- United Kingdom

- /

- Professional Services

- /

- AIM:ELIX

Unveiling Three Undiscovered Gems In The United Kingdom With Strong Potential

Reviewed by Simply Wall St

The United Kingdom's FTSE 100 index recently faltered after weak trade data from China, reflecting broader concerns about global economic recovery. Despite these challenges, the search for promising investments continues, with certain undiscovered gems in the UK market showing strong potential due to their resilience and growth prospects in a fluctuating economy.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -3.68% | -4.07% | ★★★★★★ |

| FW Thorpe | 3.34% | 11.37% | 9.41% | ★★★★★☆ |

| Goodwin | 59.96% | 9.26% | 13.12% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

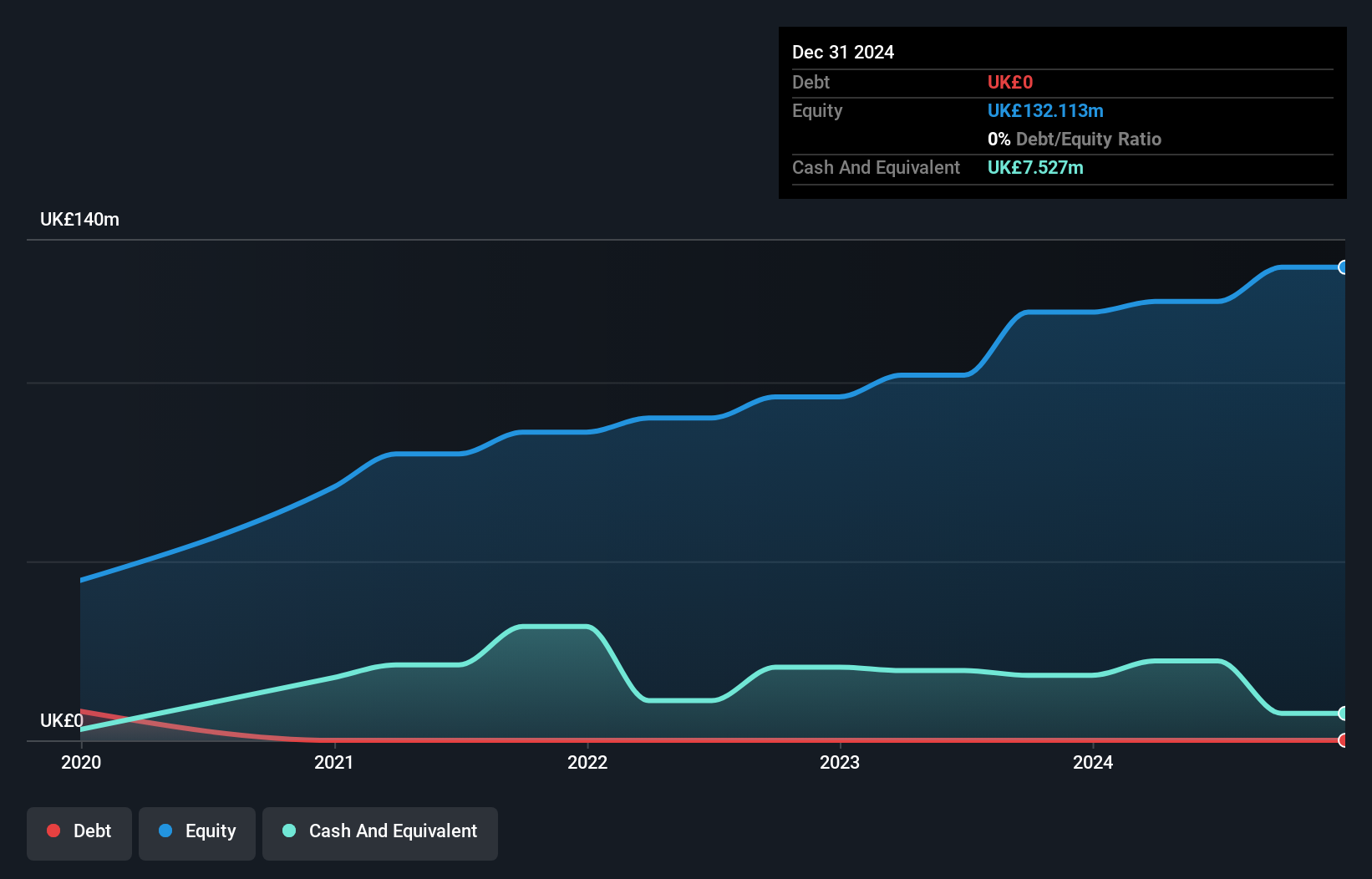

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc, with a market cap of £288.55 million, offers management consultancy services through its subsidiaries in the United Kingdom, the United States, and internationally.

Operations: Elixirr generates revenue primarily from its management consulting services, amounting to £85.89 million. The company's market cap stands at £288.55 million.

Elixirr International, a promising player in the UK market, showcases high-quality earnings and is debt-free. The company has seen significant growth, with earnings increasing by 33.9% over the past year, outpacing the Professional Services industry’s -3.9%. Recent collaborations like the one with Peak Performance Project highlight Elixirr's technological prowess and strategic acumen. Despite shareholder dilution over the past year, Elixirr trades at 59.7% below its estimated fair value, suggesting potential upside for investors.

- Take a closer look at Elixirr International's potential here in our health report.

Understand Elixirr International's track record by examining our Past report.

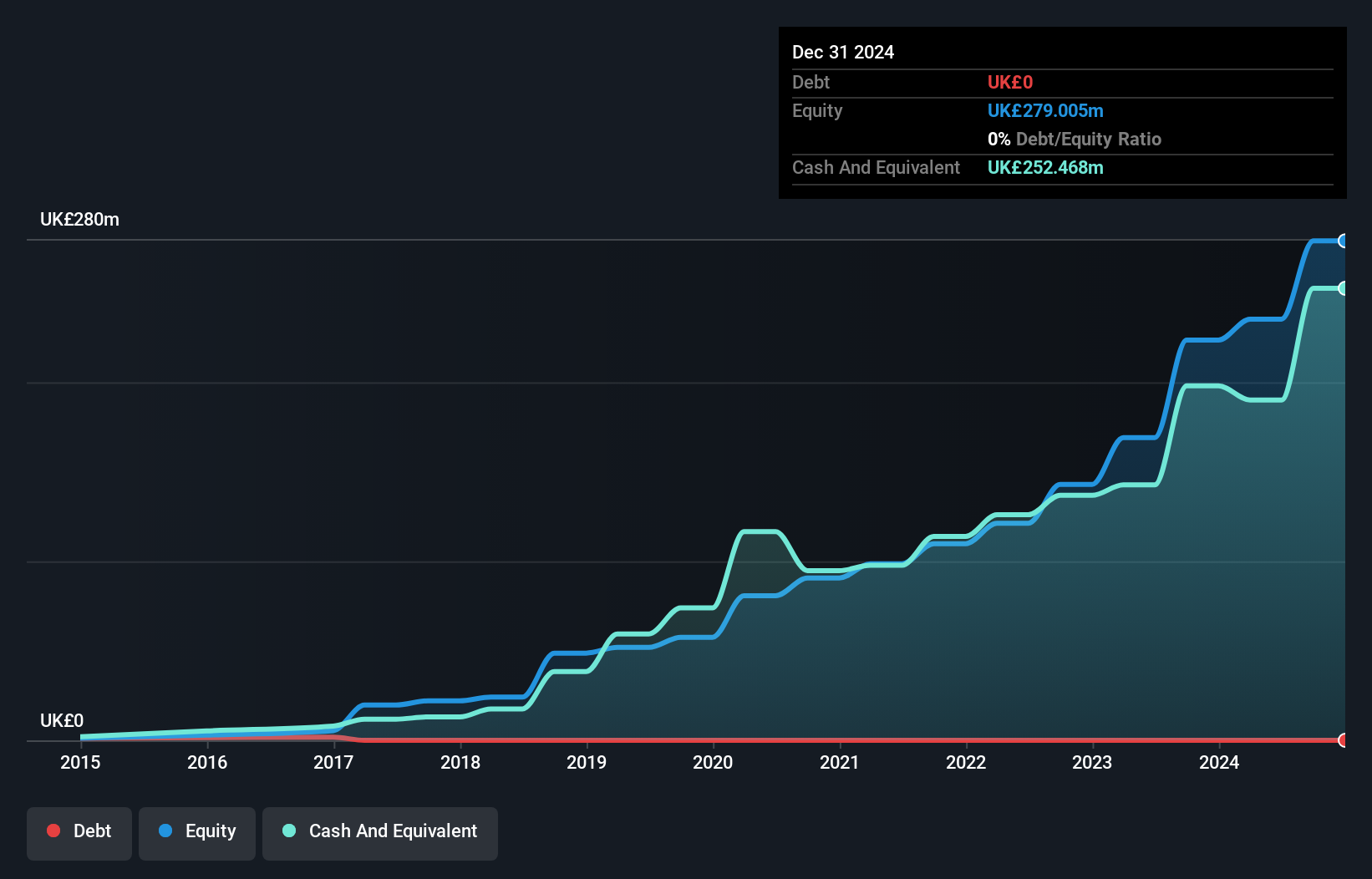

Alpha Group International (LSE:ALPH)

Simply Wall St Value Rating: ★★★★★★

Overview: Alpha Group International plc offers foreign exchange risk management and alternative banking solutions across the UK, Europe, Canada, and globally, with a market cap of approximately £1.10 billion.

Operations: Alpha Group International plc generates revenue primarily from Alpha Pay (£64.30 million), Institutional services (£61.29 million), and Corporate London operations (£45.42 million). Other significant contributions come from Corporate Amsterdam (£8.70 million) and Corporate Toronto (£4.23 million).

Alpha Group International, trading at a P/E ratio of 12.4x compared to the UK market's 17x, demonstrates strong value potential. Over the past year, its earnings surged by an impressive 130%, significantly outpacing the Capital Markets industry's modest growth of 0.4%. The company recently started a share repurchase program authorized to buy back up to 10% of its issued share capital. With no debt and consistent free cash flow positivity, Alpha Group seems well-positioned for continued growth.

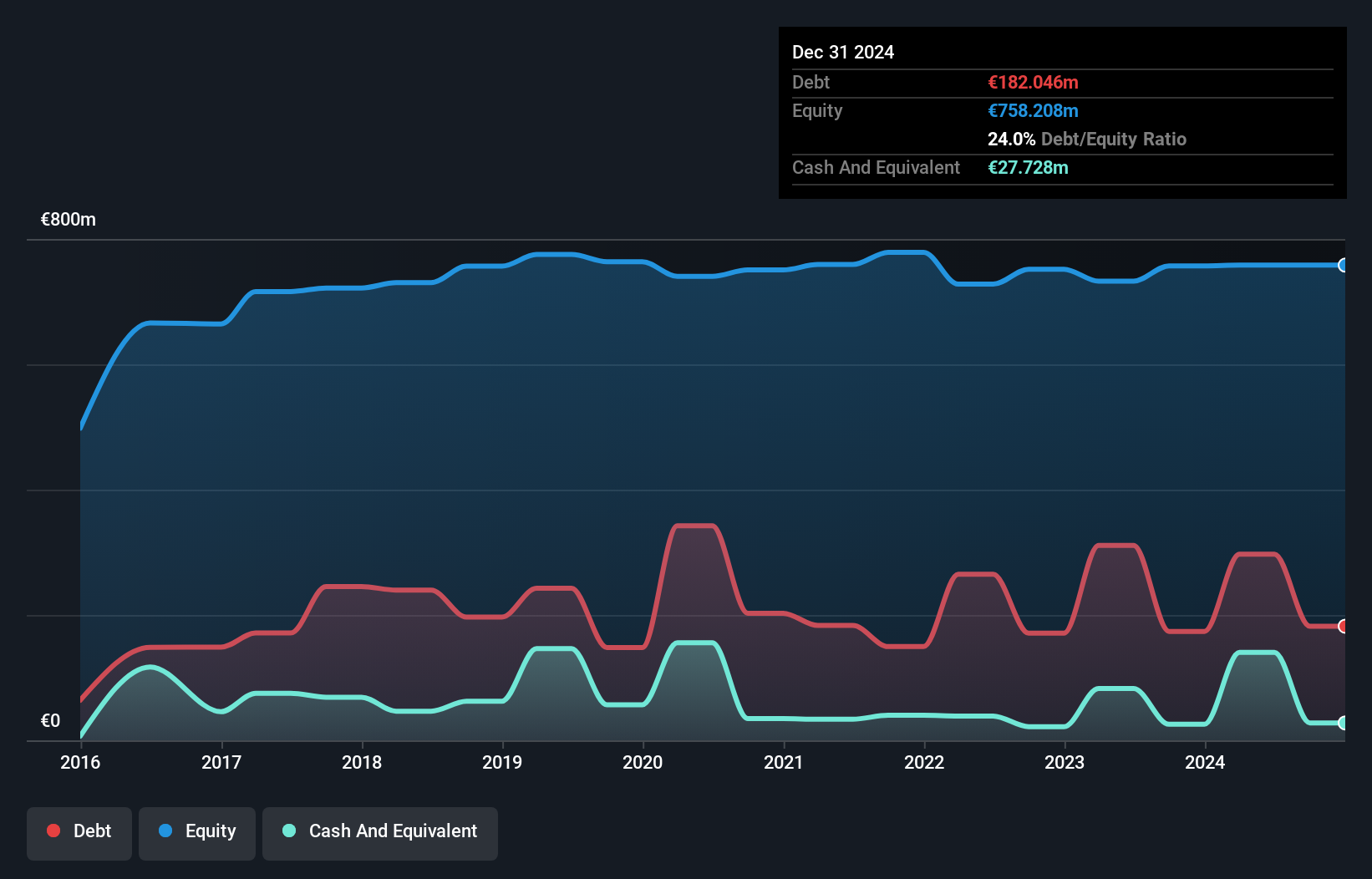

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★★

Overview: Cairn Homes plc, with a market cap of £1.02 billion, operates as a home and community builder in Ireland.

Operations: The company's primary revenue stream is derived from building and property development, generating €666.81 million.

Cairn Homes, a notable player in the UK housing market, has shown promising signs with its earnings forecast to grow at 10.91% annually. Over the past five years, CRN's debt to equity ratio improved from 26% to 23%, reflecting prudent financial management. The company boasts high-quality earnings and trades at a favorable price-to-earnings ratio of 14x compared to the UK's market average of 17x. Additionally, its interest payments are well covered by EBIT at an impressive 8.4 times coverage.

- Click to explore a detailed breakdown of our findings in Cairn Homes' health report.

Evaluate Cairn Homes' historical performance by accessing our past performance report.

Where To Now?

- Reveal the 77 hidden gems among our UK Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elixirr International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:ELIX

Elixirr International

Through its subsidiaries, provides management consultancy services in the United Kingdom, the United States, and internationally.

Very undervalued with flawless balance sheet.