Advertisement

TK Group (Holdings) Limited's (HKG:2283) Stock Is Going Strong: Is the Market Following Fundamentals?

TK Group (Holdings) (HKG:2283) has had a great run on the share market with its stock up by a significant 19% over the last three months. Given that the market rewards strong financials in the long-term, we wonder if that is the case in this instance. Particularly, we will be paying attention to TK Group (Holdings)'s ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for TK Group (Holdings)

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for TK Group (Holdings) is:

20% = HK$229m ÷ HK$1.1b (Based on the trailing twelve months to June 2020).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each HK$1 of shareholders' capital it has, the company made HK$0.20 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

TK Group (Holdings)'s Earnings Growth And 20% ROE

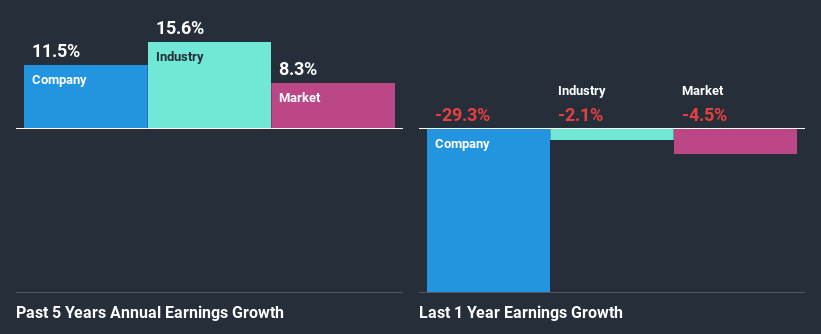

To begin with, TK Group (Holdings) seems to have a respectable ROE. Further, the company's ROE compares quite favorably to the industry average of 10%. This certainly adds some context to TK Group (Holdings)'s decent 11% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that TK Group (Holdings)'s reported growth was lower than the industry growth of 16% in the same period, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. What is 2283 worth today? The intrinsic value infographic in our free research report helps visualize whether 2283 is currently mispriced by the market.

Is TK Group (Holdings) Making Efficient Use Of Its Profits?

With a three-year median payout ratio of 46% (implying that the company retains 54% of its profits), it seems that TK Group (Holdings) is reinvesting efficiently in a way that it sees respectable amount growth in its earnings and pays a dividend that's well covered.

Additionally, TK Group (Holdings) has paid dividends over a period of seven years which means that the company is pretty serious about sharing its profits with shareholders. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 42%. As a result, TK Group (Holdings)'s ROE is not expected to change by much either, which we inferred from the analyst estimate of 22% for future ROE.

Conclusion

In total, we are pretty happy with TK Group (Holdings)'s performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. As a result, the decent growth in its earnings is not surprising. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you’re looking to trade TK Group (Holdings), open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if TK Group (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2283

TK Group (Holdings)

An investment holding company, engages in the manufacture, sale, subcontracting, fabrication, and modification of molds and plastic components.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor