- United Kingdom

- /

- Specialty Stores

- /

- LSE:WOSG

December 2024 UK Stocks Trading Below Estimated Fair Value

Reviewed by Simply Wall St

The UK stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China, highlighting concerns over global economic recovery. In such an environment, identifying undervalued stocks can be crucial for investors seeking opportunities, as these stocks may have the potential to perform well despite broader market pressures.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TBC Bank Group (LSE:TBCG) | £30.35 | £58.95 | 48.5% |

| Gaming Realms (AIM:GMR) | £0.37 | £0.72 | 48.4% |

| Fevertree Drinks (AIM:FEVR) | £7.235 | £13.12 | 44.9% |

| Brickability Group (AIM:BRCK) | £0.648 | £1.24 | 47.7% |

| GlobalData (AIM:DATA) | £2.00 | £3.73 | 46.4% |

| Tracsis (AIM:TRCS) | £5.45 | £9.76 | 44.2% |

| Informa (LSE:INF) | £8.466 | £15.73 | 46.2% |

| Nexxen International (AIM:NEXN) | £3.915 | £7.52 | 48% |

| Videndum (LSE:VID) | £2.46 | £4.60 | 46.5% |

| St. James's Place (LSE:STJ) | £8.57 | £16.01 | 46.5% |

Here we highlight a subset of our preferred stocks from the screener.

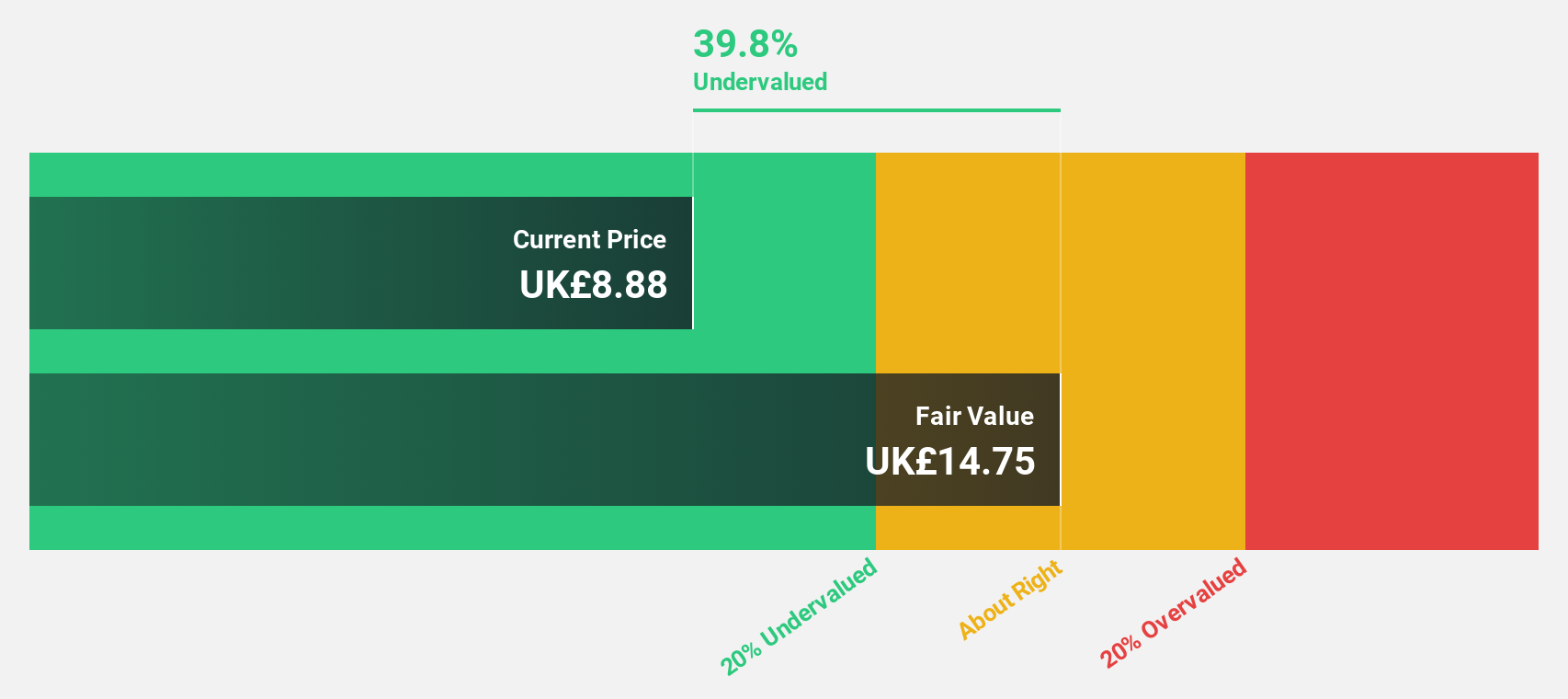

Fevertree Drinks (AIM:FEVR)

Overview: Fevertree Drinks PLC, along with its subsidiaries, develops and sells premium mixer drinks across the United Kingdom, the United States, Europe, and other international markets, with a market cap of £844.59 million.

Operations: The company's revenue is primarily derived from its non-alcoholic beverages segment, which generated £361.70 million.

Estimated Discount To Fair Value: 44.9%

Fevertree Drinks is trading at £7.24, significantly below its estimated fair value of £13.12, making it highly undervalued based on discounted cash flow analysis. Despite a modest revenue decline to £172.9 million for H1 2024, net income rose substantially to £7.6 million from the previous year’s £1.1 million, reflecting robust earnings growth of 84%. However, its dividend coverage by free cash flows remains weak at 2.3%.

- The growth report we've compiled suggests that Fevertree Drinks' future prospects could be on the up.

- Get an in-depth perspective on Fevertree Drinks' balance sheet by reading our health report here.

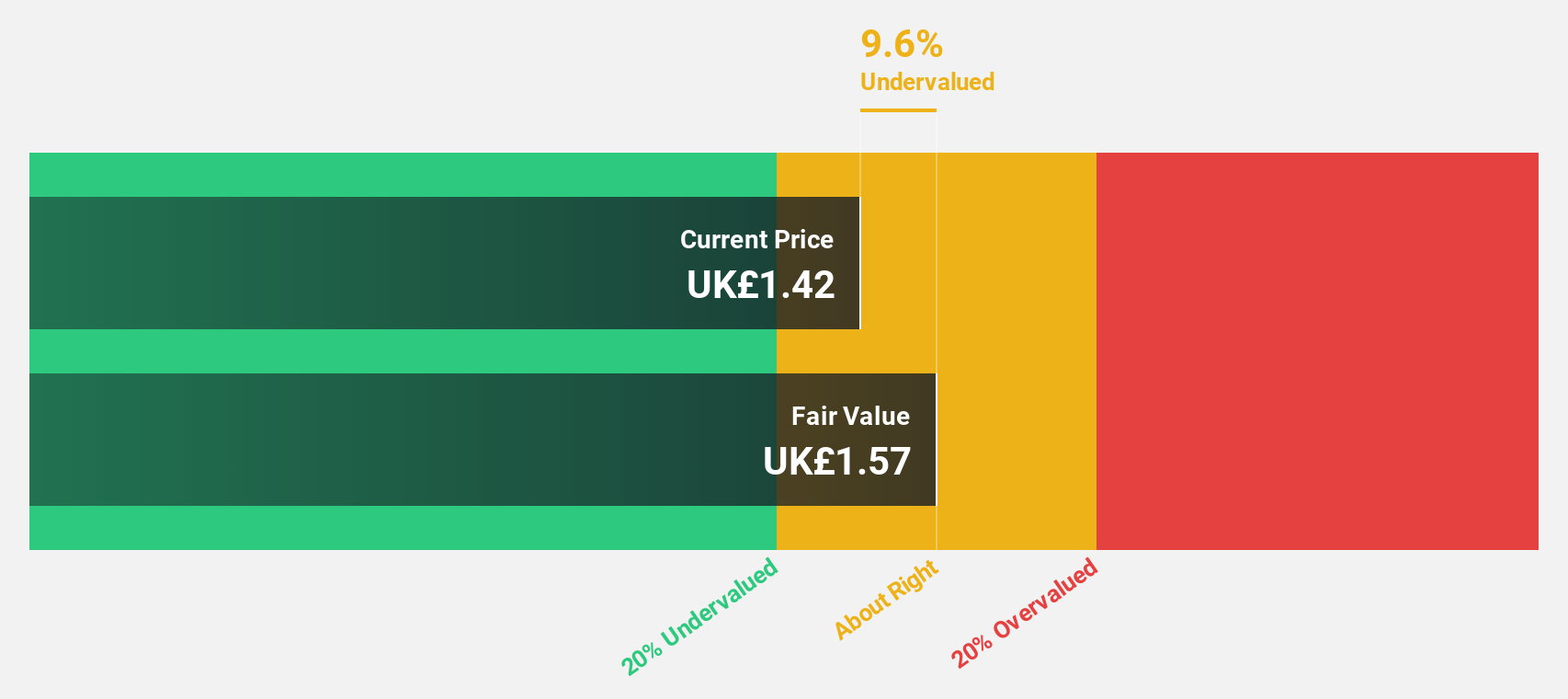

NCC Group (LSE:NCC)

Overview: NCC Group plc operates in the cyber and software resilience sector across the United Kingdom, Asia-Pacific, North America, and Europe with a market cap of £515.38 million.

Operations: The company's revenue is derived from Cyber Security, contributing £258.50 million, and Escode, accounting for £65.90 million.

Estimated Discount To Fair Value: 33.9%

NCC Group is trading at £1.64, well below its estimated fair value of £2.49, indicating it is significantly undervalued based on discounted cash flow analysis. Despite a forecasted low return on equity of 13.4% in three years, NCC's earnings are expected to grow substantially by 87.41% annually and become profitable over the same period, outpacing the UK market's revenue growth rate. Recent inclusion in multiple FTSE indices enhances its visibility among investors.

- Our comprehensive growth report raises the possibility that NCC Group is poised for substantial financial growth.

- Click here to discover the nuances of NCC Group with our detailed financial health report.

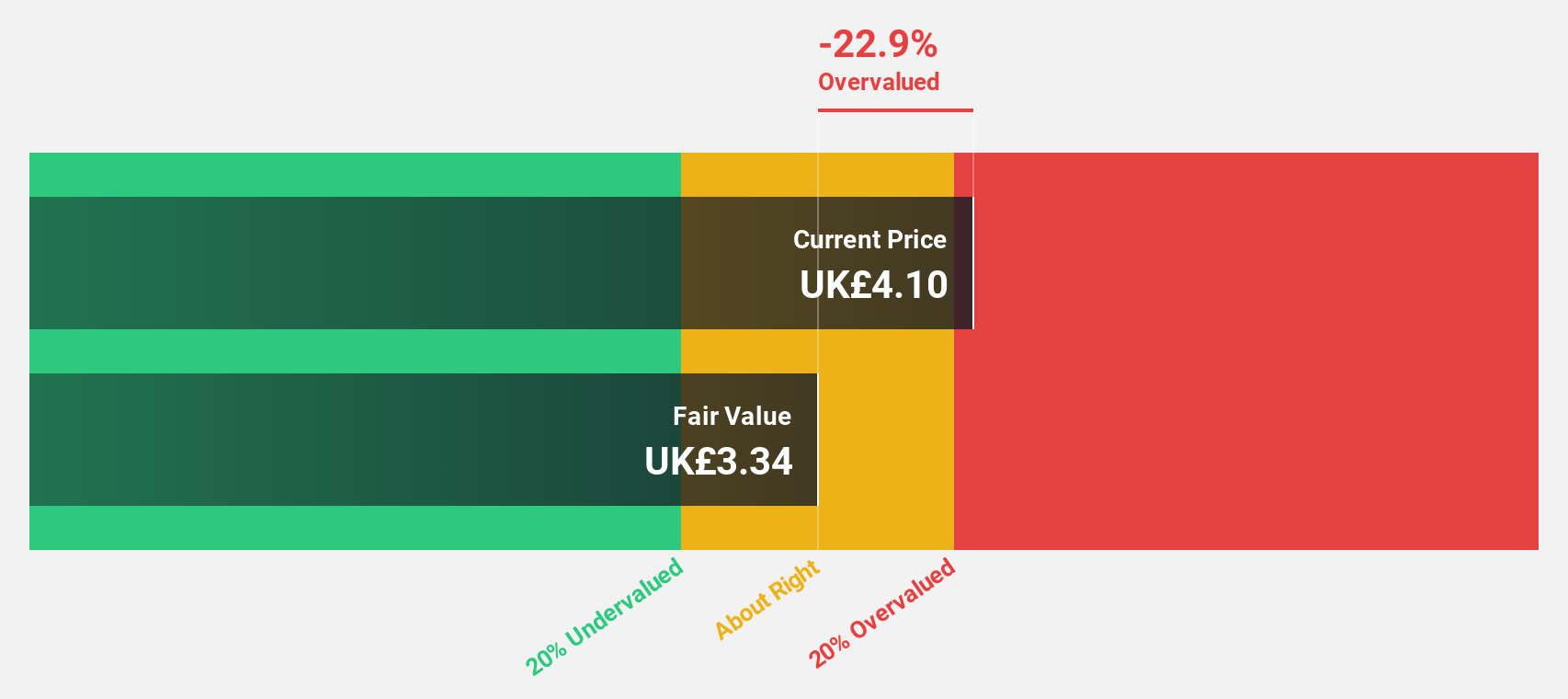

Watches of Switzerland Group (LSE:WOSG)

Overview: Watches of Switzerland Group PLC is a retailer specializing in luxury watches and jewelry across the United Kingdom, Europe, and the United States, with a market cap of £1.37 billion.

Operations: The company's revenue is derived from two primary segments: £846.10 million from the UK & Europe and £691.80 million from the US.

Estimated Discount To Fair Value: 43.3%

Watches of Switzerland Group is trading at £5.7, significantly below its estimated fair value of £10.06, highlighting its undervaluation based on discounted cash flow analysis. Despite a recent decline in profit margins and net income, the company's earnings are forecast to grow 20.1% annually, outpacing the UK market's growth rate of 14.7%. However, revenue growth is slower than desired at 8.3% per year amid high share price volatility recently observed.

- According our earnings growth report, there's an indication that Watches of Switzerland Group might be ready to expand.

- Dive into the specifics of Watches of Switzerland Group here with our thorough financial health report.

Summing It All Up

- Dive into all 57 of the Undervalued UK Stocks Based On Cash Flows we have identified here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Watches of Switzerland Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:WOSG

Watches of Switzerland Group

Operates as a retailer of luxury watches and jewelry in the United Kingdom, Europe, and the United States.

Flawless balance sheet with reasonable growth potential.