- United Kingdom

- /

- Auto

- /

- LSE:AML

3 UK Growth Stocks With Up To 20% Insider Ownership

Reviewed by Simply Wall St

As the UK market grapples with global economic challenges, including weaker trade data from China impacting the FTSE indices, investors are keenly observing growth opportunities that can weather such uncertainties. In this context, companies with high insider ownership often attract attention due to their potential for aligned interests and long-term commitment, making them appealing candidates for those seeking resilient growth stocks.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 77% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| Foresight Group Holdings (LSE:FSG) | 34% | 23.5% |

| Facilities by ADF (AIM:ADF) | 13.1% | 190% |

| Judges Scientific (AIM:JDG) | 10.6% | 25.3% |

| Enteq Technologies (AIM:NTQ) | 27.2% | 53.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 26.4% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| PensionBee Group (LSE:PBEE) | 38.8% | 67.1% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 189.1% |

Here we highlight a subset of our preferred stocks from the screener.

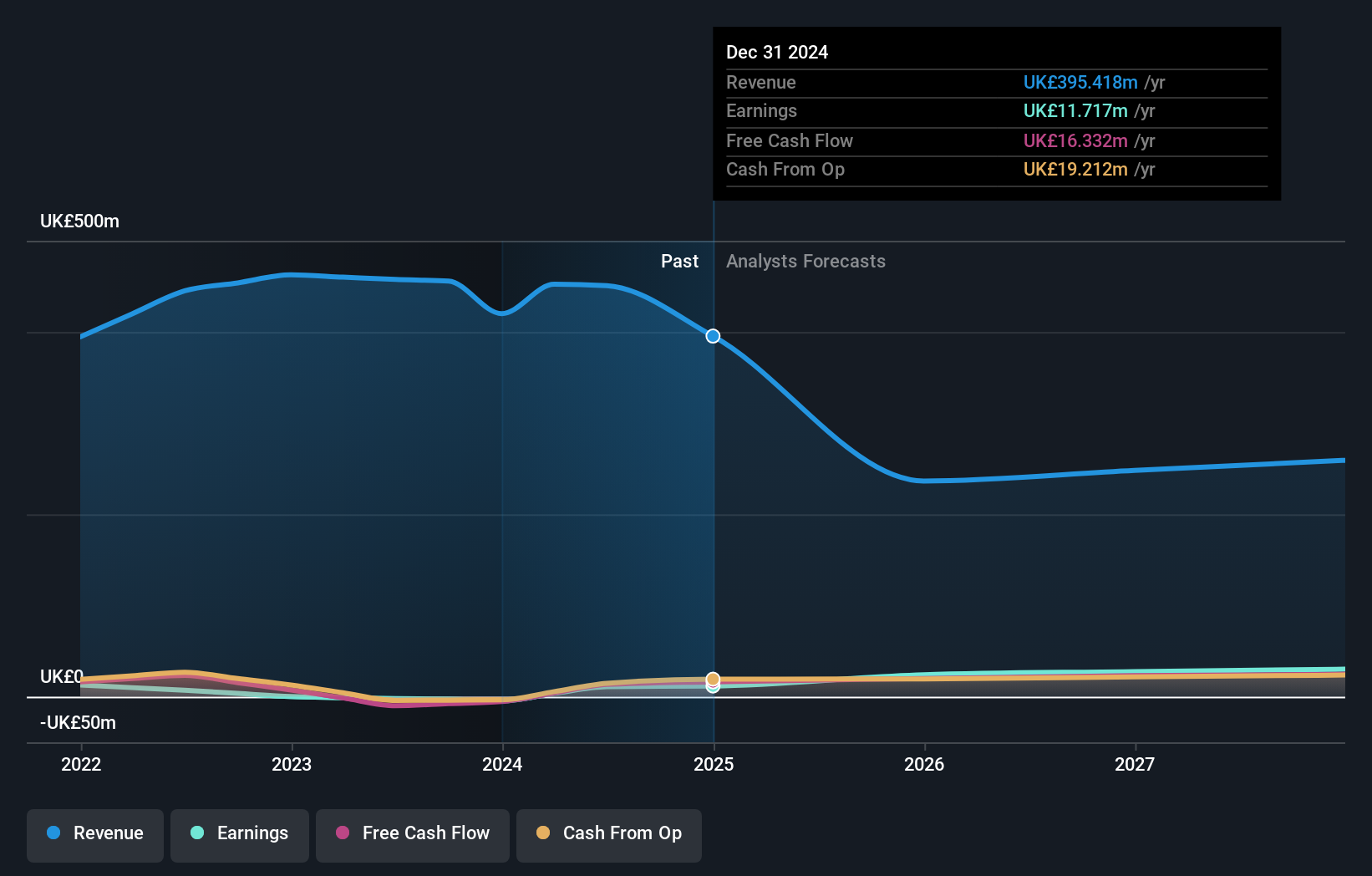

M&C Saatchi (AIM:SAA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: M&C Saatchi plc offers advertising and marketing communications services across the United Kingdom, Europe, the Middle East, Africa, the Asia Pacific, and the Americas with a market cap of £232.29 million.

Operations: M&C Saatchi plc generates revenue from providing advertising and marketing communications services across various regions, including the United Kingdom, Europe, the Middle East, Africa, the Asia Pacific, and the Americas.

Insider Ownership: 16.2%

M&C Saatchi shows potential as a growth company with high insider ownership, evidenced by significant insider buying in recent months. While the company's revenue is forecast to decline by 15.2% annually over the next three years, its earnings are expected to grow significantly at 27.4% per year, outpacing the UK market average. Recent profitability and a strong return on equity forecast of 32.1% bolster its appeal, despite trading at 59.5% below fair value estimates.

- Dive into the specifics of M&C Saatchi here with our thorough growth forecast report.

- Our valuation report unveils the possibility M&C Saatchi's shares may be trading at a discount.

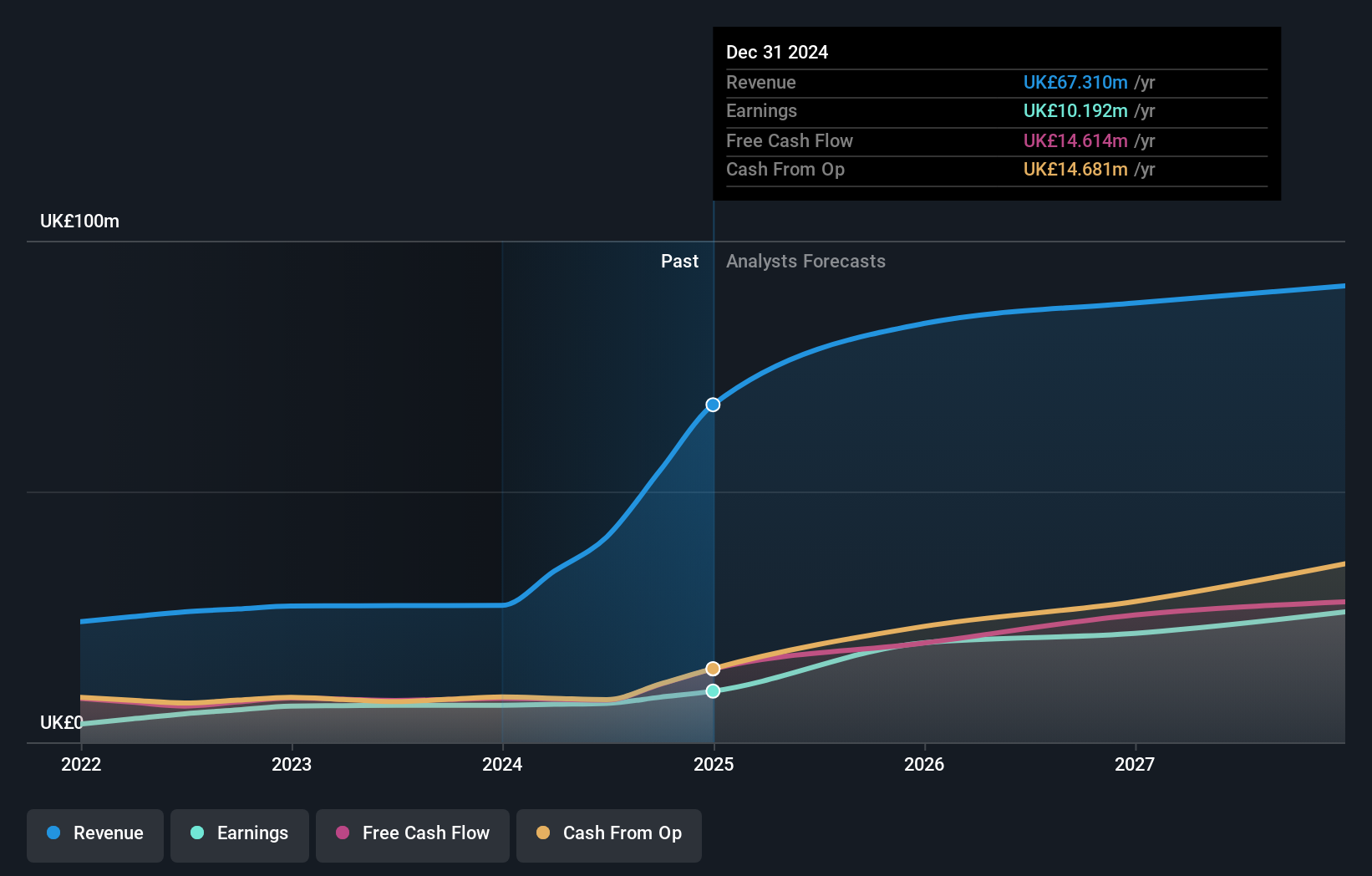

Property Franchise Group (AIM:TPFG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: The Property Franchise Group PLC manages and leases residential real estate properties in the United Kingdom, with a market cap of £267.17 million.

Operations: The company's revenue segments include £8.28 million from Financial Services and £31.64 million from Property Franchising in the UK.

Insider Ownership: 13.6%

The Property Franchise Group demonstrates growth potential with forecasted earnings and revenue growth significantly outpacing the UK market. Despite a dividend not well-covered by cash flows and recent shareholder dilution, insider activity shows more buying than selling over the past three months. The company recently reported increased sales of £26.85 million for H1 2024, up from £13.18 million year-on-year, alongside an interim dividend increase to 6.0 pence per share, reflecting confidence in its financial health.

- Click here and access our complete growth analysis report to understand the dynamics of Property Franchise Group.

- According our valuation report, there's an indication that Property Franchise Group's share price might be on the cheaper side.

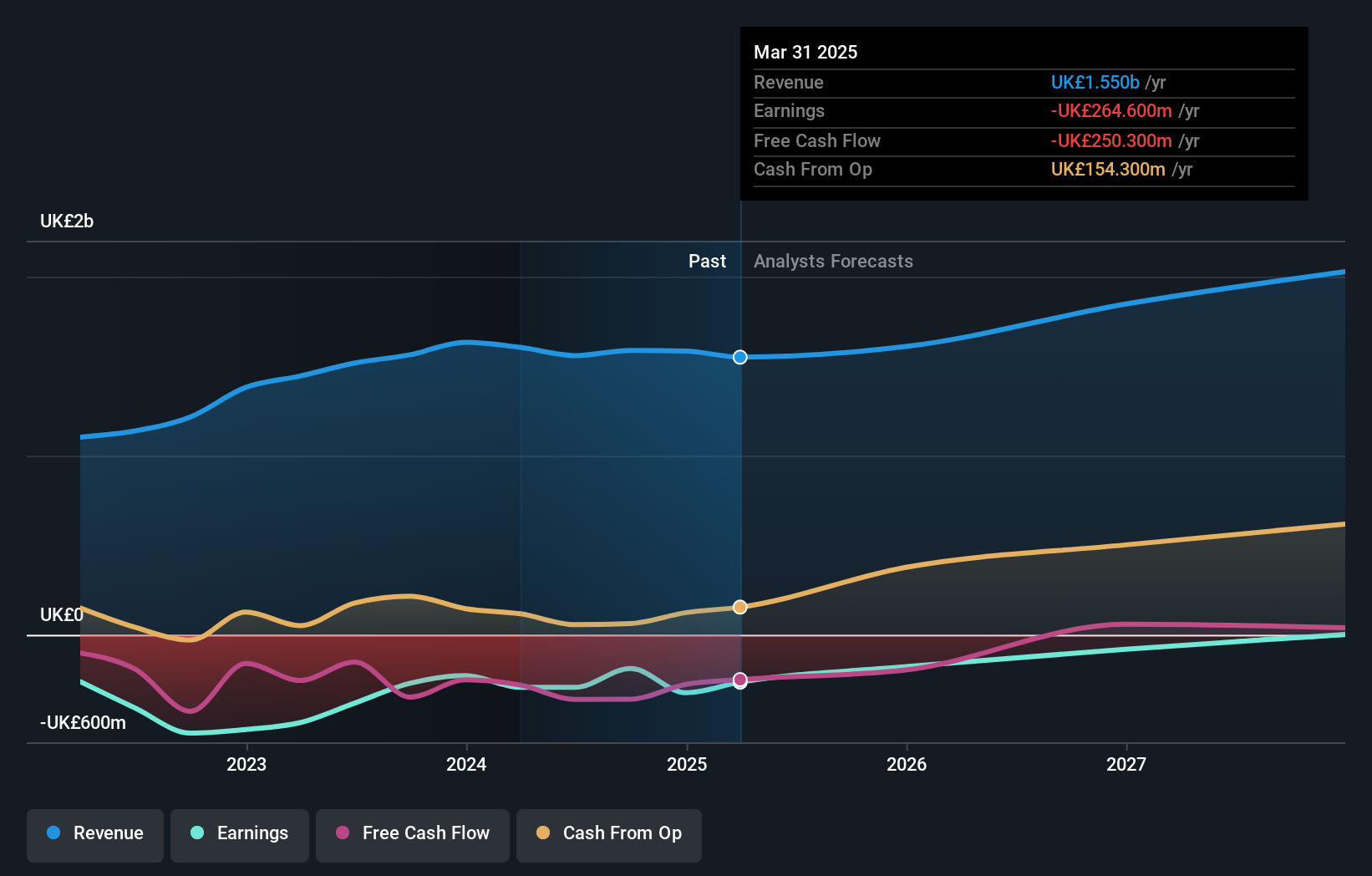

Aston Martin Lagonda Global Holdings (LSE:AML)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aston Martin Lagonda Global Holdings plc is involved in the design, development, manufacture, and marketing of luxury sports cars globally, with a market capitalization of approximately £905.05 million.

Operations: The company's revenue is primarily derived from its automotive segment, which generated £1.59 billion.

Insider Ownership: 20.6%

Aston Martin Lagonda Global Holdings shows mixed growth prospects with forecasted earnings growth of 62.85% annually, expected to become profitable in three years, outpacing the UK market. However, revenue growth is slower than desired at 12.4% per year. Recent follow-on equity offerings raised £221 million, indicating capital needs but also potential dilution concerns. Despite trading significantly below fair value and no substantial insider activity recently, its share price remains highly volatile.

- Unlock comprehensive insights into our analysis of Aston Martin Lagonda Global Holdings stock in this growth report.

- Our expertly prepared valuation report Aston Martin Lagonda Global Holdings implies its share price may be lower than expected.

Where To Now?

- Explore the 68 names from our Fast Growing UK Companies With High Insider Ownership screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:AML

Aston Martin Lagonda Global Holdings

Engages in the design, development, manufacture, and marketing of luxury sports cars worldwide.

Good value with reasonable growth potential.