Advertisement

- United Kingdom

- /

- Trade Distributors

- /

- AIM:BMT

We Think Braime Group (LON:BMT) Is Taking Some Risk With Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Braime Group PLC (LON:BMT) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Braime Group

What Is Braime Group's Net Debt?

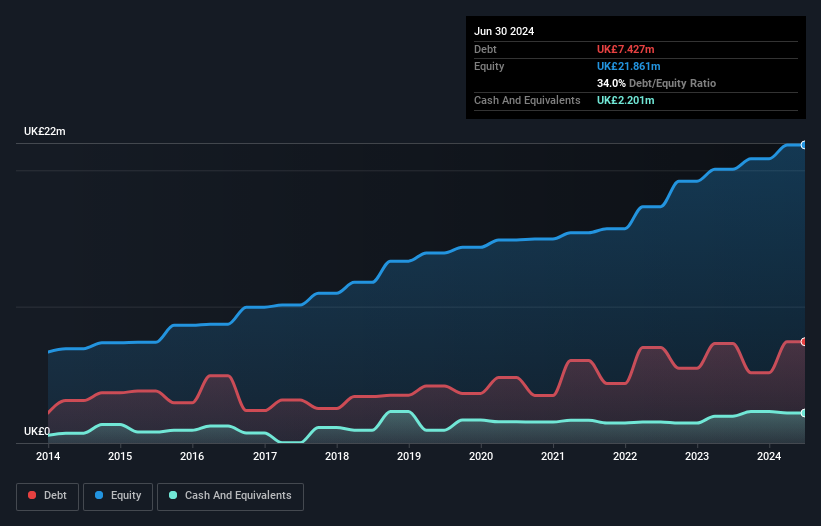

As you can see below, Braime Group had UK£7.43m of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. However, it also had UK£2.20m in cash, and so its net debt is UK£5.23m.

A Look At Braime Group's Liabilities

According to the last reported balance sheet, Braime Group had liabilities of UK£10.7m due within 12 months, and liabilities of UK£2.98m due beyond 12 months. Offsetting this, it had UK£2.20m in cash and UK£9.48m in receivables that were due within 12 months. So it has liabilities totalling UK£2.02m more than its cash and near-term receivables, combined.

Of course, Braime Group has a market capitalization of UK£18.5m, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Looking at its net debt to EBITDA of 1.2 and interest cover of 6.8 times, it seems to us that Braime Group is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. In fact Braime Group's saving grace is its low debt levels, because its EBIT has tanked 28% in the last twelve months. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Braime Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Braime Group created free cash flow amounting to 14% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Braime Group's EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example, its net debt to EBITDA is relatively strong. Taking the abovementioned factors together we do think Braime Group's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Braime Group (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Braime Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:BMT

Braime Group

Engages in the distribution of bulk material handling components and monitoring equipment in the United Kingdom, Rest of Europe, the Middle East, the United States, Africa, Australia, and Asia.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor