Stock Analysis

- United Kingdom

- /

- Professional Services

- /

- AIM:RWS

3 UK Growth Companies With High Insider Ownership And Earnings Growth Above 31%

Reviewed by Simply Wall St

Amidst a backdrop of fluctuating global markets and specific challenges within the UK economy, such as a stagnant housing market and calls for stronger industrial strategies, investors may find solace in growth companies with high insider ownership. These firms not only demonstrate confidence from those closest to the company but also offer potential resilience and growth in uncertain economic times.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Plant Health Care (AIM:PHC) | 26.4% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 124.5% |

| Getech Group (AIM:GTC) | 17.2% | 86.1% |

| Gulf Keystone Petroleum (LSE:GKP) | 10.7% | 47.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 25.5% |

| Velocity Composites (AIM:VEL) | 28.5% | 143.4% |

| TEAM (AIM:TEAM) | 25.8% | 58.6% |

| Judges Scientific (AIM:JDG) | 11.5% | 25.3% |

| Afentra (AIM:AET) | 38.3% | 64.4% |

| Mothercare (AIM:MTC) | 15.1% | 41.2% |

Underneath we present a selection of stocks filtered out by our screen.

Loungers (AIM:LGRS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Loungers plc operates cafés, bars, and restaurants under the Lounge and Cosy Club brand names in England and Wales, with a market capitalization of approximately £293.83 million.

Operations: The company generates £310.80 million in revenue from its café bars and restaurants.

Insider Ownership: 13.9%

Earnings Growth Forecast: 31.4% p.a.

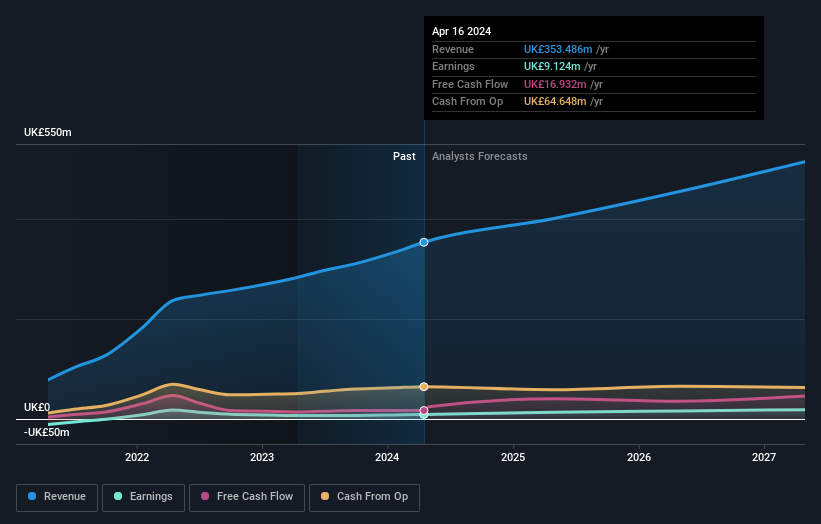

Loungers plc, despite trading 47.1% below its estimated fair value, shows robust growth prospects with earnings expected to increase significantly over the next three years, outpacing the UK market's average. However, its profit margins have dipped from last year and its return on equity is projected to remain low. Recent strategic executive changes and a record revenue of £353.5 million for FY2024 underscore a commitment to scaling operations efficiently under new leadership.

- Delve into the full analysis future growth report here for a deeper understanding of Loungers.

- The analysis detailed in our Loungers valuation report hints at an deflated share price compared to its estimated value.

RWS Holdings (AIM:RWS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: RWS Holdings plc specializes in technology-enabled language, content, and intellectual property services with a market capitalization of approximately £0.73 billion.

Operations: The company specializes in providing services across technology-enabled language, content, and intellectual property sectors.

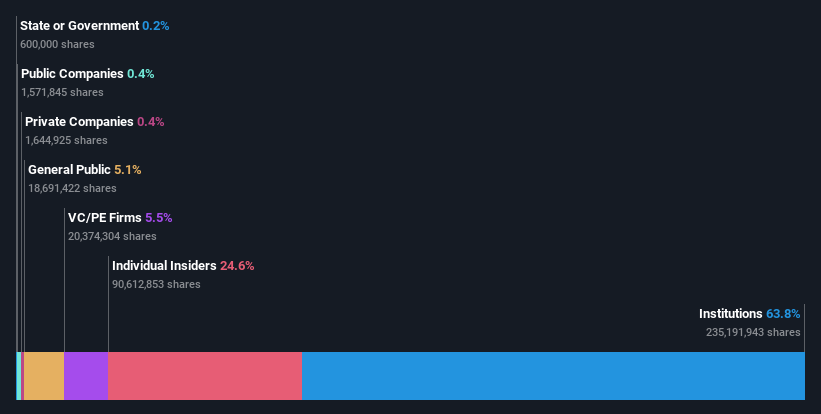

Insider Ownership: 24.6%

Earnings Growth Forecast: 67.4% p.a.

RWS Holdings, currently trading at a significant discount to its estimated fair value, is poised for profitability with expected growth in earnings by 67.35% annually over the next three years. Despite this, its dividend coverage is weak due to insufficient earnings and cash flows. Recent initiatives like the launch of HAI, a digital translation platform, demonstrate innovation but revenue growth projections remain modest at 4.2% annually, slightly above the UK market average of 3.7%. Moreover, insider ownership does not show significant buying activity recently which might concern investors looking for aligned interests with management.

- Click here and access our complete growth analysis report to understand the dynamics of RWS Holdings.

- Upon reviewing our latest valuation report, RWS Holdings' share price might be too pessimistic.

International Workplace Group (LSE:IWG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Workplace Group plc operates globally, offering workspace solutions across the Americas, Europe, the Middle East, Africa, and Asia Pacific with a market capitalization of approximately £1.80 billion.

Operations: The company generates revenue primarily through its operations in the Americas (£1.05 billion), Europe, the Middle East, and Africa (£1.32 billion), Asia Pacific (£273 million), and Worka (£319 million).

Insider Ownership: 25.2%

Earnings Growth Forecast: 108.2% p.a.

International Workplace Group plc, transitioning into profitability, is expected to see earnings surge by 108.16% annually over the next three years. Although revenue growth at 7.8% per year is modest compared to some peers, it outpaces the UK market average of 3.7%. Insider activity shows more buying than selling recently, though not in large volumes, suggesting cautious optimism among insiders. Analysts predict a potential stock price increase of 29.1%, underscoring a positive outlook despite a forecasted low return on equity of 11.6%.

- Take a closer look at International Workplace Group's potential here in our earnings growth report.

- The valuation report we've compiled suggests that International Workplace Group's current price could be quite moderate.

Make It Happen

- Navigate through the entire inventory of 64 Fast Growing UK Companies With High Insider Ownership here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether RWS Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:RWS

RWS Holdings

Provides technology-enabled language, content, and intellectual property (IP) services.

Flawless balance sheet, undervalued and pays a dividend.