Advertisement

- United Kingdom

- /

- Hospitality

- /

- LSE:ENT

It Might Not Be A Great Idea To Buy Entain Plc (LON:ENT) For Its Next Dividend

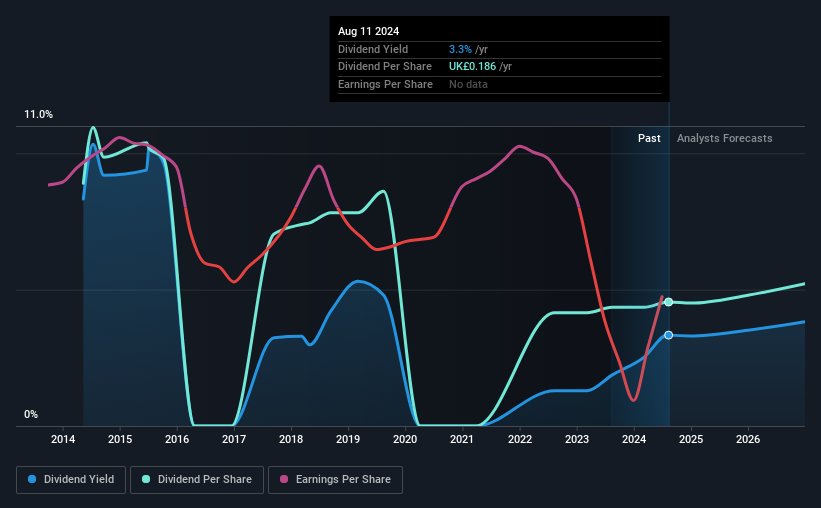

Readers hoping to buy Entain Plc (LON:ENT) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. In other words, investors can purchase Entain's shares before the 15th of August in order to be eligible for the dividend, which will be paid on the 20th of September.

The company's next dividend payment will be UK£0.093 per share. Last year, in total, the company distributed UK£0.19 to shareholders. Based on the last year's worth of payments, Entain has a trailing yield of 3.3% on the current stock price of UK£5.582. If you buy this business for its dividend, you should have an idea of whether Entain's dividend is reliable and sustainable. So we need to investigate whether Entain can afford its dividend, and if the dividend could grow.

View our latest analysis for Entain

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Entain lost money last year, so the fact that it's paying a dividend is certainly disconcerting. There might be a good reason for this, but we'd want to look into it further before getting comfortable. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If Entain didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. Over the past year it paid out 116% of its free cash flow as dividends, which is uncomfortably high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Entain reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Entain's dividend payments per share have declined at 6.5% per year on average over the past 10 years, which is uninspiring. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Get our latest analysis on Entain's balance sheet health here.

To Sum It Up

Has Entain got what it takes to maintain its dividend payments? It's hard to get used to Entain paying a dividend despite reporting a loss over the past year. Worse, the dividend was not well covered by cash flow. Bottom line: Entain has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

With that being said, if you're still considering Entain as an investment, you'll find it beneficial to know what risks this stock is facing. Our analysis shows 1 warning sign for Entain and you should be aware of this before buying any shares.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Entain might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:ENT

Entain

Operates as a sports-betting and gaming company in the United Kingdom, Ireland, Italy, rest of Europe, Australia, New Zealand, and internationally.

Reasonable growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|62.4% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.2% undervalued

ZW

Community Contributor