- United Kingdom

- /

- Banks

- /

- LSE:TBCG

3 UK Growth Stocks With Up To 38% Insider Ownership

Reviewed by Simply Wall St

Over the last 7 days, the UK market has remained flat, but it has shown an 8.8% increase over the past year, with earnings forecasted to grow by 14% annually. In this context of steady growth and optimistic projections, identifying companies with high insider ownership can be a strategic approach as it often signals strong alignment between management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 82.5% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| Gaming Realms (AIM:GMR) | 20.1% | 22.1% |

| LSL Property Services (LSE:LSL) | 10.8% | 28.2% |

| Judges Scientific (AIM:JDG) | 10.6% | 23% |

| Enteq Technologies (AIM:NTQ) | 20% | 53.8% |

| Facilities by ADF (AIM:ADF) | 22.7% | 144.7% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 29.0% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.6% |

Let's explore several standout options from the results in the screener.

RWS Holdings (AIM:RWS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: RWS Holdings plc offers technology-enabled language, content, and intellectual property services with a market cap of £589.90 million.

Operations: The company's revenue is derived from four main segments: IP Services (£105.10 million), Language Services (£325.40 million), Regulated Industry (£149.40 million), and Language & Content Technology (£137.90 million).

Insider Ownership: 24.6%

RWS Holdings is forecast to achieve profitability within three years, surpassing average market growth expectations. Despite trading at 72.9% below estimated fair value, its dividend yield of 7.66% isn't well supported by earnings or cash flow. Revenue growth is projected at 4.2% annually, slightly above the UK market rate but below high-growth benchmarks. Recent leadership changes include Jacqui Taylor as Chief People Officer and Mark Lawyer leading Regulated Industries & Linguistic AI initiatives, potentially enhancing strategic direction and operational efficiency.

- Click here and access our complete growth analysis report to understand the dynamics of RWS Holdings.

- Insights from our recent valuation report point to the potential undervaluation of RWS Holdings shares in the market.

Hochschild Mining (LSE:HOC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hochschild Mining plc is a precious metals company involved in the exploration, mining, processing, and sale of gold and silver across several countries including Peru, Argentina, the United States, Canada, Brazil, and Chile with a market cap of £1.12 billion.

Operations: The company's revenue is primarily derived from its San Jose segment, contributing $266.70 million, and its Inmaculada segment, generating $451.91 million.

Insider Ownership: 38.4%

Hochschild Mining recently became profitable, reporting a net income of US$39.52 million for H1 2024, contrasting with a loss last year. Despite high debt levels and share price volatility, earnings are forecast to grow significantly at 49.8% annually, outpacing the UK market average. Revenue growth is projected at 8.1% per year, faster than the market but below high-growth benchmarks. The stock trades at 57.3% below its estimated fair value without recent insider trading activity noted.

- Dive into the specifics of Hochschild Mining here with our thorough growth forecast report.

- The analysis detailed in our Hochschild Mining valuation report hints at an inflated share price compared to its estimated value.

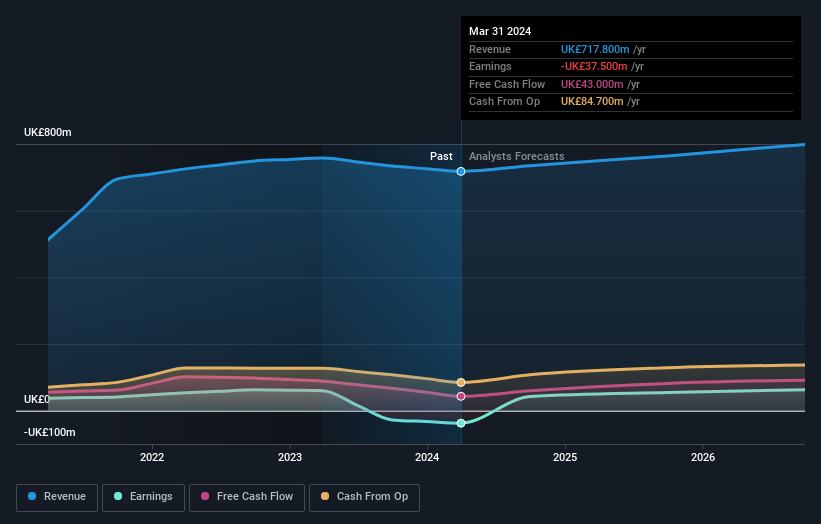

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates in Georgia, Azerbaijan, and Uzbekistan offering banking, leasing, insurance, brokerage, and card processing services to both corporate and individual customers with a market cap of £1.47 billion.

Operations: The company's revenue segments include GEL 2.13 billion from segment adjustments and GEL 236.42 million from Uzbekistan operations.

Insider Ownership: 17.6%

TBC Bank Group shows strong growth potential with earnings expected to increase 15.3% annually, outpacing the UK market average of 14%. Revenue is projected to grow at 18.9% per year, surpassing the market's 3.6%. The stock trades at a significant discount to its estimated fair value and offers good relative value compared to peers. Recent executive changes include appointing Giorgi Giguashvili as Company Secretary, enhancing corporate governance expertise. No recent insider trading activity was reported.

- Get an in-depth perspective on TBC Bank Group's performance by reading our analyst estimates report here.

- The valuation report we've compiled suggests that TBC Bank Group's current price could be quite moderate.

Taking Advantage

- Unlock more gems! Our Fast Growing UK Companies With High Insider Ownership screener has unearthed 59 more companies for you to explore.Click here to unveil our expertly curated list of 62 Fast Growing UK Companies With High Insider Ownership.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if TBC Bank Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TBCG

TBC Bank Group

Through its subsidiaries, provides banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan.

Undervalued with excellent balance sheet and pays a dividend.