Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that NWS Holdings Limited (HKG:659) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Our analysis indicates that 659 is potentially undervalued!

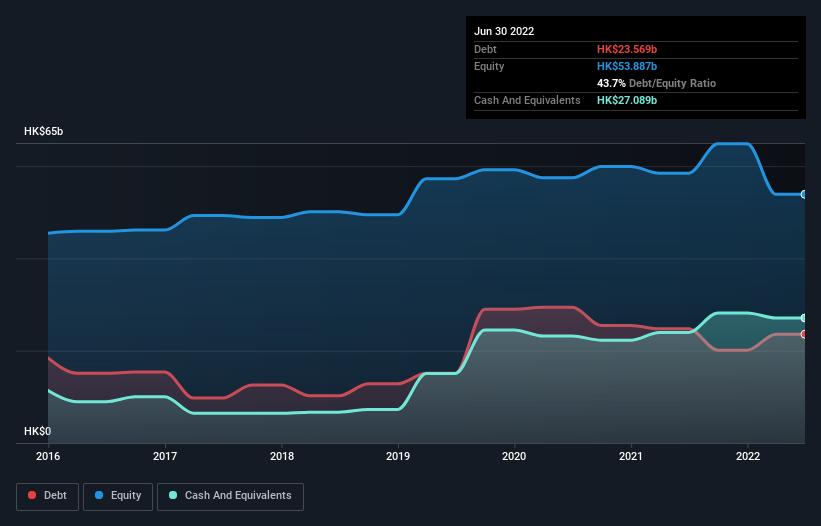

What Is NWS Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that NWS Holdings had debt of HK$23.6b at the end of June 2022, a reduction from HK$24.7b over a year. But it also has HK$27.1b in cash to offset that, meaning it has HK$3.52b net cash.

How Healthy Is NWS Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that NWS Holdings had liabilities of HK$56.9b due within 12 months and liabilities of HK$37.9b due beyond that. Offsetting this, it had HK$27.1b in cash and HK$14.2b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$53.6b.

This deficit casts a shadow over the HK$23.4b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, NWS Holdings would probably need a major re-capitalization if its creditors were to demand repayment. Given that NWS Holdings has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

Although NWS Holdings made a loss at the EBIT level, last year, it was also good to see that it generated HK$2.3b in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NWS Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While NWS Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last year, NWS Holdings actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

Although NWS Holdings's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of HK$3.52b. And it impressed us with free cash flow of HK$3.9b, being 165% of its EBIT. So although we see some areas for improvement, we're not too worried about NWS Holdings's balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with NWS Holdings , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:659

CTF Services

A conglomerate company with a diversified portfolio of businesses in toll roads, insurance, logistics, construction, and facilities management primarily in Hong Kong and the Mainland.

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor