Advertisement

Investors pursuing a solid, dependable stock investment can often be led to AstraZeneca PLC (LON:AZN), a large-cap worth UK£81b. One reason being its ‘too big to fail’ aura which gives it the appearance of a strong and stable investment. However, the key to their continued success lies in its financial health. Let’s take a look at AstraZeneca’s leverage and assess its financial strength to get an idea of their ability to fund strategic acquisitions and grow through cyclical pressures. Note that this information is centred entirely on financial health and is a high-level overview, so I encourage you to look further into AZN here.

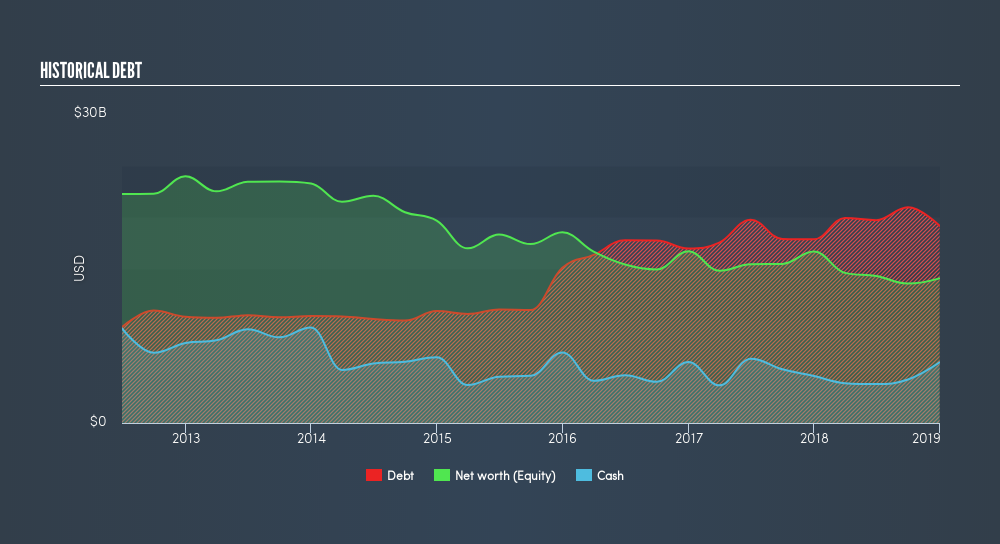

See our latest analysis for AstraZeneca

AZN’s Debt (And Cash Flows)

AZN has built up its total debt levels in the last twelve months, from US$18b to US$19b , which includes long-term debt. With this rise in debt, AZN's cash and short-term investments stands at US$5.9b to keep the business going. Moreover, AZN has produced US$2.6b in operating cash flow during the same period of time, leading to an operating cash to total debt ratio of 14%, indicating that AZN’s current level of operating cash is not high enough to cover debt.

Does AZN’s liquid assets cover its short-term commitments?

Looking at AZN’s US$16b in current liabilities, the company may not be able to easily meet these obligations given the level of current assets of US$16b, with a current ratio of 0.96x. The current ratio is calculated by dividing current assets by current liabilities.

Can AZN service its debt comfortably?

With total debt exceeding equities, AstraZeneca is considered a highly levered company. This isn’t surprising for large-caps, as equity can often be more expensive to issue than debt, plus interest payments are tax deductible. Consequently, larger-cap organisations tend to enjoy lower cost of capital as a result of easily attained financing, providing an advantage over smaller companies. We can assess the sustainability of AZN’s debt levels to the test by looking at how well interest payments are covered by earnings. Preferably, earnings before interest and tax (EBIT) should be at least three times as large as net interest. For AZN, the ratio of 2.86x suggests that interest is not strongly covered. Given the sheer size of AstraZeneca, it's unlikely to default on interest payments and enter bankruptcy. However, compared to an amply profitable large-cap peer, debtors may see more risk in lending to AZN.

Next Steps:

With a high level of debt on its balance sheet, AZN could still be in a financially strong position if its cash flow also stacked up. However, this isn’t the case, and there’s room for AZN to increase its operational efficiency. In addition to this, its lack of liquidity raises questions over current asset management practices for the large-cap. I admit this is a fairly basic analysis for AZN's financial health. Other important fundamentals need to be considered alongside. I recommend you continue to research AstraZeneca to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for AZN’s future growth? Take a look at our free research report of analyst consensus for AZN’s outlook.

- Valuation: What is AZN worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether AZN is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:AZN

AstraZeneca

A biopharmaceutical company, focuses on the discovery, development, manufacture, and commercialization of prescription medicines.

Undervalued with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor