Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Velocity Composites plc (LON:VEL) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Velocity Composites

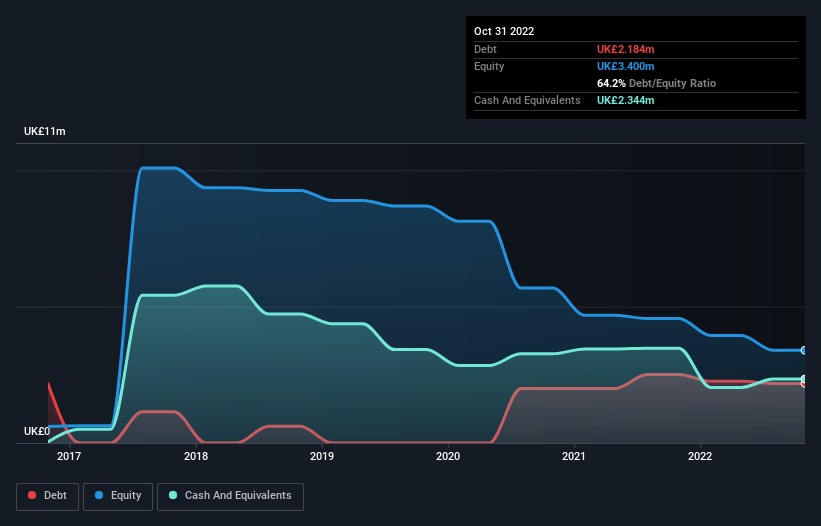

How Much Debt Does Velocity Composites Carry?

You can click the graphic below for the historical numbers, but it shows that Velocity Composites had UK£2.18m of debt in October 2022, down from UK£2.51m, one year before. But it also has UK£2.34m in cash to offset that, meaning it has UK£160.0k net cash.

A Look At Velocity Composites' Liabilities

The latest balance sheet data shows that Velocity Composites had liabilities of UK£3.12m due within a year, and liabilities of UK£3.30m falling due after that. Offsetting these obligations, it had cash of UK£2.34m as well as receivables valued at UK£2.24m due within 12 months. So its liabilities total UK£1.83m more than the combination of its cash and short-term receivables.

Of course, Velocity Composites has a market capitalization of UK£14.2m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Velocity Composites also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Velocity Composites's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Velocity Composites wasn't profitable at an EBIT level, but managed to grow its revenue by 22%, to UK£12m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Velocity Composites?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Velocity Composites had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through UK£118k of cash and made a loss of UK£1.3m. While this does make the company a bit risky, it's important to remember it has net cash of UK£160.0k. That means it could keep spending at its current rate for more than two years. Velocity Composites's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 2 warning signs we've spotted with Velocity Composites .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:VEL

Velocity Composites

Provides engineered composite material kits and related products to the aerospace industry in the United Kingdom, Europe, the United States, and internationally.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor