Advertisement

- United Kingdom

- /

- Food and Staples Retail

- /

- LSE:OCDO

Health Check: How Prudently Does Ocado Group (LON:OCDO) Use Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Ocado Group plc (LON:OCDO) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Ocado Group

What Is Ocado Group's Debt?

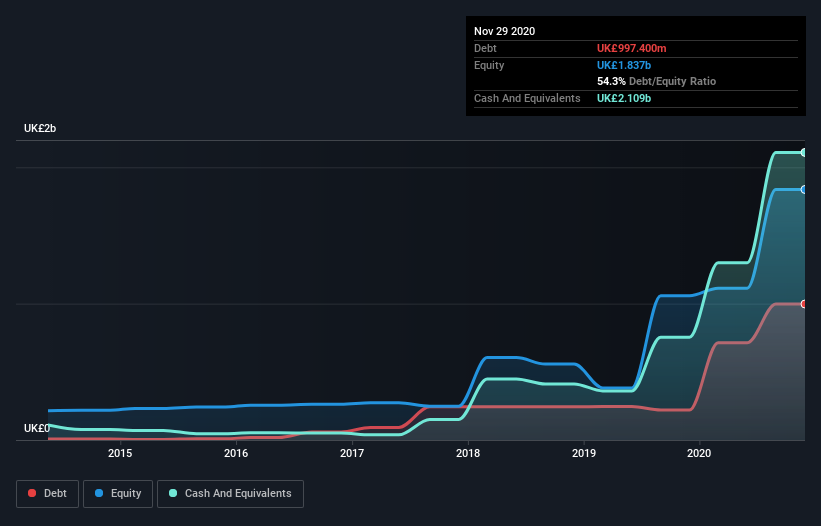

As you can see below, at the end of November 2020, Ocado Group had UK£997.4m of debt, up from UK£219.7m a year ago. Click the image for more detail. But it also has UK£2.11b in cash to offset that, meaning it has UK£1.11b net cash.

A Look At Ocado Group's Liabilities

The latest balance sheet data shows that Ocado Group had liabilities of UK£494.1m due within a year, and liabilities of UK£1.70b falling due after that. Offsetting these obligations, it had cash of UK£2.11b as well as receivables valued at UK£166.6m due within 12 months. So it can boast UK£84.4m more liquid assets than total liabilities.

This state of affairs indicates that Ocado Group's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the UK£14.8b company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that Ocado Group has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ocado Group can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Ocado Group reported revenue of UK£2.3b, which is a gain of 33%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Ocado Group?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Ocado Group had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through UK£226m of cash and made a loss of UK£126m. While this does make the company a bit risky, it's important to remember it has net cash of UK£1.11b. That kitty means the company can keep spending for growth for at least two years, at current rates. With very solid revenue growth in the last year, Ocado Group may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Ocado Group has 3 warning signs we think you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Ocado Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:OCDO

Ocado Group

Operates as an online grocery retailer in the United Kingdom and internationally.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor