Stock Analysis

Exploring Undiscovered Hong Kong Stocks With Solid Potential July 2024

Reviewed by Simply Wall St

As global markets navigate through varying economic signals, small-cap stocks, particularly in regions like Hong Kong, have shown notable resilience and potential for growth amid broader market fluctuations. The recent performance of indices such as the Russell 2000 highlights a robust environment for smaller companies that could harbor undervalued opportunities ready for discovery. In this context, identifying stocks with solid fundamentals and strategic market positions becomes crucial, especially in a dynamic landscape where economic indicators and investor sentiment are rapidly evolving.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| S.A.S. Dragon Holdings | 37.35% | 4.13% | 12.06% | ★★★★★★ |

| PW Medtech Group | NA | 17.93% | -2.70% | ★★★★★★ |

| China Leon Inspection Holding | 17.06% | 24.06% | 27.08% | ★★★★★★ |

| Sundart Holdings | 0.01% | -2.76% | -4.34% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| JiaXing Gas Group | 17.72% | 26.04% | 22.07% | ★★★★★☆ |

| Xin Point Holdings | 2.03% | 9.80% | 15.04% | ★★★★★☆ |

| Hung Hing Printing Group | 3.97% | -2.51% | 33.57% | ★★★★★☆ |

| Mulsanne Group Holding | 186.88% | -12.02% | -43.54% | ★★★★☆☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Luzhou Bank (SEHK:1983)

Simply Wall St Value Rating: ★★★★★★

Overview: Luzhou Bank Co., Ltd. operates as a provider of corporate and retail banking, financial market services, and other related services across the People’s Republic of China, with a market capitalization of HK$5.22 billion.

Operations: The bank primarily generates revenue through financial services, consistently achieving a gross profit margin of 100%. Net income has shown variability with a notable increase to CN¥968.83 million by the first quarter of 2024, reflecting growth in operational scale and efficiency.

Luzhou Bank, often overlooked, showcases robust financial health with CN¥159.2B in total assets and a prudent bad loans ratio at 1.3%. With earnings growth of 28.6% last year, surpassing the industry's 1.6%, it reflects high-quality earnings and sound management practices. Recently, Luzhou announced a dividend increase and appointed a new director, signaling ongoing governance enhancements and shareholder value focus—traits appealing to those scouting for potential in Hong Kong's banking sector.

- Unlock comprehensive insights into our analysis of Luzhou Bank stock in this health report.

Gain insights into Luzhou Bank's historical performance by reviewing our past performance report.

Luzhou Bank (SEHK:1983)

Simply Wall St Value Rating: ★★★★★★

Overview: Luzhou Bank Co., Ltd. operates as a provider of corporate and retail banking, financial market services, and other related services across the People’s Republic of China, with a market capitalization of HK$5.22 billion.

Operations: The bank primarily generates revenue through financial services, consistently achieving a gross profit margin of 100%. Net income has shown variability with a notable increase to CN¥968.83 million by the first quarter of 2024, reflecting growth in operational scale and efficiency.

Luzhou Bank, often overlooked, showcases robust financial health with CN¥159.2B in total assets and a prudent bad loans ratio at 1.3%. With earnings growth of 28.6% last year, surpassing the industry's 1.6%, it reflects high-quality earnings and sound management practices. Recently, Luzhou announced a dividend increase and appointed a new director, signaling ongoing governance enhancements and shareholder value focus—traits appealing to those scouting for potential in Hong Kong's banking sector.

- Unlock comprehensive insights into our analysis of Luzhou Bank stock in this health report.

Gain insights into Luzhou Bank's historical performance by reviewing our past performance report.

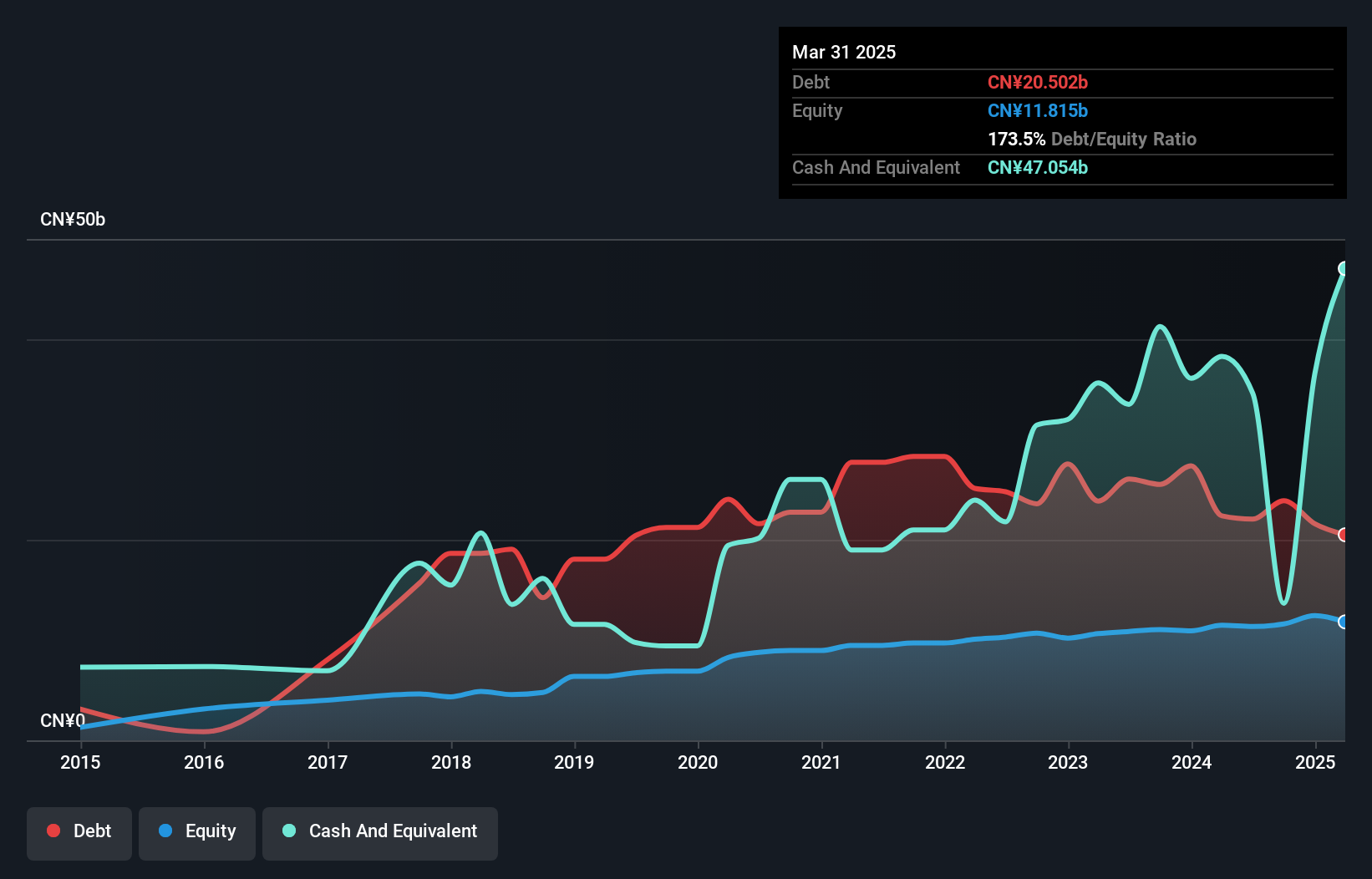

Harbin Bank (SEHK:6138)

Simply Wall St Value Rating: ★★★★★☆

Overview: Harbin Bank Co., Ltd. is a financial institution based in China, offering a range of banking products and services, with a market capitalization of HK$3.24 billion.

Operations: The bank generates revenue through its banking operations, consistently achieving a gross profit margin of 100% by not reporting any cost of goods sold. Its operating expenses, primarily general and administrative costs, have been a significant portion of its revenue across various reporting periods.

Harbin Bank, with its total assets of CN¥850.6 billion and a robust loan portfolio of CN¥345.8 billion, demonstrates significant financial depth in Hong Kong's lesser-tapped markets. The bank's earnings surged by an impressive 2142.8% over the past year, vastly outperforming the industry average growth of 1.6%. Moreover, Harbin maintains a healthy risk profile with a bad loans ratio at 2.7% and a sufficient allowance for bad loans at 201%. These figures underscore its potential as an undiscovered gem amidst evolving market dynamics.

- Get an in-depth perspective on Harbin Bank's performance by reading our health report here.

Examine Harbin Bank's past performance report to understand how it has performed in the past.

Harbin Bank (SEHK:6138)

Simply Wall St Value Rating: ★★★★★☆

Overview: Harbin Bank Co., Ltd. is a financial institution based in China, offering a range of banking products and services, with a market capitalization of HK$3.24 billion.

Operations: The bank generates revenue through its banking operations, consistently achieving a gross profit margin of 100% by not reporting any cost of goods sold. Its operating expenses, primarily general and administrative costs, have been a significant portion of its revenue across various reporting periods.

Harbin Bank, with its total assets of CN¥850.6 billion and a robust loan portfolio of CN¥345.8 billion, demonstrates significant financial depth in Hong Kong's lesser-tapped markets. The bank's earnings surged by an impressive 2142.8% over the past year, vastly outperforming the industry average growth of 1.6%. Moreover, Harbin maintains a healthy risk profile with a bad loans ratio at 2.7% and a sufficient allowance for bad loans at 201%. These figures underscore its potential as an undiscovered gem amidst evolving market dynamics.

- Get an in-depth perspective on Harbin Bank's performance by reading our health report here.

Examine Harbin Bank's past performance report to understand how it has performed in the past.

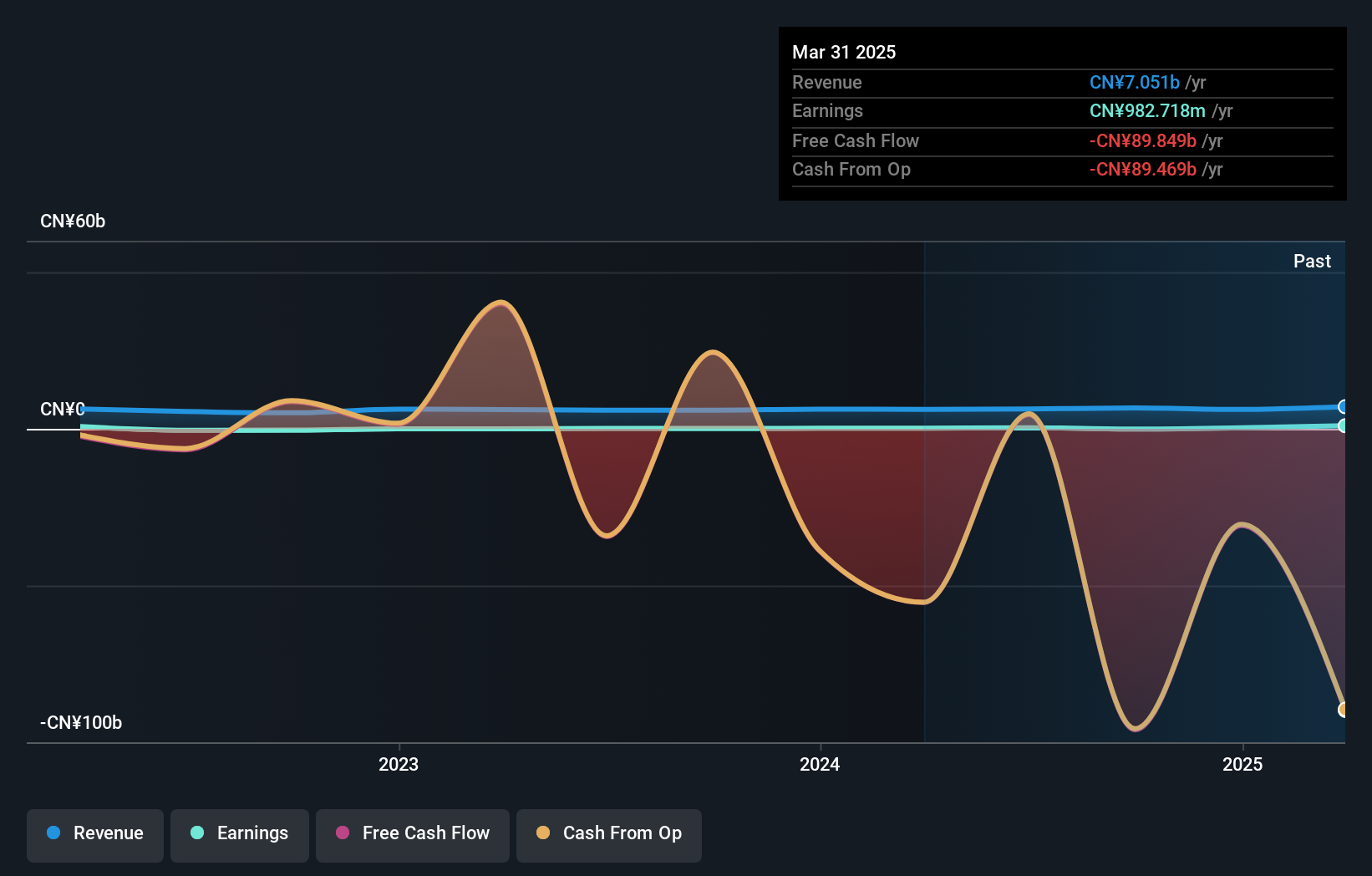

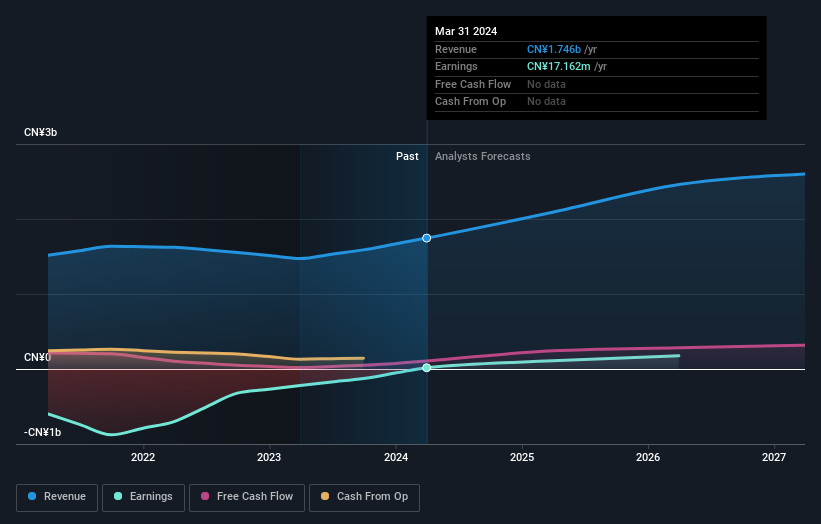

Arrail Group (SEHK:6639)

Simply Wall St Value Rating: ★★★★★★

Overview: Arrail Group Limited is a healthcare company that operates dental hospitals and clinics across China, with a market capitalization of HK$1.95 billion.

Operations: Arrail Dental and Rytime Dental, components of the company's operations, generated revenues of CN¥784.79 million and CN¥960.99 million respectively. The business has experienced a fluctuating gross profit margin over recent periods, with a notable figure of 22.49% as of the latest reported date in 2024, reflecting varying operational efficiencies and cost management strategies across its dental services segments.

Arrail Group, a lesser-known entity in Hong Kong's healthcare sector, has shown remarkable turnaround with its latest financials. From a substantial net loss last year, the company reported a net profit of CNY 17.16 million and sales growth to CNY 1,745.78 million this year, driven by increased patient visits and service improvements post-COVID-19. With earnings per share now at CNY 0.04 from previous losses and cash exceeding debt levels, Arrail's recovery seems robust amidst an industry growing at 3.1%.

- Take a closer look at Arrail Group's potential here in our health report.

Explore historical data to track Arrail Group's performance over time in our Past section.

Arrail Group (SEHK:6639)

Simply Wall St Value Rating: ★★★★★★

Overview: Arrail Group Limited is a healthcare company that operates dental hospitals and clinics across China, with a market capitalization of HK$1.95 billion.

Operations: Arrail Dental and Rytime Dental, components of the company's operations, generated revenues of CN¥784.79 million and CN¥960.99 million respectively. The business has experienced a fluctuating gross profit margin over recent periods, with a notable figure of 22.49% as of the latest reported date in 2024, reflecting varying operational efficiencies and cost management strategies across its dental services segments.

Arrail Group, a lesser-known entity in Hong Kong's healthcare sector, has shown remarkable turnaround with its latest financials. From a substantial net loss last year, the company reported a net profit of CNY 17.16 million and sales growth to CNY 1,745.78 million this year, driven by increased patient visits and service improvements post-COVID-19. With earnings per share now at CNY 0.04 from previous losses and cash exceeding debt levels, Arrail's recovery seems robust amidst an industry growing at 3.1%.

- Take a closer look at Arrail Group's potential here in our health report.

Explore historical data to track Arrail Group's performance over time in our Past section.

Turning Ideas Into Actions

- Gain an insight into the universe of 178 SEHK Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Harbin Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6138

Harbin Bank

Provides various banking products and services primarily in China.

Excellent balance sheet with proven track record.