Stock Analysis

- United Kingdom

- /

- Hospitality

- /

- LSE:DPEU

Should You Be Adding DP Eurasia (LON:DPEU) To Your Watchlist Today?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like DP Eurasia (LON:DPEU). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for DP Eurasia

DP Eurasia's Improving Profits

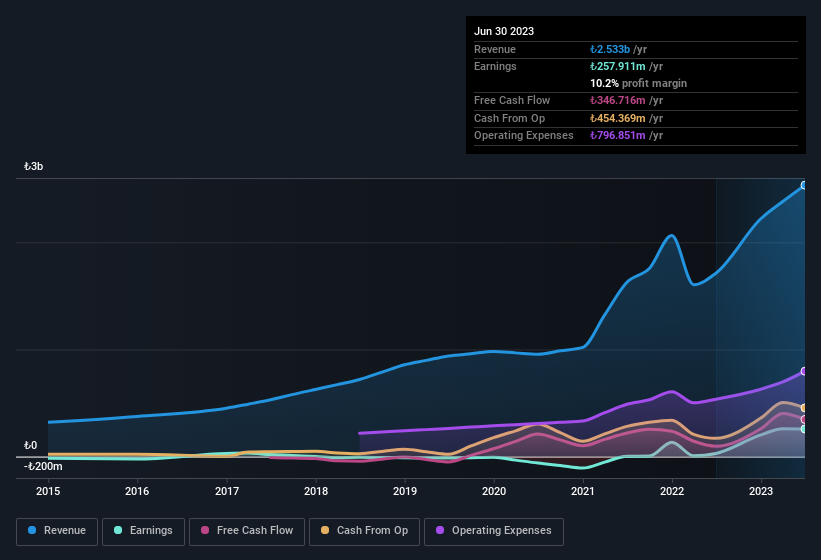

Investors and investment funds chase profits, and that means share prices tend rise with positive earnings per share (EPS) outcomes. Which is why EPS growth is looked upon so favourably. It's an outstanding feat for DP Eurasia to have grown EPS from ₺0.20 to ₺1.76 in just one year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future. But the key is discerning whether something profound has changed, or if this is a just a one-off boost.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. DP Eurasia shareholders can take confidence from the fact that EBIT margins are up from 1.9% to 9.2%, and revenue is growing. Both of which are great metrics to check off for potential growth.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

DP Eurasia isn't a huge company, given its market capitalisation of UK£97m. That makes it extra important to check on its balance sheet strength.

Are DP Eurasia Insiders Aligned With All Shareholders?

It should give investors a sense of security owning shares in a company if insiders also own shares, creating a close alignment their interests. DP Eurasia followers will find comfort in knowing that insiders have a significant amount of capital that aligns their best interests with the wider shareholder group. Insider share holdings at DP Eurasia are collectively valued at ₺18m, which amounts to 19% of the business. That is a valuable holding, but it's worth noting the CEO has a took home a ₺5.1m salary in the year to December 2022.

Does DP Eurasia Deserve A Spot On Your Watchlist?

DP Eurasia's earnings per share growth have been climbing higher at an appreciable rate. That sort of growth is nothing short of eye-catching, and the large investment held by insiders should certainly brighten the view of the company. The hope is, of course, that the strong growth marks a fundamental improvement in the business economics. So at the surface level, DP Eurasia is worth putting on your watchlist; after all, shareholders do well when the market underestimates fast growing companies. However, before you get too excited we've discovered 2 warning signs for DP Eurasia (1 is a bit concerning!) that you should be aware of.

Although DP Eurasia certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see insider buying, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're helping make it simple.

Find out whether DP Eurasia is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:DPEU

DP Eurasia

DP Eurasia N.V., together with its subsidiaries, engages in the operation of corporate-owned and franchised stores under the Domino’s Pizza brand name in Turkey, Russia, Azerbaijan, and Georgia.

Acceptable track record with worrying balance sheet.