- United Kingdom

- /

- Diversified Financial

- /

- AIM:BOKU

Why We Think Shareholders May Be Considering Bumping Up Boku, Inc.'s (LON:BOKU) CEO Compensation

The solid performance at Boku, Inc. (LON:BOKU) has been impressive and shareholders will probably be pleased to know that CEO Jon Prideaux has delivered. At the upcoming AGM on 19 May 2021, they will get a chance to hear the board review the company results, discuss future strategy and cast their vote on any resolutions such as executive remuneration. Let's take a look at why we think the CEO has done a good job and we'll present the case for a bump in pay.

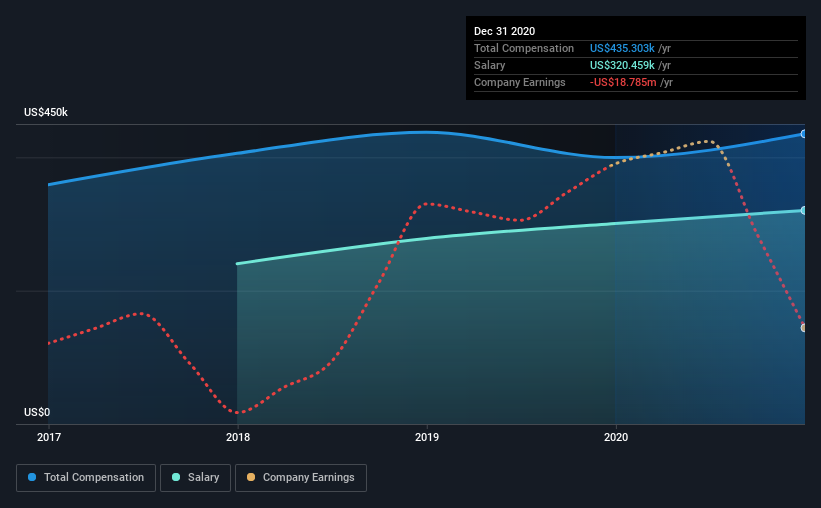

View our latest analysis for Boku

Comparing Boku, Inc.'s CEO Compensation With the industry

Our data indicates that Boku, Inc. has a market capitalization of UK£511m, and total annual CEO compensation was reported as US$435k for the year to December 2020. We note that's an increase of 8.9% above last year. We note that the salary portion, which stands at US$320.5k constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the same industry with market caps ranging from UK£284m to UK£1.1b, we found that the median CEO total compensation was US$732k. This suggests that Jon Prideaux is paid below the industry median. Furthermore, Jon Prideaux directly owns UK£5.0m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$320k | US$301k | 74% |

| Other | US$115k | US$99k | 26% |

| Total Compensation | US$435k | US$400k | 100% |

On an industry level, around 63% of total compensation represents salary and 37% is other remuneration. Boku is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Boku, Inc.'s Growth Numbers

Over the past three years, Boku, Inc. has seen its earnings per share (EPS) grow by 84% per year. It achieved revenue growth of 12% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Boku, Inc. Been A Good Investment?

Boasting a total shareholder return of 70% over three years, Boku, Inc. has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for Boku that you should be aware of before investing.

Switching gears from Boku, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you’re looking to trade Boku, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Boku might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:BOKU

Boku

Provides local payment solutions for merchants in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion