Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

Analysts Are Betting On Barratt Developments plc (LON:BDEV) With A Big Upgrade This Week

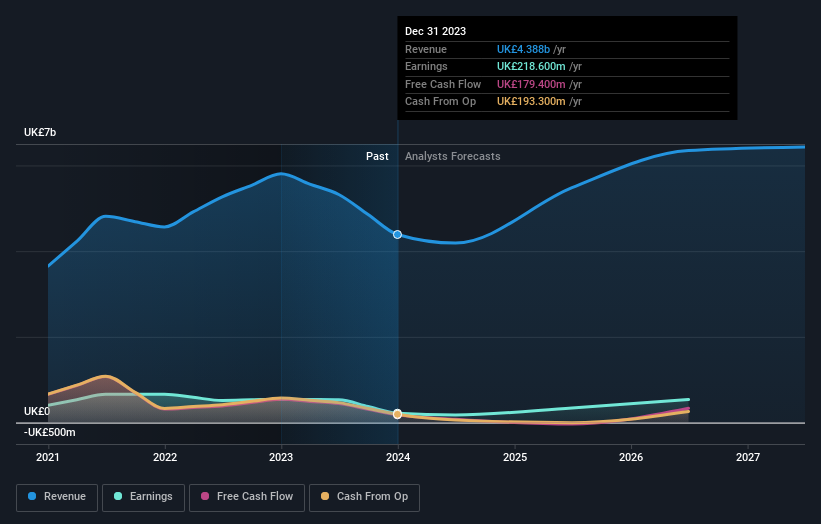

Barratt Developments plc (LON:BDEV) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

After the upgrade, the seven analysts covering Barratt Developments are now predicting revenues of UK£5.3b in 2025. If met, this would reflect a sizeable 22% improvement in sales compared to the last 12 months. Before the latest update, the analysts were foreseeing UK£4.2b of revenue in 2025. The consensus has definitely become more optimistic, showing a very substantial lift in revenue forecasts.

Check out our latest analysis for Barratt Developments

Additionally, the consensus price target for Barratt Developments increased 5.1% to UK£5.71, showing a clear increase in optimism from the analysts involved.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Barratt Developments' growth to accelerate, with the forecast 22% annualised growth to the end of 2025 ranking favourably alongside historical growth of 3.2% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.1% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Barratt Developments is expected to grow much faster than its industry.

The Bottom Line

The highlight for us was that analysts increased their revenue forecasts for Barratt Developments this year. Analysts also expect revenues to grow faster than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Barratt Developments.

Analysts are definitely bullish on Barratt Developments, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including the risk of cutting its dividend. You can learn more, and discover the 3 other warning signs we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

288 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

101 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

9 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

64 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18057.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

HedgeY on Newron Pharmaceuticals ·

Still A Binary Phase III Bet on Evenamide

Fair Value:CHF 1824.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

HedgeY on Kinepolis Group ·

A Premium Cinema Operator With a Quietly Compounding Cash Machine

Fair Value:€3515.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

101 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.5% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative