Advertisement

The harsh reality for Benchmark Holdings plc (LON:BMK) shareholders is that its auditors, KPMG LLP - Klynveld Peat Marwick Goerdeler, expressed doubts about its ability to continue as a going concern, in its reported results to September 2021. This means that, based on the financial results to that date, the company arguably should raise capital, or otherwise strengthen the balance sheet, as soon as possible.

Given its situation, it may not be in a good position to raise capital on favorable terms. So current risks on the balance sheet could have a big impact on how shareholders fare from here. Debt is always a risk factor in these cases, as creditors could be in a position to wind up the company, in the worst case scenario.

See our latest analysis for Benchmark Holdings

What Is Benchmark Holdings's Net Debt?

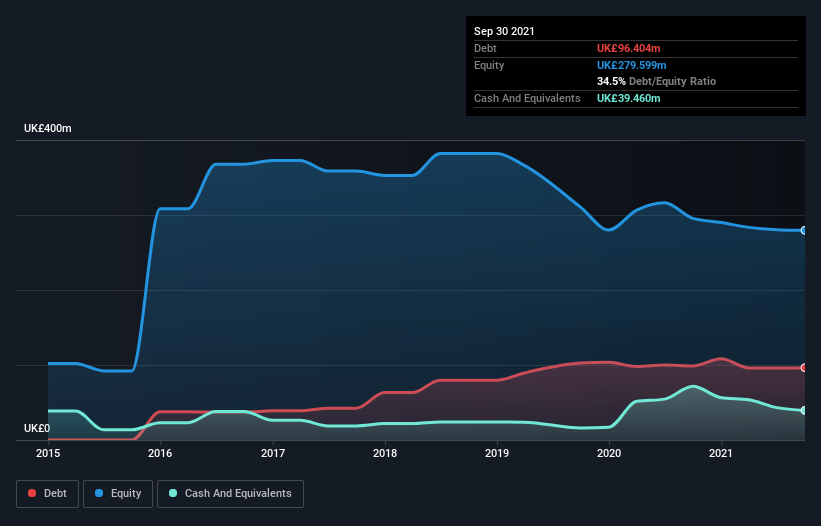

As you can see below, Benchmark Holdings had UK£96.4m of debt, at September 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of UK£39.5m, its net debt is less, at about UK£56.9m.

A Look At Benchmark Holdings' Liabilities

Zooming in on the latest balance sheet data, we can see that Benchmark Holdings had liabilities of UK£63.5m due within 12 months and liabilities of UK£138.9m due beyond that. On the other hand, it had cash of UK£39.5m and UK£34.4m worth of receivables due within a year. So its liabilities total UK£128.6m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Benchmark Holdings is worth UK£429.3m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Benchmark Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Benchmark Holdings reported revenue of UK£125m, which is a gain of 18%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months Benchmark Holdings produced an earnings before interest and tax (EBIT) loss. Indeed, it lost UK£7.3m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through UK£17m of cash over the last year. So suffice it to say we do consider the stock to be risky. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because companies should always make sure the auditor has confidence that the company will continue as a going concern, in our view. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Benchmark Holdings , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Benchmark Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:BMK

Benchmark Holdings

Engages in the provision of technical services, products, and specialist knowledge that supports the development of food and farming industries.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor