Advertisement

Performance Technologies S.A.'s (ATH:PERF) Shareholders Might Be Looking For Exit

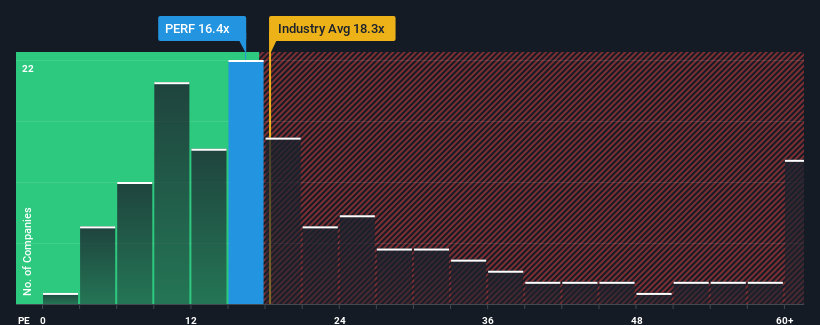

When close to half the companies in Greece have price-to-earnings ratios (or "P/E's") below 11x, you may consider Performance Technologies S.A. (ATH:PERF) as a stock to potentially avoid with its 16.4x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Performance Technologies has been doing a good job lately as it's been growing earnings at a solid pace. One possibility is that the P/E is high because investors think this respectable earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Performance Technologies

Does Growth Match The High P/E?

In order to justify its P/E ratio, Performance Technologies would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 17% last year. As a result, it also grew EPS by 8.6% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 8.6% shows it's noticeably less attractive on an annualised basis.

With this information, we find it concerning that Performance Technologies is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Key Takeaway

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Performance Technologies revealed its three-year earnings trends aren't impacting its high P/E anywhere near as much as we would have predicted, given they look worse than current market expectations. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Before you settle on your opinion, we've discovered 3 warning signs for Performance Technologies (1 is significant!) that you should be aware of.

You might be able to find a better investment than Performance Technologies. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:PERF

Performance Technologies

Provides production and marketing of it products, solutions and services, in Greece.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.0% undervalued

46 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23056.0% overvalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RI

richard_53rym on Nintendo ·

Nintendo facing the Ram shortage situation

Fair Value:JP¥8k11.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Rio Silver ·

Rare Pure High Grade Silver with 35% Insider (Near Producer)

Fair Value:CA$2298.8% undervalued

14 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Ares Strategic Mining ·

Ares Strategic Mining: $250M Pentagon Contract vs C$76M Market Cap

Fair Value:CA$0.9369.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.2% undervalued

85 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5452.2% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.4% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

HA

HarishPK on lululemon athletica ·

Difficult isn’t it? Valuation experts like Aswath Damodaran suggest 12 to 18 months for value and pr...

0

|0