Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:1372

China Carbon Neutral Development Group (HKG:1372) Has A Somewhat Strained Balance Sheet

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that China Carbon Neutral Development Group Limited (HKG:1372) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for China Carbon Neutral Development Group

What Is China Carbon Neutral Development Group's Debt?

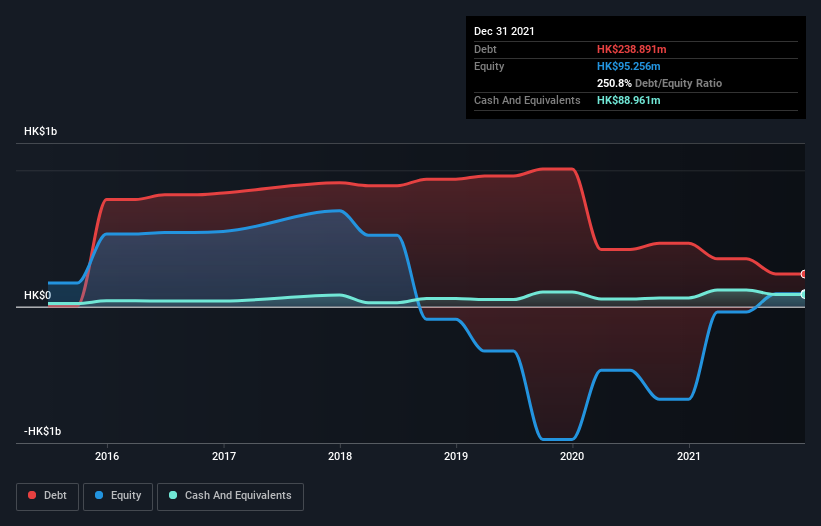

As you can see below, China Carbon Neutral Development Group had HK$238.9m of debt at December 2021, down from HK$464.8m a year prior. However, it does have HK$89.0m in cash offsetting this, leading to net debt of about HK$149.9m.

How Healthy Is China Carbon Neutral Development Group's Balance Sheet?

We can see from the most recent balance sheet that China Carbon Neutral Development Group had liabilities of HK$175.5m falling due within a year, and liabilities of HK$216.2m due beyond that. On the other hand, it had cash of HK$89.0m and HK$130.3m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$172.5m.

Of course, China Carbon Neutral Development Group has a market capitalization of HK$1.12b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

China Carbon Neutral Development Group has a very low debt to EBITDA ratio of 1.3 so it is strange to see weak interest coverage, with last year's EBIT being only 1.5 times the interest expense. So while we're not necessarily alarmed we think that its debt is far from trivial. Notably, China Carbon Neutral Development Group made a loss at the EBIT level, last year, but improved that to positive EBIT of HK$116m in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is China Carbon Neutral Development Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, China Carbon Neutral Development Group recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Both China Carbon Neutral Development Group's interest cover and its conversion of EBIT to free cash flow were discouraging. But its not so bad at managing its debt, based on its EBITDA,. Taking the abovementioned factors together we do think China Carbon Neutral Development Group's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 4 warning signs for China Carbon Neutral Development Group (1 can't be ignored) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1372

China Carbon Neutral Development Group

An investment holding company, engages in the civil engineering and construction business in Hong Kong, Macau, and Mainland China.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor