Advertisement

- United Kingdom

- /

- Beverage

- /

- AIM:NICL

Dividend Investors: Don't Be Too Quick To Buy Nichols plc (LON:NICL) For Its Upcoming Dividend

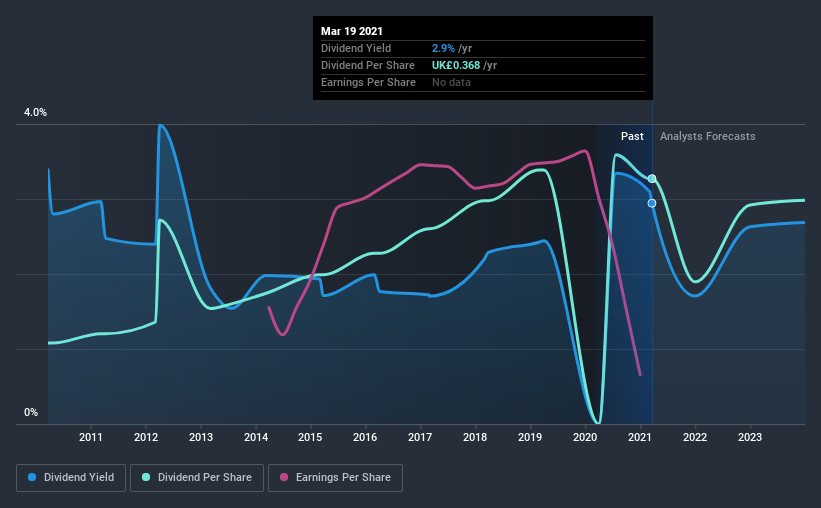

Nichols plc (LON:NICL) stock is about to trade ex-dividend in four days. This means that investors who purchase shares on or after the 25th of March will not receive the dividend, which will be paid on the 6th of May.

Nichols's upcoming dividend is UK£0.088 a share, following on from the last 12 months, when the company distributed a total of UK£0.37 per share to shareholders. Based on the last year's worth of payments, Nichols has a trailing yield of 2.9% on the current stock price of £12.5. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether Nichols can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Nichols

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. An unusually high payout ratio of 280% of its profit suggests something is happening other than the usual distribution of profits to shareholders. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. It paid out more than half (55%) of its free cash flow in the past year, which is within an average range for most companies.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Nichols fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Nichols's earnings per share have fallen at approximately 26% a year over the previous five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Since the start of our data, 10 years ago, Nichols has lifted its dividend by approximately 12% a year on average. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Nichols is already paying out 280% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

The Bottom Line

Should investors buy Nichols for the upcoming dividend? Earnings per share have been in decline, which is not encouraging. Worse, Nichols's paying out a majority of its earnings and more than half its free cash flow. Positive cash flows are good news but it's not a good combination. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Nichols.

So if you're still interested in Nichols despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. Our analysis shows 2 warning signs for Nichols and you should be aware of these before buying any shares.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Nichols, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nichols might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:NICL

Nichols

Engages in supply of soft drinks to the retail, wholesale, catering, licensed, and leisure industries in the United Kingdom, the Middle East, Africa, and internationally.

Excellent balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor