- United Kingdom

- /

- Consumer Durables

- /

- LSE:CRN

Yellow Cake And 2 Other Undiscovered Gems In The UK Market

Reviewed by Simply Wall St

Over the last 7 days, the United Kingdom market has remained flat, but over the past 12 months, it has risen by 6.8%, with earnings expected to grow by 14% per annum over the next few years. In this promising environment, identifying lesser-known stocks with strong growth potential can be particularly rewarding for investors.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

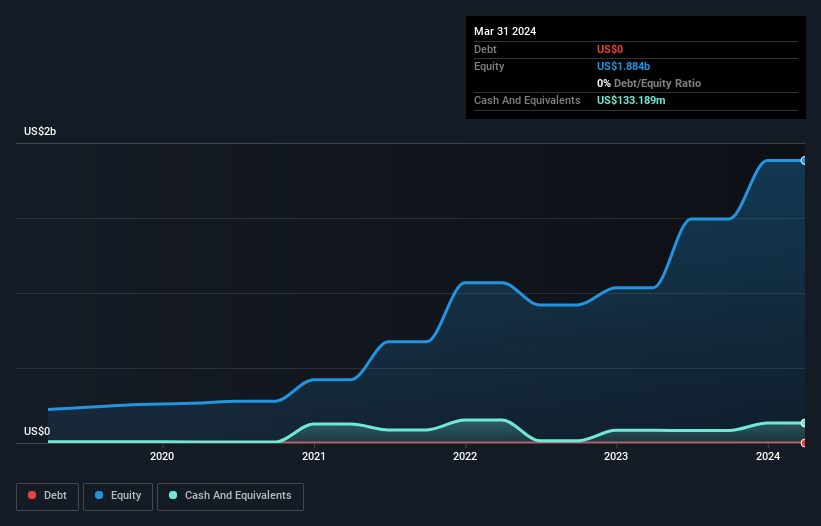

Yellow Cake (AIM:YCA)

Simply Wall St Value Rating: ★★★★★★

Overview: Yellow Cake plc operates in the uranium sector with a market cap of £1.14 billion.

Operations: Yellow Cake plc generates revenue primarily through holding U3O8 for long-term capital appreciation, amounting to $735.02 million.

Yellow Cake has recently reported impressive financial results, with revenue reaching US$735.02 million for the year ending March 31, 2024, a stark contrast to the negative revenue of US$96.9 million a year prior. Net income surged to US$727.01 million from a net loss of US$102.94 million last year. Despite shareholders experiencing dilution over the past year, YCA remains debt-free and boasts a low price-to-earnings ratio of 2.1x compared to the UK market's 16.5x.

- Click here and access our complete health analysis report to understand the dynamics of Yellow Cake.

Evaluate Yellow Cake's historical performance by accessing our past performance report.

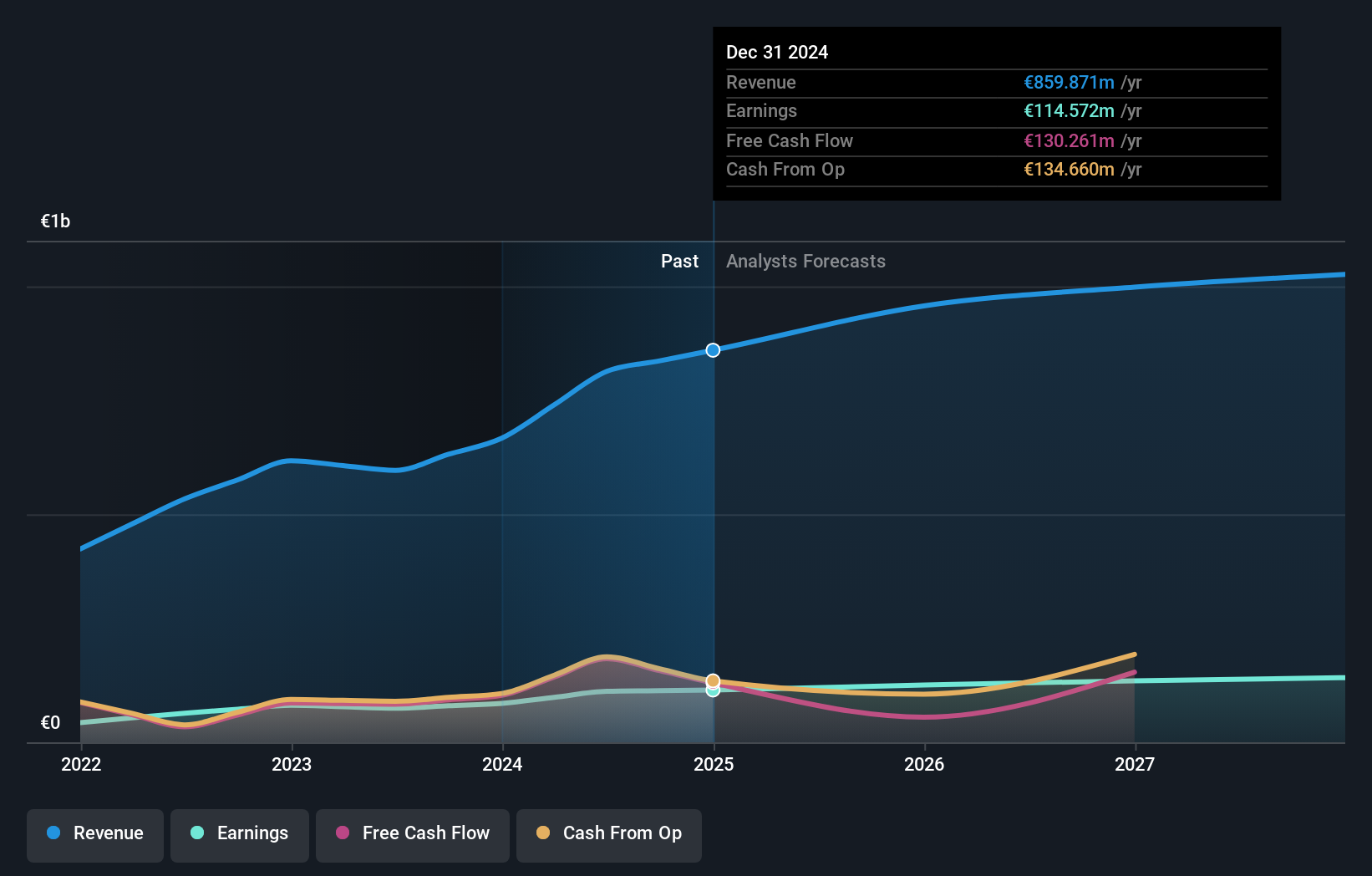

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cairn Homes plc, a holding company with a market cap of £980.21 million, operates as a home and community builder in Ireland.

Operations: Cairn Homes generates revenue primarily from building and property development, amounting to €813.40 million. The company's net profit margin is %.

Cairn Homes, a notable player in the UK market, has shown impressive growth with earnings surging 49.5% over the past year and outperforming its industry. The company’s debt to equity ratio rose from 31.3% to 39.1% in five years, but its net debt to equity remains satisfactory at 20.7%. Trading at a P/E ratio of 10.4x, Cairn offers good value compared to the UK market average of 16.5x and recently repurchased shares worth €70 million under its buyback program announced in March 2023.

- Unlock comprehensive insights into our analysis of Cairn Homes stock in this health report.

Review our historical performance report to gain insights into Cairn Homes''s past performance.

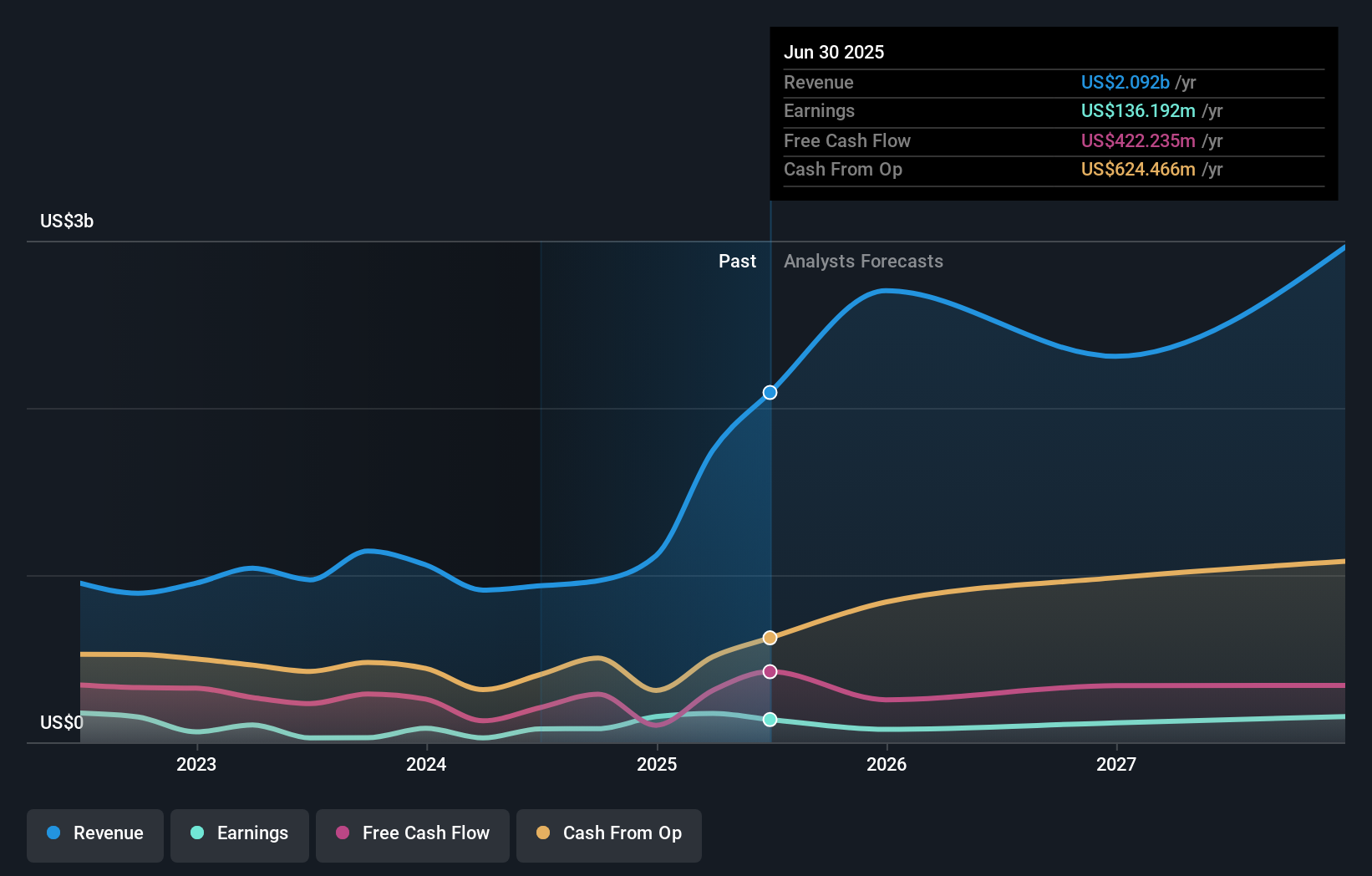

Seplat Energy (LSE:SEPL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Seplat Energy Plc engages in oil and gas exploration, production, and gas processing activities across Nigeria, the Bahamas, Italy, Switzerland, Barbados, and England with a market cap of £1.11 billion.

Operations: Seplat Energy generates revenue primarily from oil ($815.03 million) and gas ($120.87 million). The company operates across multiple countries, including Nigeria, the Bahamas, Italy, Switzerland, Barbados, and England.

Seplat Energy's recent performance highlights its potential as an undervalued player in the UK market. The company reported Q2 sales of US$241.82 million, up from US$216.03 million last year, and net income of US$39.72 million compared to a net loss of US$14.63 million previously. Over the past five years, Seplat's debt to equity ratio rose from 20.6% to 41.5%. Notably, earnings surged by 207%, far outpacing the oil and gas sector's -56%.

Taking Advantage

- Discover the full array of 80 UK Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:CRN

Cairn Homes

A holding company, operates as a home and community builder in Ireland.

Solid track record with excellent balance sheet.