Top High Growth Tech Stocks in the United Kingdom for September 2024

Reviewed by Simply Wall St

The market in the United Kingdom has been flat in the last week, but it is up 9.7% over the past year, with earnings expected to grow by 14% per annum over the next few years. In this promising environment, identifying high growth tech stocks that can capitalize on these favorable conditions is crucial for investors looking to maximize their returns.

Top 10 High Growth Tech Companies In The United Kingdom

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| STV Group | 13.15% | 46.78% | ★★★★★☆ |

| Altitude Group | 23.46% | 27.56% | ★★★★★☆ |

| Filtronic | 21.83% | 33.45% | ★★★★★★ |

| YouGov | 14.31% | 29.79% | ★★★★★☆ |

| Redcentric | 4.89% | 63.79% | ★★★★★☆ |

| LungLife AI | 100.61% | 100.97% | ★★★★★☆ |

| Trustpilot Group | 16.23% | 31.98% | ★★★★★☆ |

| IQGeo Group | 11.49% | 63.61% | ★★★★★☆ |

| Beeks Financial Cloud Group | 24.63% | 57.95% | ★★★★★☆ |

| Vinanz | 113.60% | 125.86% | ★★★★★☆ |

Click here to see the full list of 46 stocks from our UK High Growth Tech and AI Stocks screener.

Let's review some notable picks from our screened stocks.

Tracsis (AIM:TRCS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Tracsis plc, with a market cap of £209.33 million, provides software and hardware solutions along with data analytics/GIS services for the rail, traffic data, and transportation industry.

Operations: With a market cap of £209.33 million, Tracsis plc generates revenue primarily from two segments: Rail Technology & Services (£34.59 million) and Data, Analytics, Consultancy & Events (£44.80 million).

Tracsis, a leader in the tech sector, is poised for significant growth with earnings projected to rise 40.6% annually over the next three years, outpacing the broader UK market's 14.4%. Their revenue growth forecast at 6.3% per year surpasses the UK's average of 3.7%, highlighting robust performance despite not hitting high-growth benchmarks above 20%. Tracsis' R&D expenses underscore their commitment to innovation, with £5M invested last year driving advancements in their software solutions for transportation and infrastructure sectors.

- Take a closer look at Tracsis' potential here in our health report.

Assess Tracsis' past performance with our detailed historical performance reports.

Informa (LSE:INF)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Informa plc operates as an international events, digital services, and academic research company in the United Kingdom, Continental Europe, the United States, China, and internationally with a market cap of approximately £11.02 billion.

Operations: Informa generates revenue primarily through its four segments: Informa Tech (£426.70 million), Informa Connect (£630.20 million), Informa Markets (£1.67 billion), and Taylor & Francis (£636.70 million). The company's diverse portfolio encompasses international events, digital services, and academic research across various regions including the UK, Europe, the US, and China.

Informa's revenue is forecast to grow at 6.7% per year, outpacing the UK market average of 3.7%. Despite a significant one-off loss of £213.5M impacting recent financial results, earnings are projected to rise by 21.5% annually over the next three years, indicating strong future potential. The company has invested substantially in R&D, with expenditures contributing to innovations in their media and events segments. Additionally, Informa repurchased 41.67 million shares for £338.9M in the first half of 2024, reflecting confidence in its long-term growth strategy.

- Unlock comprehensive insights into our analysis of Informa stock in this health report.

Review our historical performance report to gain insights into Informa's's past performance.

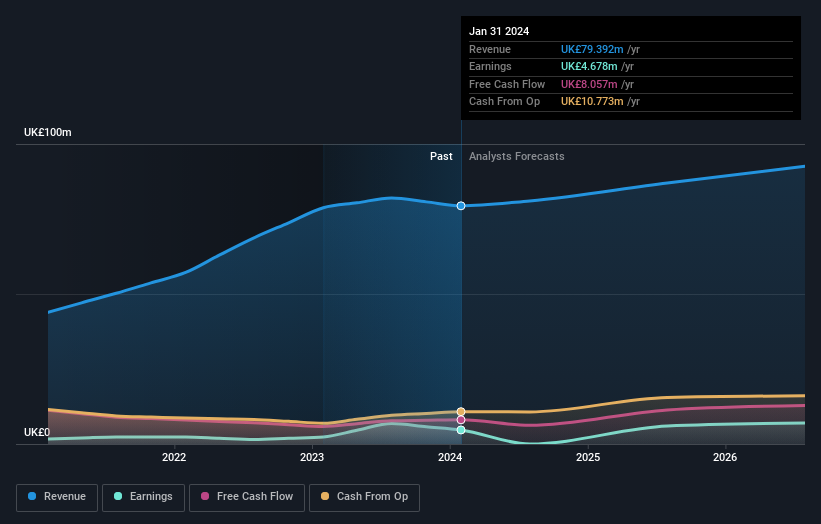

Trustpilot Group (LSE:TRST)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Trustpilot Group plc operates an online review platform for businesses and consumers across the United Kingdom, North America, Europe, and internationally, with a market cap of £877.35 million.

Operations: Trustpilot Group plc generates revenue primarily through its Internet Information Providers segment, amounting to $176.36 million. The company focuses on developing and hosting an online review platform for a global audience.

Trustpilot Group's revenue is forecast to grow at 16.2% per year, significantly outpacing the broader UK market's 3.7% growth rate. The company's earnings are expected to surge by 32% annually over the next three years, reflecting robust future potential. This growth trajectory is supported by substantial investments in R&D, with expenditures contributing to innovative enhancements in their review platform and services segments. Recently, Trafalgar Acquisition SARL indicated plans to sell up to 12.5 million shares through an accelerated bookbuild process, highlighting ongoing investor interest and activity around Trustpilot.

Summing It All Up

- Access the full spectrum of 46 UK High Growth Tech and AI Stocks by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trustpilot Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TRST

Trustpilot Group

Engages in the development and hosting of an online review platform for businesses and consumers in the United Kingdom, North America, Europe, and internationally.

Flawless balance sheet with high growth potential.