Advertisement

- United Kingdom

- /

- Professional Services

- /

- AIM:DATA

3 UK Stocks Estimated To Be 21.1% To 46.6% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 closing lower due to weak trade data from China and declining commodity prices affecting major companies. In this environment of uncertainty, investors may be on the lookout for stocks that are undervalued relative to their intrinsic value, as these can present potential opportunities despite broader market fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Begbies Traynor Group (AIM:BEG) | £0.916 | £1.68 | 45.6% |

| Savills (LSE:SVS) | £9.27 | £16.53 | 43.9% |

| Gooch & Housego (AIM:GHH) | £3.77 | £7.13 | 47.1% |

| Aptitude Software Group (LSE:APTD) | £2.79 | £5.13 | 45.7% |

| GlobalData (AIM:DATA) | £1.775 | £3.32 | 46.6% |

| On the Beach Group (LSE:OTB) | £2.65 | £4.78 | 44.5% |

| Entain (LSE:ENT) | £6.376 | £12.03 | 47% |

| ECO Animal Health Group (AIM:EAH) | £0.695 | £1.28 | 45.6% |

| Kromek Group (AIM:KMK) | £0.051 | £0.10 | 49.7% |

| Ibstock (LSE:IBST) | £1.80 | £3.24 | 44.5% |

Here's a peek at a few of the choices from the screener.

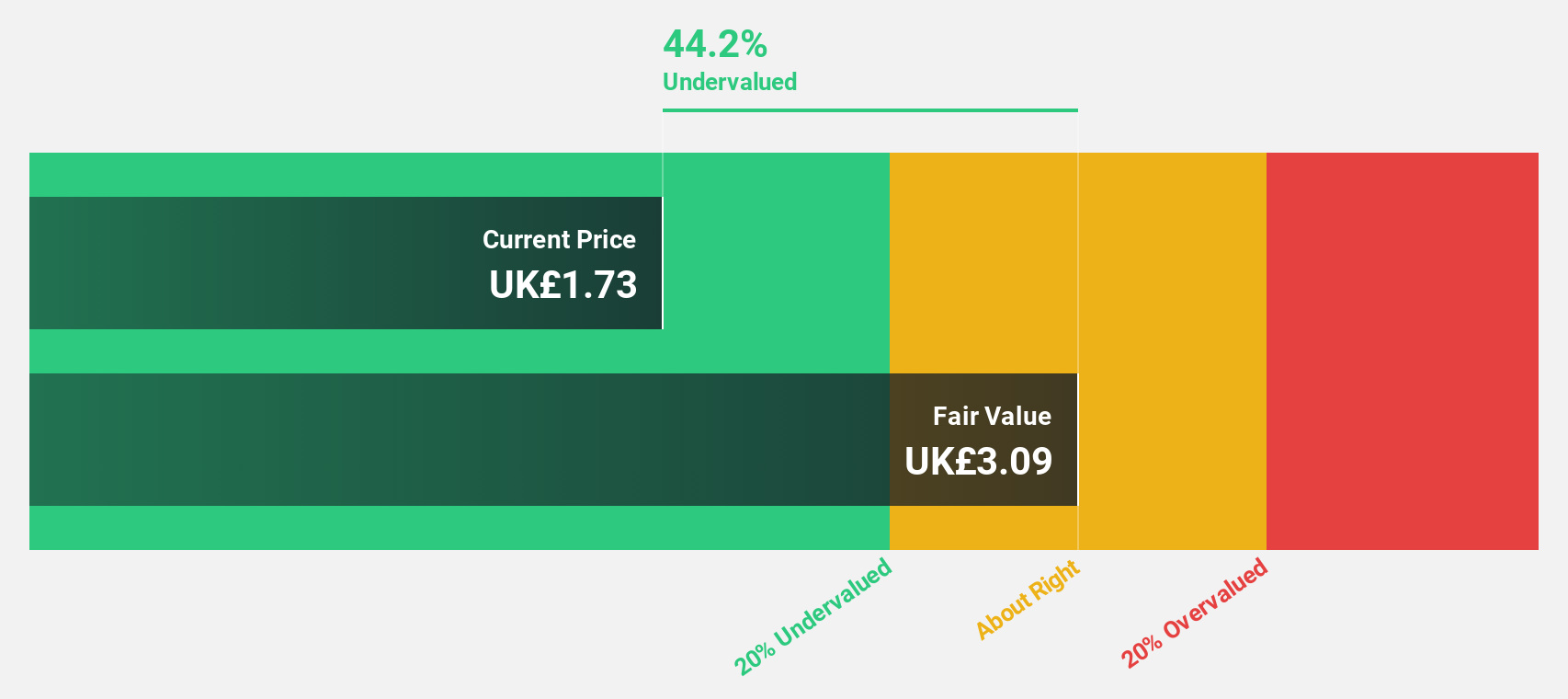

GlobalData (AIM:DATA)

Overview: GlobalData Plc, along with its subsidiaries, offers business information through proprietary data, analytics, and insights across Europe, North America, and the Asia Pacific with a market cap of £1.35 billion.

Operations: The company's revenue is derived from its Data, Analytics and Insights segments, with £109.40 million from Healthcare and £176.10 million from Non-Healthcare sectors.

Estimated Discount To Fair Value: 46.6%

GlobalData is trading at £1.78, significantly below its estimated fair value of £3.32, indicating it may be undervalued based on cash flows. Despite a volatile share price and a reduced dividend, the company is forecast to grow earnings by 21% annually, outpacing the UK market's growth rate. Recent M&A interest from ICG and KKR highlights potential strategic value, while an active share buyback program aims to enhance shareholder returns amidst plans to move to the Main Market.

- Our earnings growth report unveils the potential for significant increases in GlobalData's future results.

- Delve into the full analysis health report here for a deeper understanding of GlobalData.

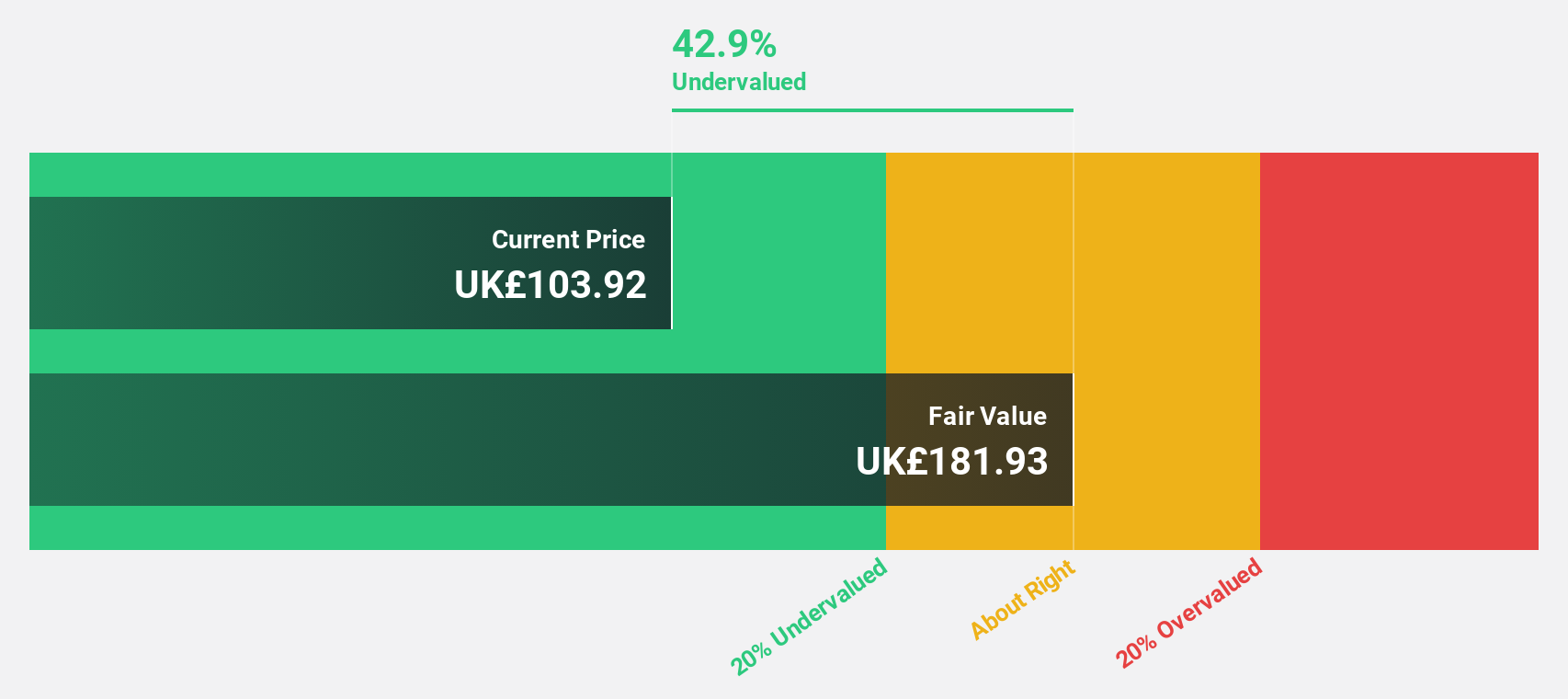

AstraZeneca (LSE:AZN)

Overview: AstraZeneca PLC is a biopharmaceutical company engaged in the discovery, development, manufacture, and commercialization of prescription medicines, with a market cap of approximately £166.35 billion.

Operations: The company's revenue primarily stems from its biopharmaceuticals segment, which generated $54.98 billion.

Estimated Discount To Fair Value: 42.9%

AstraZeneca is currently trading at £107.28, well below its estimated fair value of £187.75, highlighting potential undervaluation based on cash flows. Despite a recent decision to discontinue the CAPItello-280 trial, AstraZeneca's earnings are projected to grow 14.5% annually, surpassing UK market averages. The company reported strong Q1 results with revenue of US$13.59 billion and net income of US$2.92 billion, reflecting robust financial health despite high debt levels and large one-off items impacting results.

- Our growth report here indicates AstraZeneca may be poised for an improving outlook.

- Navigate through the intricacies of AstraZeneca with our comprehensive financial health report here.

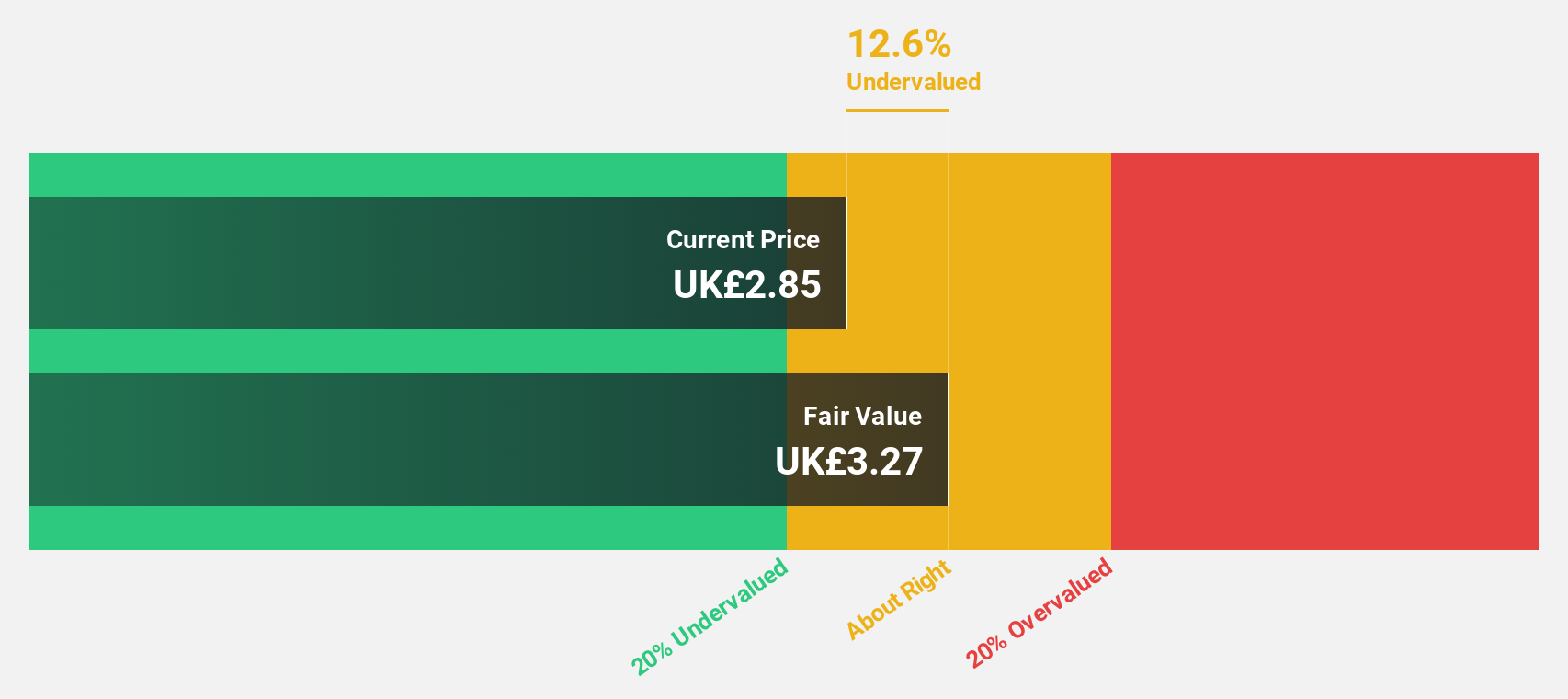

Bridgepoint Group (LSE:BPT)

Overview: Bridgepoint Group plc is a private equity and private credit firm focusing on middle market, lower mid-market, small mid cap, small cap, growth capital, buyouts investments, syndicate debt, infrastructure, direct lending and credit opportunities in private credit investments with a market cap of £2.21 billion.

Operations: The company's revenue is derived from four main segments: Credit (£75.70 million), Infrastructure (£72.50 million), and Private Equity (£275.60 million).

Estimated Discount To Fair Value: 21.1%

Bridgepoint Group is trading at £2.67, over 20% below its estimated fair value of £3.39, indicating potential undervaluation based on cash flows. Despite a volatile share price and lower profit margins compared to the previous year, earnings are forecast to grow significantly at 32.63% annually, outpacing the UK market average. Recent revenue growth and a proposed dividend increase reflect positive momentum, although large one-off items have impacted financial results.

- Insights from our recent growth report point to a promising forecast for Bridgepoint Group's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Bridgepoint Group.

Key Takeaways

- Gain an insight into the universe of 52 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:DATA

GlobalData

Operates as a data, insight, and technology company in Europe, North America, and the Asia Pacific.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor