Advertisement

Dah Sing Banking Group's (HKG:2356) Dividend Will Be Increased To HK$0.24

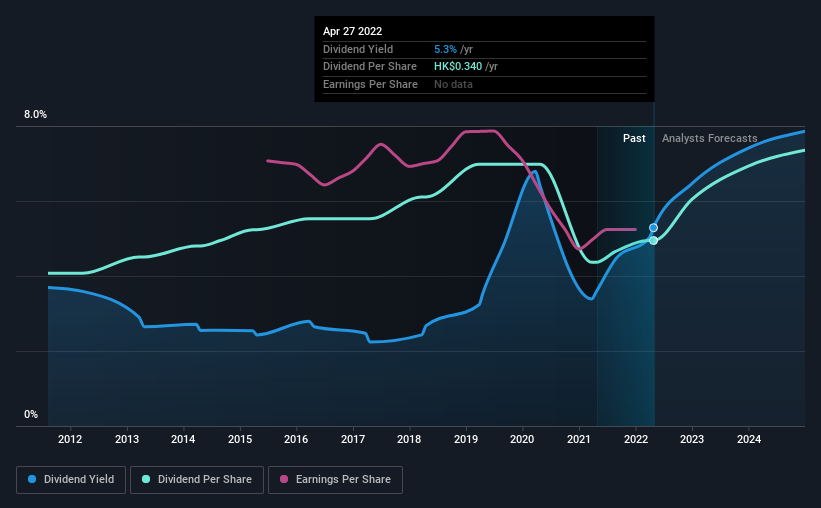

Dah Sing Banking Group Limited (HKG:2356) has announced that it will be increasing its dividend on the 16th of June to HK$0.24. Although the dividend is now higher, the yield is only 5.3%, which is below the industry average.

View our latest analysis for Dah Sing Banking Group

Dah Sing Banking Group's Earnings Easily Cover the Distributions

If it is predictable over a long period, even low dividend yields can be attractive. Prior to this announcement, Dah Sing Banking Group's earnings easily covered the dividend, but free cash flows were negative. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

Looking forward, earnings per share is forecast to rise by 12.8% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 25% by next year, which is in a pretty sustainable range.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The first annual payment during the last 10 years was HK$0.28 in 2012, and the most recent fiscal year payment was HK$0.34. This works out to be a compound annual growth rate (CAGR) of approximately 2.0% a year over that time. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

Dividend Growth Is Doubtful

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Dah Sing Banking Group has seen earnings per share falling at 5.1% per year over the last five years. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. Earnings are predicted to grow over the next year, but we would remain cautious until a track record of earnings growth is established.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think Dah Sing Banking Group's payments are rock solid. While the low payout ratio is redeeming feature, this is offset by the minimal cash to cover the payments. We don't think Dah Sing Banking Group is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 2 warning signs for Dah Sing Banking Group (of which 1 doesn't sit too well with us!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2356

Dah Sing Banking Group

An investment holding company, provides banking, financial, and other related services in Hong Kong, Macau, and the People’s Republic of China.

Adequate balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor