Advertisement

- United Kingdom

- /

- Oil and Gas

- /

- LSE:BISI

We Think Shareholders May Want To Consider A Review Of Bisichi PLC's (LON:BISI) CEO Compensation Package

Key Insights

- Bisichi's Annual General Meeting to take place on 18th of June

- CEO Andrew Heller's total compensation includes salary of UK£850.0k

- The total compensation is 287% higher than the average for the industry

- Bisichi's EPS declined by 9.2% over the past three years while total shareholder loss over the past three years was 42%

Shareholders will probably not be too impressed with the underwhelming results at Bisichi PLC (LON:BISI) recently. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 18th of June. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. We present the case why we think CEO compensation is out of sync with company performance.

Check out our latest analysis for Bisichi

Comparing Bisichi PLC's CEO Compensation With The Industry

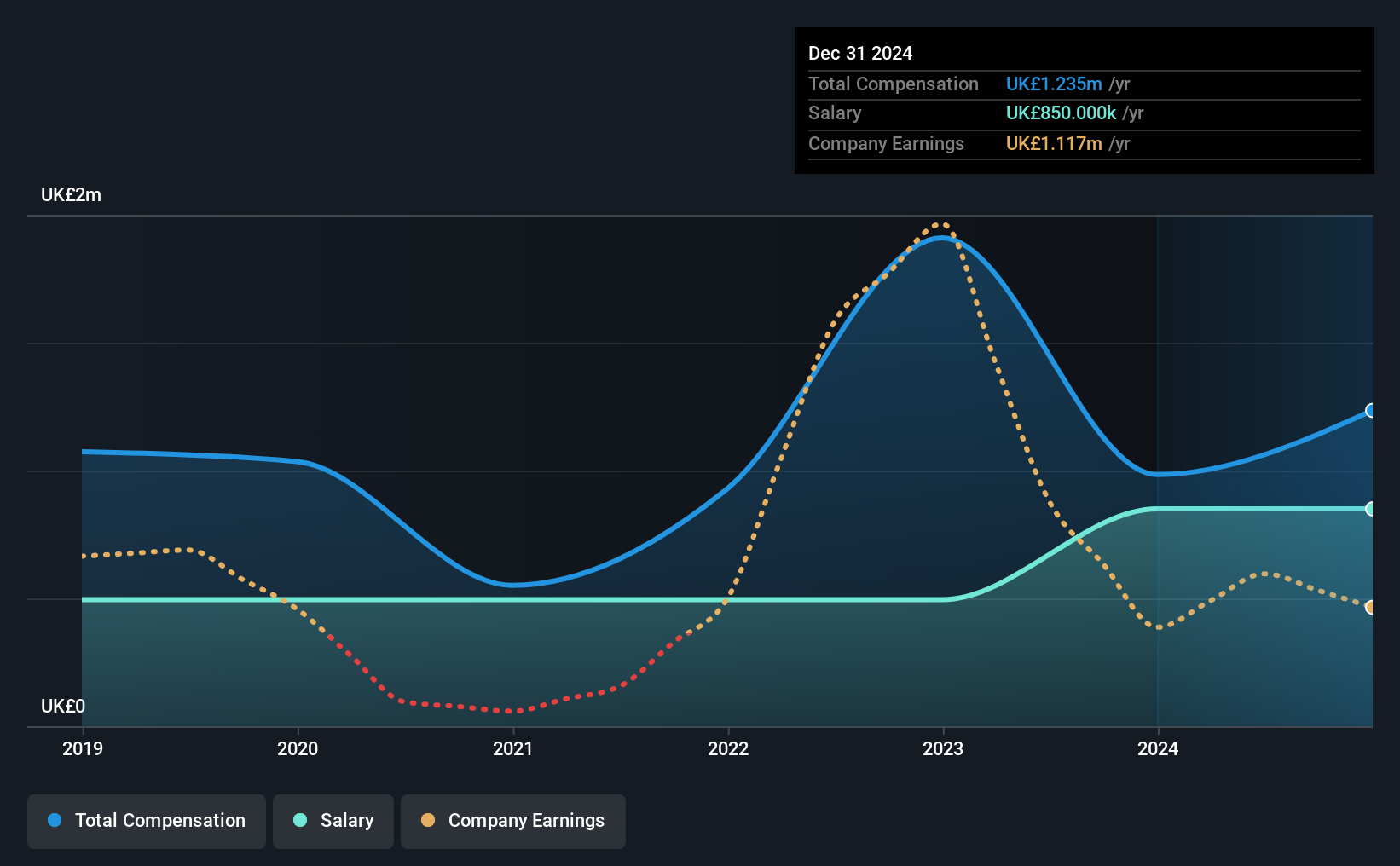

Our data indicates that Bisichi PLC has a market capitalization of UK£10m, and total annual CEO compensation was reported as UK£1.2m for the year to December 2024. We note that's an increase of 26% above last year. In particular, the salary of UK£850.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the British Oil and Gas industry with market capitalizations below UK£148m, we found that the median total CEO compensation was UK£319k. Hence, we can conclude that Andrew Heller is remunerated higher than the industry median. Furthermore, Andrew Heller directly owns UK£804k worth of shares in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£850k | UK£850k | 69% |

| Other | UK£385k | UK£134k | 31% |

| Total Compensation | UK£1.2m | UK£984k | 100% |

Talking in terms of the industry, salary represented approximately 65% of total compensation out of all the companies we analyzed, while other remuneration made up 35% of the pie. There isn't a significant difference between Bisichi and the broader market, in terms of salary allocation in the overall compensation package. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Bisichi PLC's Growth Numbers

Bisichi PLC has reduced its earnings per share by 9.2% a year over the last three years. Its revenue is up 6.2% over the last year.

Few shareholders would be pleased to read that EPS have declined. The fairly low revenue growth fails to impress given that the EPS is down. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Bisichi PLC Been A Good Investment?

The return of -42% over three years would not have pleased Bisichi PLC shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 2 warning signs for Bisichi that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Bisichi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BISI

Bisichi

Engages in coal mining and processing activities in the United Kingdom and South Africa.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor