- United Kingdom

- /

- Packaging

- /

- LSE:SMDS

DS Smith Plc (LON:SMDS) Reported Earnings Last Week And Analysts Are Already Upgrading Their Estimates

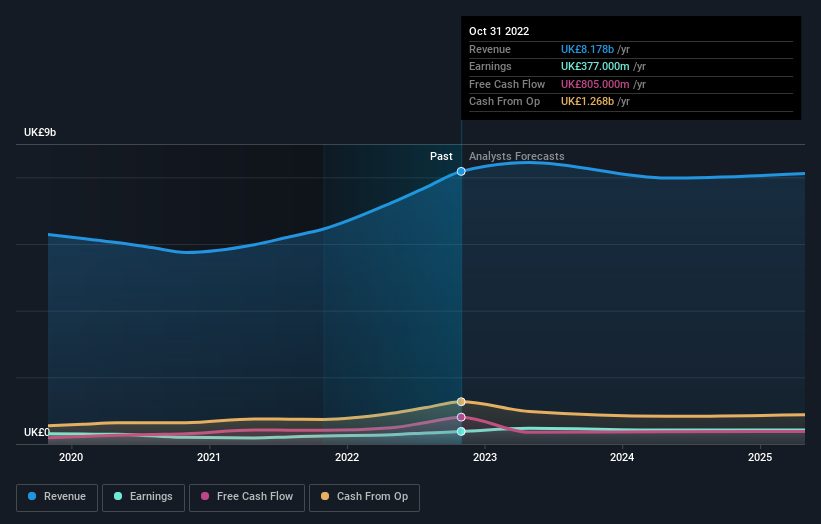

Investors in DS Smith Plc (LON:SMDS) had a good week, as its shares rose 6.5% to close at UK£3.28 following the release of its half-year results. It was a workmanlike result, with revenues of UK£4.3b coming in 4.2% ahead of expectations, and statutory earnings per share of UK£0.20, in line with analyst appraisals. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for DS Smith

After the latest results, the eleven analysts covering DS Smith are now predicting revenues of UK£8.45b in 2023. If met, this would reflect a credible 3.3% improvement in sales compared to the last 12 months. Per-share earnings are expected to shoot up 36% to UK£0.37. In the lead-up to this report, the analysts had been modelling revenues of UK£7.94b and earnings per share (EPS) of UK£0.31 in 2023. So it seems there's been a definite increase in optimism about DS Smith's future following the latest results, with a very substantial lift in the earnings per share forecasts in particular.

Althoughthe analysts have upgraded their earnings estimates, there was no change to the consensus price target of UK£3.85, suggesting that the forecast performance does not have a long term impact on the company's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic DS Smith analyst has a price target of UK£5.00 per share, while the most pessimistic values it at UK£3.10. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We can infer from the latest estimates that forecasts expect a continuation of DS Smith'shistorical trends, as the 6.6% annualised revenue growth to the end of 2023 is roughly in line with the 6.5% annual revenue growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 4.1% annually. So it's pretty clear that DS Smith is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around DS Smith's earnings potential next year. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. The consensus price target held steady at UK£3.85, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on DS Smith. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple DS Smith analysts - going out to 2025, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 2 warning signs for DS Smith you should be aware of, and 1 of them is significant.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:SMDS

DS Smith

Provides packaging solutions, paper products, and recycling services worldwide.

Slight with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion