Advertisement

- United Kingdom

- /

- Construction

- /

- LSE:KIE

March 2025's Undervalued Small Caps With Insider Action In Global

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a challenging landscape marked by easing U.S. inflation and ongoing trade policy uncertainties, small-cap stocks have faced significant headwinds, with indices like the Russell 2000 experiencing notable declines. Despite these pressures, opportunities may arise for investors seeking value in small-cap companies that demonstrate resilience and potential growth amid economic fluctuations.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 22.7x | 5.8x | 11.75% | ★★★★★☆ |

| Macfarlane Group | 10.5x | 0.6x | 40.48% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 45.50% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 20.89% | ★★★★★☆ |

| Minto Apartment Real Estate Investment Trust | 8.4x | 3.4x | 22.05% | ★★★★★☆ |

| Hong Leong Asia | 9.1x | 0.2x | 45.50% | ★★★★☆☆ |

| Gamma Communications | 21.5x | 2.2x | 38.57% | ★★★★☆☆ |

| Franchise Brands | 39.4x | 2.0x | 25.13% | ★★★★☆☆ |

| Sing Investments & Finance | 7.3x | 3.7x | 36.22% | ★★★★☆☆ |

| Saturn Oil & Gas | 6.9x | 0.5x | -34.05% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

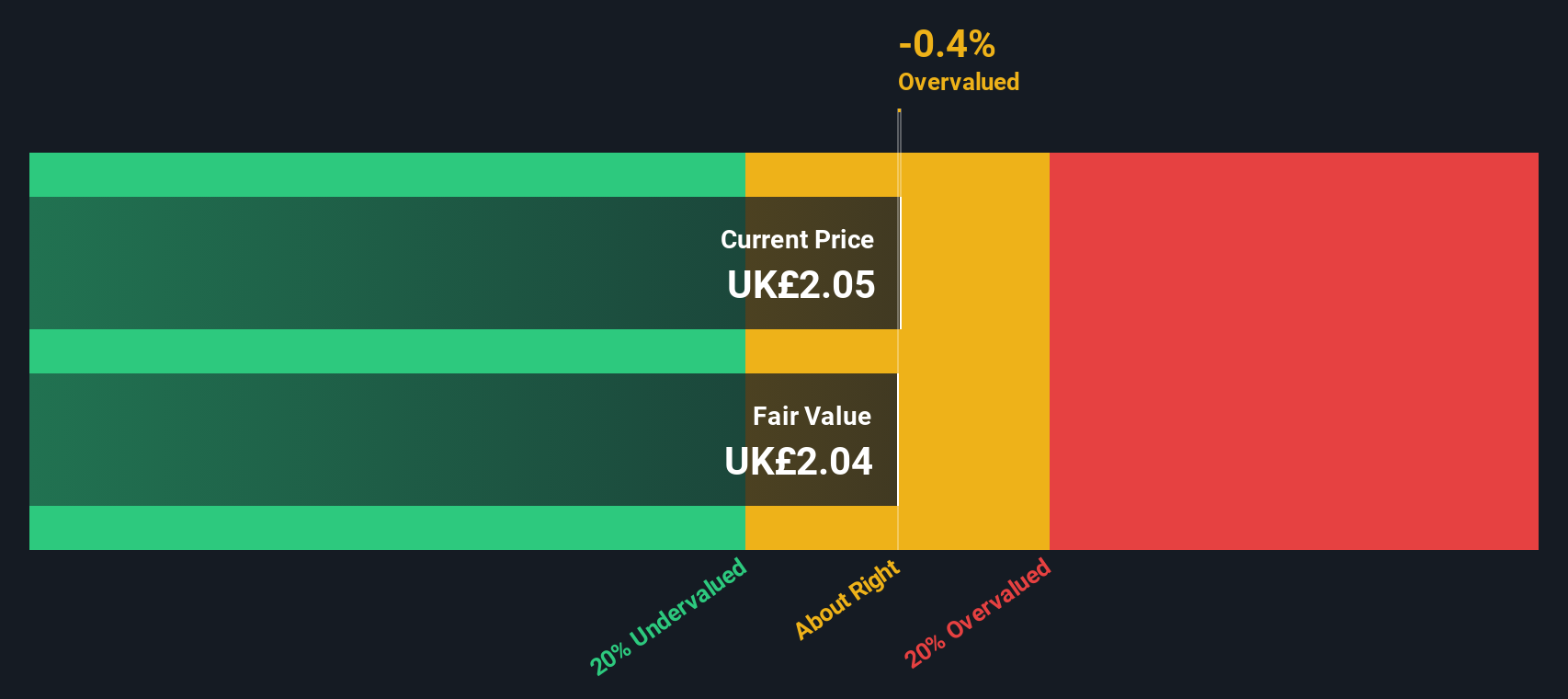

Kier Group (LSE:KIE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kier Group is a UK-based construction and infrastructure services company with operations in property, corporate, construction, and infrastructure services segments, holding a market cap of £0.26 billion.

Operations: The company generates revenue primarily from its Construction (£1.92 billion) and Infrastructure Services (£2.08 billion) segments. Over recent periods, the gross profit margin has shown variability, peaking at 10.12% in June 2018 before declining to 8.03% by December 2024. Operating expenses have consistently been a significant component of costs, with general and administrative expenses making up a substantial portion of these operating costs across the periods reviewed.

PE: 10.5x

Kier Group, operating in the construction sector, is experiencing insider confidence with share purchases indicating potential growth. The company reported a sales increase to £1.97 billion for the half year ending December 2024, alongside a net income rise to £20.4 million. A 20% interim dividend hike reflects financial health despite higher risk funding from external borrowing. Recently announced share repurchases aim to return capital to shareholders, enhancing its attractiveness in this investment category.

- Click to explore a detailed breakdown of our findings in Kier Group's valuation report.

Examine Kier Group's past performance report to understand how it has performed in the past.

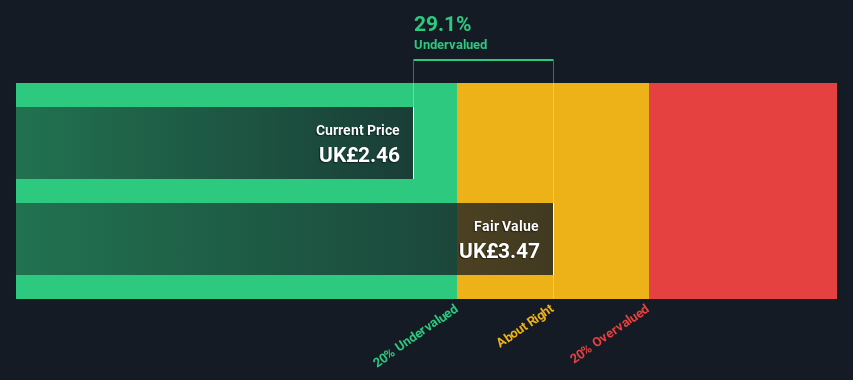

Marshalls (LSE:MSLH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Marshalls is a UK-based company specializing in the manufacturing and supply of products for the landscaping, building, and roofing sectors, with a market capitalization of approximately £1.20 billion.

Operations: The company generates revenue primarily from its Roofing, Building, and Landscaping products. Over the years, it has experienced fluctuations in net income margin, with a notable decrease during 2020 but subsequent recovery observed by 2024. Gross profit margin reached a peak of 64.18% in late 2024 and early 2025. Operating expenses have consistently been a significant portion of costs, with general and administrative expenses being a major component within this category.

PE: 19.5x

Marshalls, a company with exclusively external borrowing, reported a sales dip to £619.2 million for 2024 from £671.2 million the previous year but saw net income rise to £31 million from £18.6 million. Earnings per share increased significantly, reflecting potential growth despite funding risks. Recent insider confidence was evident as insiders made notable stock purchases over the past six months, suggesting optimism about future prospects amidst their expansion into Vancouver's retail market on March 18, 2025.

- Take a closer look at Marshalls' potential here in our valuation report.

Explore historical data to track Marshalls' performance over time in our Past section.

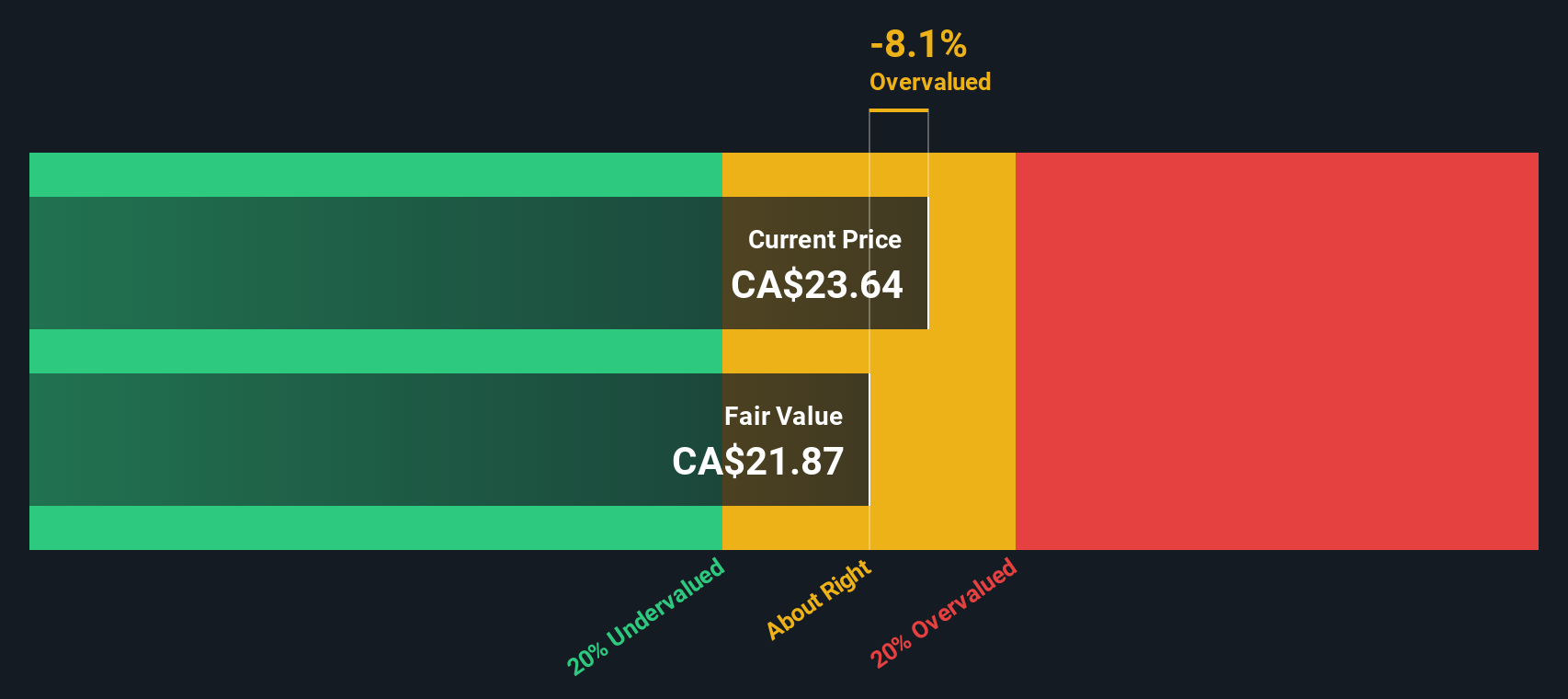

Wajax (TSX:WJX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Wajax is a Canadian company specializing in the distribution and service of industrial equipment and machinery, with a market capitalization of approximately CA$0.48 billion.

Operations: The company generates revenue primarily from wholesale operations in machinery and industrial equipment, with a recent quarterly revenue of CA$2.10 billion. The cost of goods sold (COGS) significantly impacts the gross profit, which stood at CA$413.78 million for the latest period. Operating expenses are a notable expense category, amounting to CA$311.52 million in the same period, while non-operating expenses were reported at CA$59.47 million. The net income margin was 2.04%, indicating that after all costs and expenses, this percentage of revenue translates into profit for shareholders.

PE: 9.0x

Wajax, a smaller company in the industrial sector, has seen its net profit margin decrease to 2% from last year's 3.8%, indicating some financial pressure. Despite sales dropping slightly to C$2.1 billion for the year ending December 2024, insider confidence is evident with recent share purchases by insiders. The company's earnings per share have halved compared to last year, yet it continues paying a quarterly dividend of C$0.35 per share. Future growth may depend on improving its financial position and managing external borrowings effectively.

- Click here and access our complete valuation analysis report to understand the dynamics of Wajax.

Assess Wajax's past performance with our detailed historical performance reports.

Key Takeaways

- Explore the 145 names from our Undervalued Global Small Caps With Insider Buying screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kier Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:KIE

Kier Group

Primarily engages in the construction business in the United Kingdom and internationally.

Proven track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor