Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Byte Computer S.A. (ATH:BYTE) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Byte Computer

How Much Debt Does Byte Computer Carry?

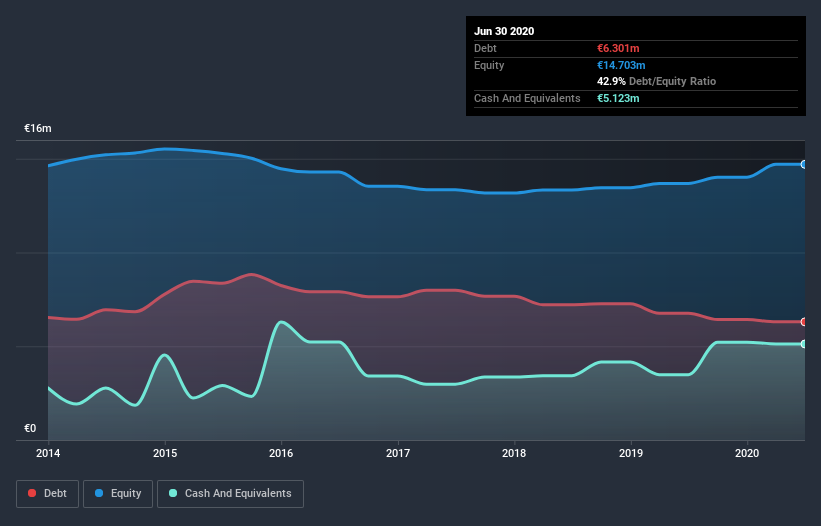

The image below, which you can click on for greater detail, shows that Byte Computer had debt of €6.30m at the end of June 2020, a reduction from €6.76m over a year. However, it also had €5.12m in cash, and so its net debt is €1.18m.

How Strong Is Byte Computer's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Byte Computer had liabilities of €13.1m due within 12 months and liabilities of €2.38m due beyond that. Offsetting these obligations, it had cash of €5.12m as well as receivables valued at €12.2m due within 12 months. So it actually has €1.88m more liquid assets than total liabilities.

This short term liquidity is a sign that Byte Computer could probably pay off its debt with ease, as its balance sheet is far from stretched.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Looking at its net debt to EBITDA of 0.63 and interest cover of 5.0 times, it seems to us that Byte Computer is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Importantly, Byte Computer grew its EBIT by 79% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Byte Computer will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Byte Computer recorded free cash flow worth a fulsome 85% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Byte Computer's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that's just the beginning of the good news since its EBIT growth rate is also very heartening. Overall, we don't think Byte Computer is taking any bad risks, as its debt load seems modest. So we're not worried about the use of a little leverage on the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Byte Computer you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Byte Computer, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Byte Computer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ATSE:BYTE

Byte Computer

Byte Computer S.A. provides integrated IT and communication solutions in Greece and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

33 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

TH

TheTurntTomato on Nokia Oyj ·

Nokia Strengthens Growth Outlook with Solid Q2 Results and Expanding AI Strategy

Fair Value:€15.1639.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DR

DrPotato on Zoetis ·

For a quality compounder with intact long-term fundamentals this can represent a favorable risk/reward entry

Fair Value:€155.2558.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

Reex on Unibap Space Solutions ·

Long-term bet on Europe's strategic space autonomy (2030–2055)

Fair Value:SEK 36.0176.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

103 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative