Advertisement

- Hong Kong

- /

- Auto Components

- /

- SEHK:1316

Nexteer Automotive Group Limited (HKG:1316) Looks Just Right With A 27% Price Jump

Despite an already strong run, Nexteer Automotive Group Limited (HKG:1316) shares have been powering on, with a gain of 27% in the last thirty days. The last month tops off a massive increase of 203% in the last year.

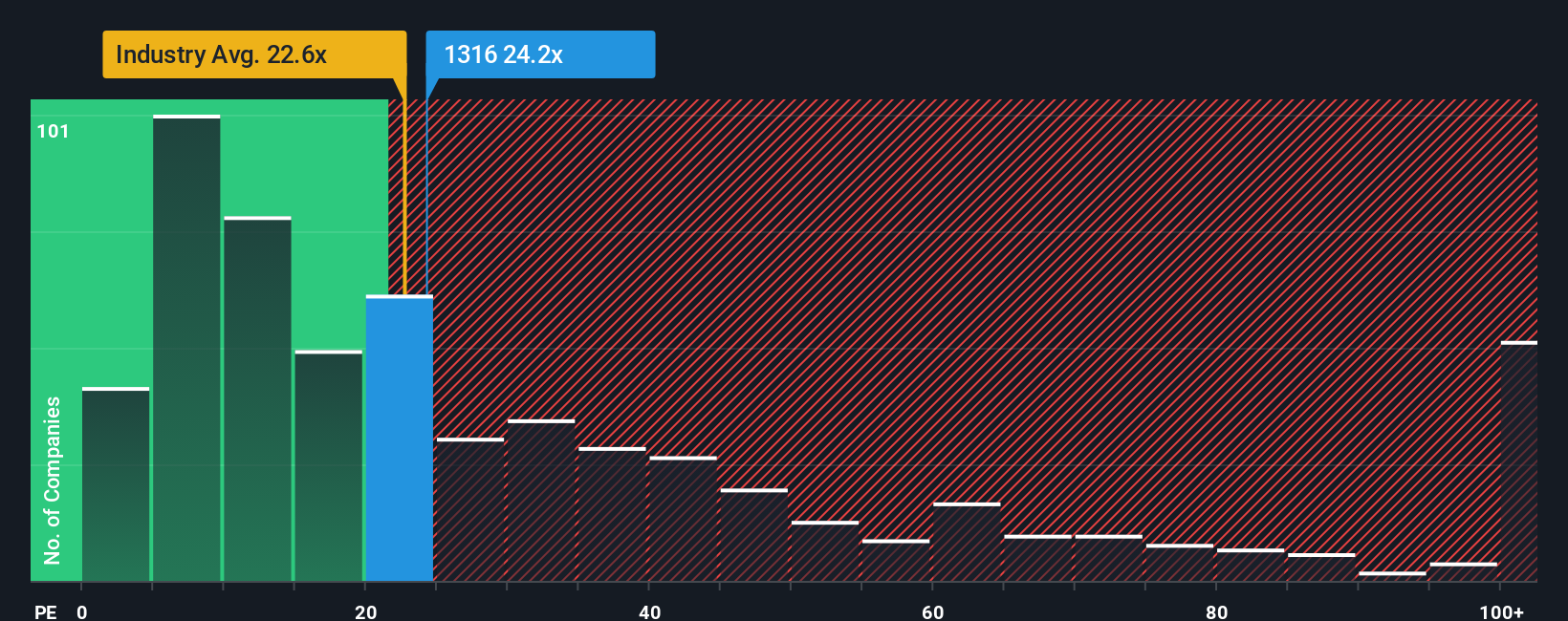

Following the firm bounce in price, Nexteer Automotive Group's price-to-earnings (or "P/E") ratio of 24.2x might make it look like a strong sell right now compared to the market in Hong Kong, where around half of the companies have P/E ratios below 12x and even P/E's below 7x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings growth that's superior to most other companies of late, Nexteer Automotive Group has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Nexteer Automotive Group

Is There Enough Growth For Nexteer Automotive Group?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Nexteer Automotive Group's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 494% gain to the company's bottom line. The latest three year period has also seen an excellent 353% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 17% per year as estimated by the analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 13% per year, which is noticeably less attractive.

With this information, we can see why Nexteer Automotive Group is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

The strong share price surge has got Nexteer Automotive Group's P/E rushing to great heights as well. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Nexteer Automotive Group's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Nexteer Automotive Group with six simple checks.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Nexteer Automotive Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1316

Nexteer Automotive Group

A motion control technology company, develops, manufactures, and supplies steering and driveline systems to original equipment manufacturer worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor