- United Kingdom

- /

- Healthtech

- /

- AIM:CRW

UK Growth Stocks With High Insider Ownership For November 2024

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 and FTSE 250 indices face downward pressure due to weak trade data from China, investors are increasingly looking for resilient growth opportunities within the market. In such challenging times, companies with high insider ownership can be appealing as they often indicate a strong alignment of interests between management and shareholders, potentially offering stability amidst broader economic uncertainties.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 80.4% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| LSL Property Services (LSE:LSL) | 10.7% | 28.2% |

| Facilities by ADF (AIM:ADF) | 12.9% | 144.7% |

| Foresight Group Holdings (LSE:FSG) | 34% | 29.0% |

| Judges Scientific (AIM:JDG) | 10.6% | 23% |

| Enteq Technologies (AIM:NTQ) | 23.8% | 53.8% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.6% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 189.1% |

Here's a peek at a few of the choices from the screener.

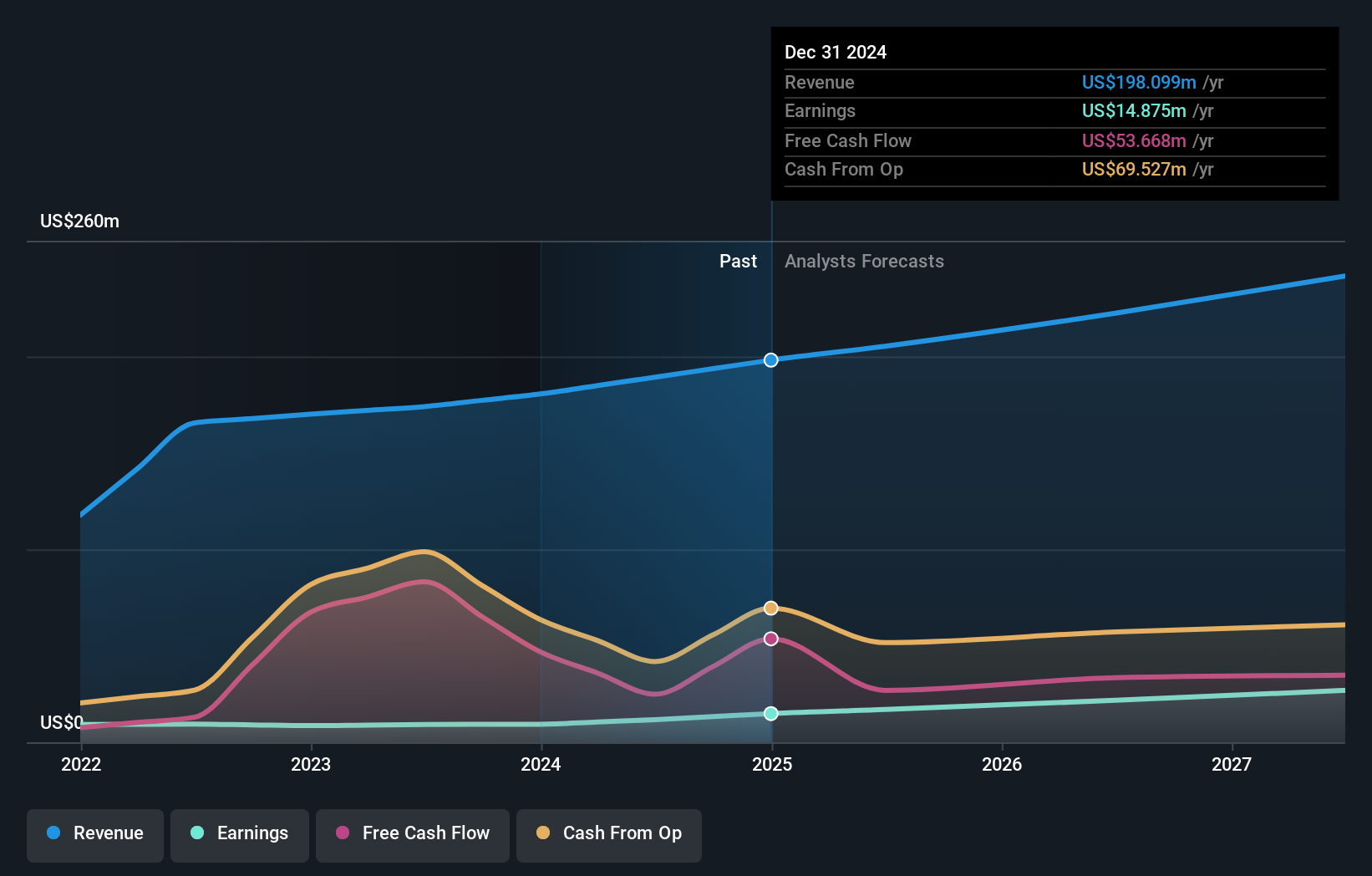

Craneware (AIM:CRW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Craneware plc, along with its subsidiaries, develops, licenses, and supports computer software for the healthcare industry in the United States and has a market cap of £706.03 million.

Operations: The company generates revenue primarily from its healthcare software segment, amounting to $189.27 million.

Insider Ownership: 16.5%

Earnings Growth Forecast: 24.3% p.a.

Craneware demonstrates potential as a growth company with high insider ownership in the UK. Despite recent substantial insider selling, its earnings are forecast to grow significantly at 24.3% annually, outpacing the UK market. The company recently announced a strategic partnership with Microsoft Azure, enhancing its cloud-based healthcare solutions and potentially driving further business growth. Although it has experienced share price volatility, Craneware's revenue is expected to grow faster than the broader market at 8.1% per year.

- Navigate through the intricacies of Craneware with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Craneware shares in the market.

Fintel (AIM:FNTL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Fintel Plc provides intermediary services and distribution channels to the retail financial services sector in the United Kingdom, with a market cap of £299.02 million.

Operations: The company generates revenue through three main segments: Research & Fintech (£24.20 million), Distribution Channels (£21.40 million), and Intermediary Services (£23.30 million).

Insider Ownership: 29.9%

Earnings Growth Forecast: 34% p.a.

Fintel shows potential as a growth company in the UK, with earnings forecasted to grow significantly at 34% annually, outpacing the market. Despite a decline in net income and profit margins compared to last year, revenue is expected to increase faster than the UK average. The company trades at 35.9% below its estimated fair value and recently increased its interim dividend by 9%, indicating confidence in future prospects despite lower current profitability.

- Dive into the specifics of Fintel here with our thorough growth forecast report.

- Our valuation report here indicates Fintel may be overvalued.

LSL Property Services (LSE:LSL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: LSL Property Services plc operates in the United Kingdom, offering business-to-business services to mortgage intermediaries and estate agency franchisees, as well as valuation services to lenders, with a market cap of £292.19 million.

Operations: The company's revenue segments include Financial Services generating £47.22 million, Surveying and Valuation contributing £79.49 million, and Estate Agency (excluding Financial Services) bringing in £30.61 million.

Insider Ownership: 10.7%

Earnings Growth Forecast: 28.2% p.a.

LSL Property Services demonstrates potential with earnings forecasted to grow significantly at 28.2% annually, surpassing the UK market average. Recent results show a return to profitability with net income of £9.95 million, up from a loss last year. Revenue is expected to increase by 12.1% annually, outpacing the broader market growth rate. Despite trading at 55.3% below estimated fair value and high insider ownership, dividend coverage remains weak due to large one-off items impacting earnings quality.

- Take a closer look at LSL Property Services' potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that LSL Property Services is priced higher than what may be justified by its financials.

Next Steps

- Gain an insight into the universe of 62 Fast Growing UK Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:CRW

Craneware

Develops, licenses, and supports computer software for the healthcare industry in the United States.

Reasonable growth potential with proven track record.