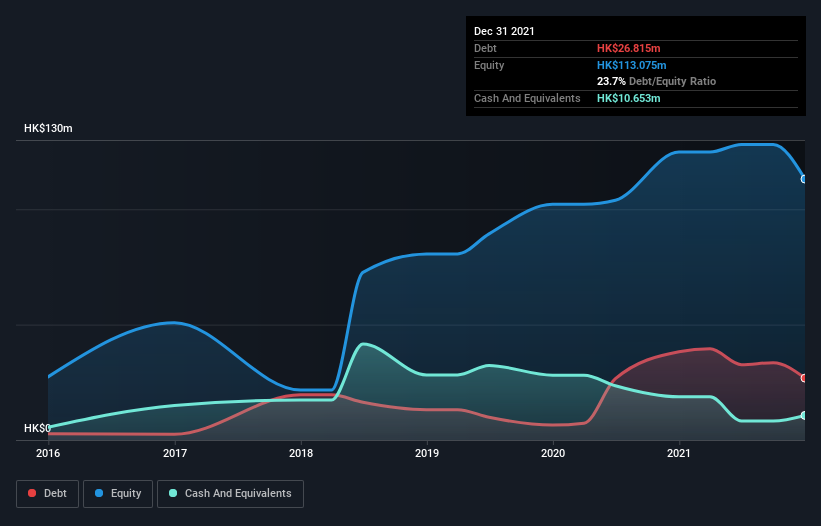

How Much Debt Does Wing Fung Group Asia Carry?

As you can see below, Wing Fung Group Asia had HK$26.8m of debt at December 2021, down from HK$38.2m a year prior. However, it does have HK$10.7m in cash offsetting this, leading to net debt of about HK$16.2m.

A Look At Wing Fung Group Asia's Liabilities

Zooming in on the latest balance sheet data, we can see that Wing Fung Group Asia had liabilities of HK$74.9m due within 12 months and liabilities of HK$132.0k due beyond that. On the other hand, it had cash of HK$10.7m and HK$156.1m worth of receivables due within a year. So it actually has HK$91.7m more liquid assets than total liabilities.

This surplus liquidity suggests that Wing Fung Group Asia's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Wing Fung Group Asia's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Wing Fung Group Asia made a loss at the EBIT level, and saw its revenue drop to HK$175m, which is a fall of 21%. That makes us nervous, to say the least.

Caveat Emptor

Not only did Wing Fung Group Asia's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Its EBIT loss was a whopping HK$23m. Having said that, the balance sheet has plenty of liquid assets for now. That should give the business time to grow its cashflow. The company is risky because it will grow into the future to get to profitability and free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with Wing Fung Group Asia (at least 1 which is concerning) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Wing Fung Group Asia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8526

Wing Fung Group Asia

An investment holding company, provides supply, installation, and fitting-out services of mechanical ventilation and air-conditioning systems for buildings in Hong Kong and Macau.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor