Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Wan Kei Group Holdings Limited (HKG:1718) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Wan Kei Group Holdings

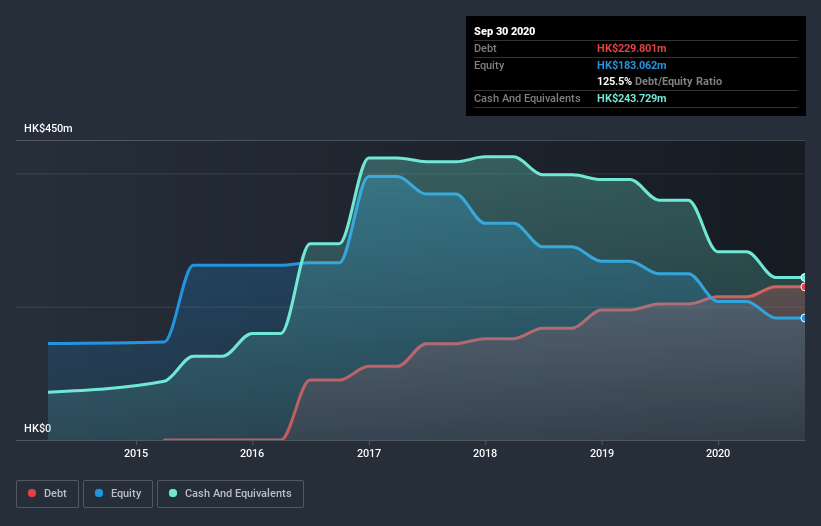

How Much Debt Does Wan Kei Group Holdings Carry?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Wan Kei Group Holdings had HK$229.8m of debt, an increase on HK$203.9m, over one year. But it also has HK$243.7m in cash to offset that, meaning it has HK$13.9m net cash.

A Look At Wan Kei Group Holdings's Liabilities

The latest balance sheet data shows that Wan Kei Group Holdings had liabilities of HK$291.4m due within a year, and liabilities of HK$5.15m falling due after that. On the other hand, it had cash of HK$243.7m and HK$178.9m worth of receivables due within a year. So it can boast HK$126.1m more liquid assets than total liabilities.

This surplus liquidity suggests that Wan Kei Group Holdings's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. Succinctly put, Wan Kei Group Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is Wan Kei Group Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Wan Kei Group Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 20%, to HK$278m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Wan Kei Group Holdings?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Wan Kei Group Holdings lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through HK$80m of cash and made a loss of HK$47m. While this does make the company a bit risky, it's important to remember it has net cash of HK$13.9m. That means it could keep spending at its current rate for more than two years. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Wan Kei Group Holdings (1 is concerning!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Wan Kei Group Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wan Kei Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1718

Wan Kei Group Holdings

An investment holding company, provides foundation construction and ground investigation field works to public and private sectors in Hong Kong and Mainland China.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor