Stock Analysis

- United Kingdom

- /

- Renewable Energy

- /

- AIM:YU.

Exploring Undiscovered UK Stocks With Solid Fundamentals July 2024

Reviewed by Simply Wall St

Recent performance of the United Kingdom's stock market has shown a downturn, influenced heavily by disappointing trade data from China, which has significantly impacted sectors closely tied to Chinese economic activity. Amidst these broader market challenges, identifying stocks with solid fundamentals becomes crucial for investors looking for potential resilience and growth opportunities in less explored areas of the market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| Georgia Capital | NA | -27.80% | 18.94% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Fix Price Group | 43.59% | 12.53% | 23.49% | ★★★★★☆ |

| Ros Agro | 57.18% | 17.80% | 18.35% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

Warpaint London (AIM:W7L)

Simply Wall St Value Rating: ★★★★★★

Overview: Warpaint London PLC, together with its subsidiaries, produces and sells cosmetics with a market capitalization of £490.64 million.

Operations: Warpaint London generates revenue primarily through its own brand sales, which contributed £87.07 million, significantly overshadowing its close-out segment at £2.52 million. The company's business model has shown a robust gross profit margin averaging around 39.87% in the most recent period, reflecting efficient cost management relative to revenue generation.

Warpaint London, with its impressive 122.4% earnings growth outpacing the Personal Products industry's 16.5%, showcases robust performance. The company, debt-free and with high-quality earnings, recently declared a dividend increase to 6 pence per share and successfully raised £31.5 million through an equity offering priced at £4.5 per share, signaling strong investor confidence and financial health. These strategic moves underline Warpaint's potential as an appealing prospect within the UK market landscape.

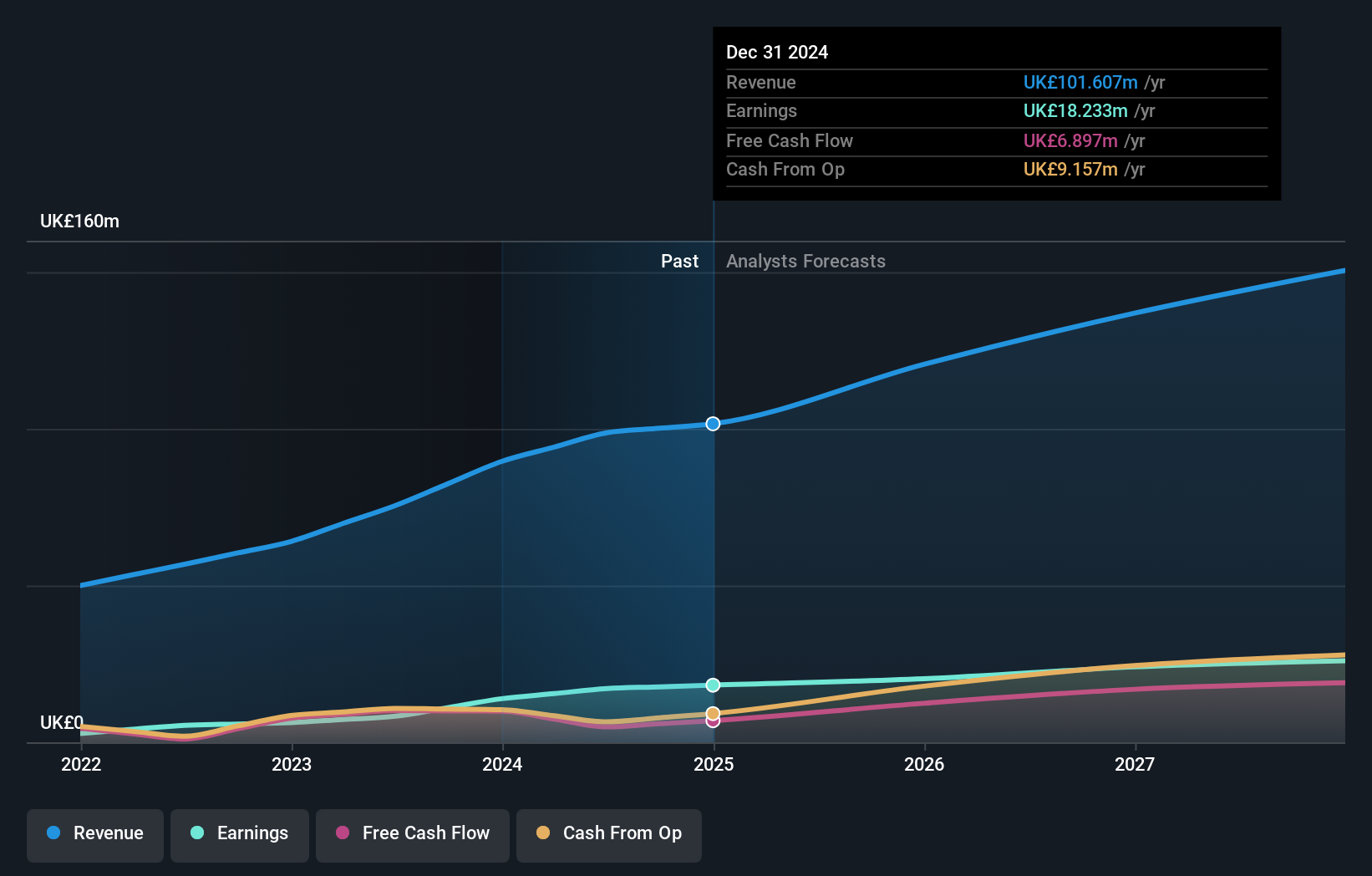

Yü Group (AIM:YU.)

Simply Wall St Value Rating: ★★★★★☆

Overview: Yü Group PLC is a UK-based company engaged in supplying energy and utility solutions, with a market capitalization of £315.55 million.

Operations: The company generates the majority of its revenue from retail activities, amounting to £459.80 million, complemented by smaller contributions from smart technologies and metering assets. It has experienced a notable increase in both gross profit and net income over recent periods, with the latest reported gross profit margin at 18.05% and a net income margin improvement to 6.71%.

Yü Group, a notable player in the Renewable Energy sector, has demonstrated remarkable financial and operational performance. With earnings growth outpacing the industry by 547.1% over the past year, Yü stands out for its robust profitability and potential for sustained growth, forecasted at 7.89% annually. Trading at 63.2% below its estimated fair value and having more cash than debt highlights its financial health. Despite significant insider selling recently, Yü’s strong earnings quality underscores its status as an undervalued gem in the UK market.

- Click here and access our complete health analysis report to understand the dynamics of Yü Group.

Understand Yü Group's track record by examining our Past report.

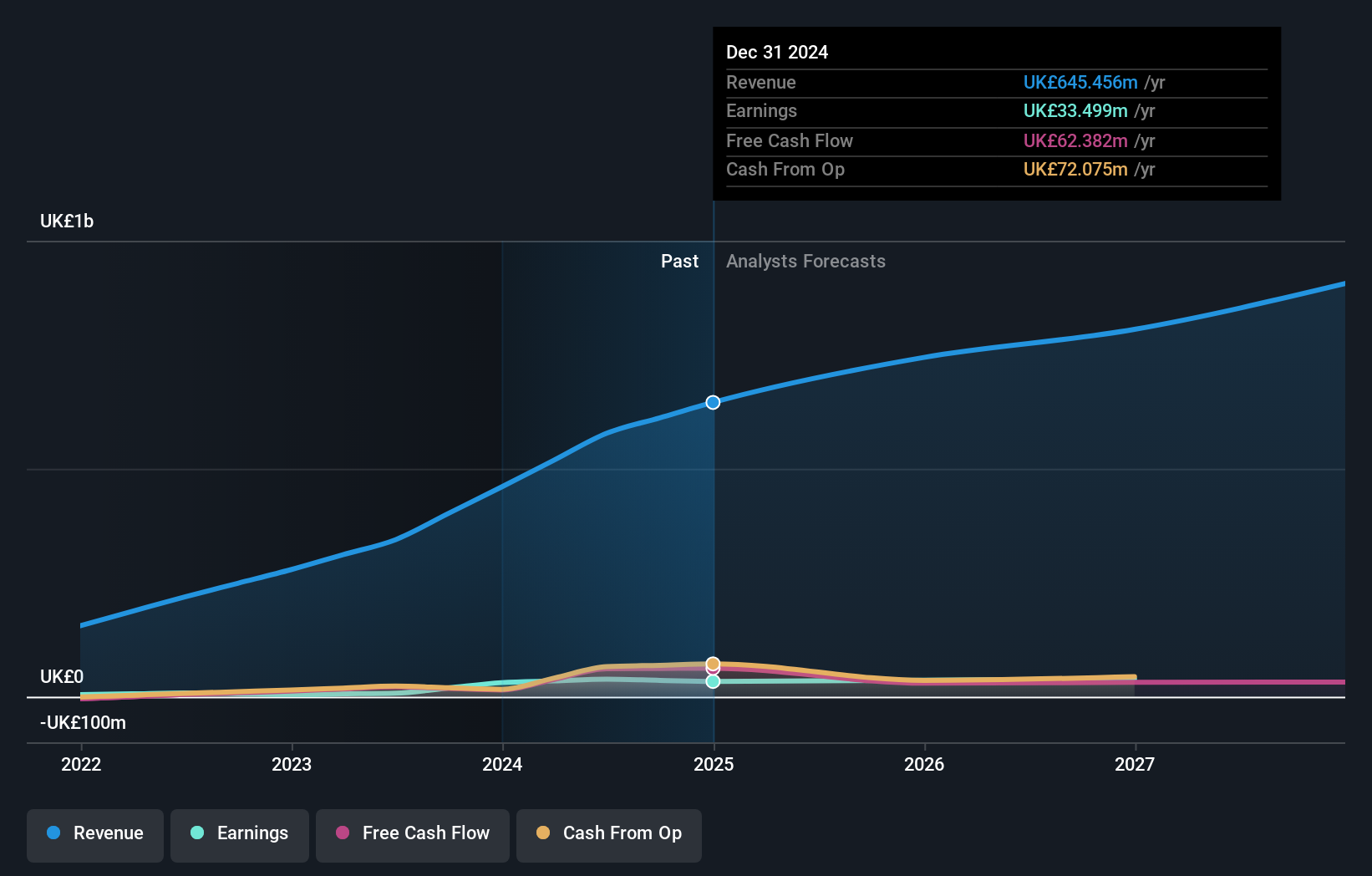

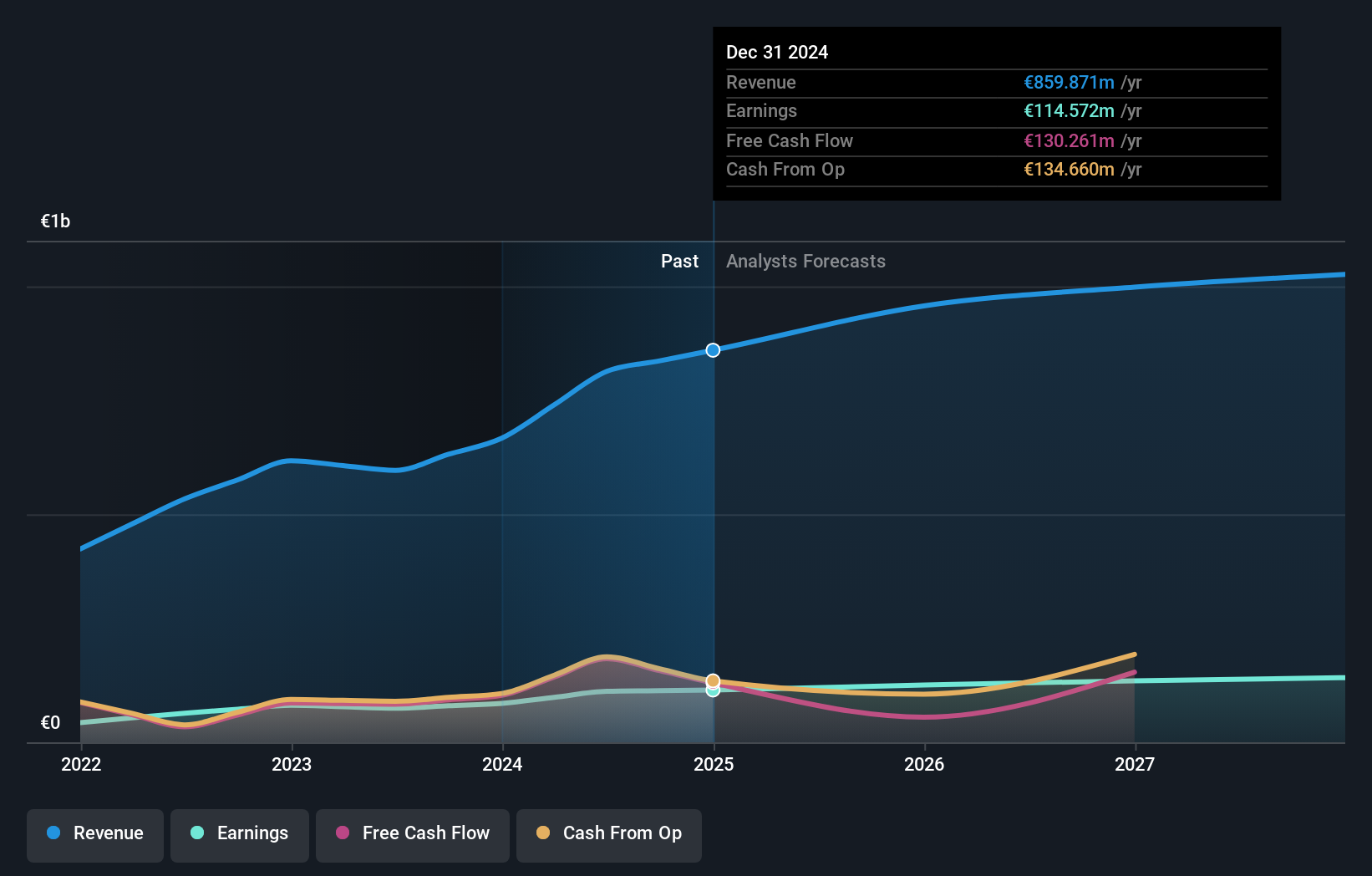

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★★

Overview: Cairn Homes plc is a home and community builder based in Ireland, with a market capitalization of approximately £1.03 billion.

Operations: Cairn Homes primarily generates its revenue through building and property development, with a notable increase in gross profit margin from 18.89% in late 2015 to 22.14% by the end of 2023, reflecting enhanced operational efficiency over the years. The company has consistently expanded its operations, as evidenced by a growth in revenue from €3.19 million at the end of 2015 to €666.81 million by late 2023, alongside managing operating expenses which stood at €34.23 million as of the latest report.

Cairn Homes, a standout in the UK's lesser-tapped markets, showcases robust financial health with a debt-to-equity reduction from 26% to 23% over five years. The company's earnings are on an upward trajectory, projected to grow by nearly 11% annually. Notably outperforming its sector with a 5.4% earnings increase last year against the industry’s downturn of -21.1%, Cairn Homes also offers compelling value, trading at 4.5% below estimated fair value while maintaining satisfactory net debt levels at 19.6%.

- Click here to discover the nuances of Cairn Homes with our detailed analytical health report.

Gain insights into Cairn Homes' historical performance by reviewing our past performance report.

Summing It All Up

- Dive into all 79 of the UK Undiscovered Gems With Strong Fundamentals we have identified here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Yü Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:YU.

Yü Group

Through its subsidiaries, supplies energy and utility solutions primarily in the United Kingdom.

Outstanding track record and undervalued.