Advertisement

- United Kingdom

- /

- Diversified Financial

- /

- AIM:TIME

With EPS Growth And More, Time Finance (LON:TIME) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Time Finance (LON:TIME). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Time Finance

Time Finance's Improving Profits

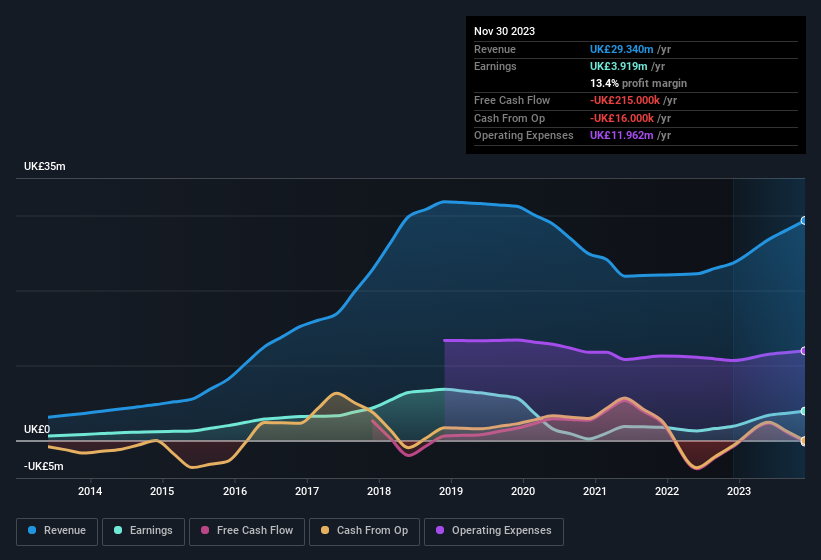

Over the last three years, Time Finance has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. So it would be better to isolate the growth rate over the last year for our analysis. Impressively, Time Finance's EPS catapulted from UK£0.02 to UK£0.043, over the last year. It's a rarity to see 110% year-on-year growth like that.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. It's noted that Time Finance's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note Time Finance achieved similar EBIT margins to last year, revenue grew by a solid 24% to UK£29m. That's progress.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

Time Finance isn't a huge company, given its market capitalisation of UK£41m. That makes it extra important to check on its balance sheet strength.

Are Time Finance Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Not only did Time Finance insiders refrain from selling stock during the year, but they also spent UK£103k buying it. That paints the company in a nice light, as it signals that its leaders are feeling confident in where the company is heading. We also note that it was the company insider, Ronald Russell, who made the biggest single acquisition, paying UK£35k for shares at about UK£0.30 each.

Does Time Finance Deserve A Spot On Your Watchlist?

Time Finance's earnings per share growth have been climbing higher at an appreciable rate. Most growth-seeking investors will find it hard to ignore that sort of explosive EPS growth. And may very well signal a significant inflection point for the business. If this these factors intrigue you, then an addition of Time Finance to your watchlist won't go amiss. You still need to take note of risks, for example - Time Finance has 1 warning sign we think you should be aware of.

The good news is that Time Finance is not the only growth stock with insider buying. Here's a list of growth-focused companies in GB with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Time Finance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:TIME

Time Finance

Provides financial products and services to consumers and businesses in the United Kingdom.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor