- Switzerland

- /

- Electrical

- /

- SWX:ACLN

Three Stocks Estimated To Be Priced Below Intrinsic Value In December 2024

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by interest rate cuts from the ECB and SNB, alongside expectations of a Fed rate cut, investors are keenly observing the mixed performance across major indices. While technology stocks have pushed the Nasdaq Composite to new heights, other indexes have struggled amid rising inflation and cooling labor markets. In such an environment, identifying stocks that may be undervalued relative to their intrinsic value can offer potential opportunities for investors seeking to balance risk with reward.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Clear Secure (NYSE:YOU) | US$26.67 | US$53.13 | 49.8% |

| Shandong Bailong Chuangyuan Bio-Tech (SHSE:605016) | CN¥16.64 | CN¥33.16 | 49.8% |

| Shenzhen King Explorer Science and Technology (SZSE:002917) | CN¥9.59 | CN¥19.09 | 49.8% |

| Musashi Seimitsu Industry (TSE:7220) | ¥4020.00 | ¥8038.95 | 50% |

| Xiamen Bank (SHSE:601187) | CN¥5.68 | CN¥11.35 | 50% |

| Gaming Realms (AIM:GMR) | £0.36 | £0.72 | 49.8% |

| MicroPort NeuroScientific (SEHK:2172) | HK$9.18 | HK$18.27 | 49.8% |

| BYD Electronic (International) (SEHK:285) | HK$39.85 | HK$79.36 | 49.8% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP291.30 | CLP579.37 | 49.7% |

| Constellium (NYSE:CSTM) | US$10.91 | US$21.69 | 49.7% |

Let's take a closer look at a couple of our picks from the screened companies.

VusionGroup (ENXTPA:VU)

Overview: VusionGroup S.A. offers digitalization solutions for commerce across Europe, Asia, and North America with a market capitalization of €2.15 billion.

Operations: The company generates revenue of €830.16 million from installing and maintaining electronic shelf labels across its operational regions.

Estimated Discount To Fair Value: 29.2%

VusionGroup is trading at €134, which is 29.2% below its estimated fair value of €189.19, indicating it may be undervalued based on cash flows. Analysts agree the stock price could rise by 44.4%. The company's revenue growth forecast of 23.4% per year surpasses the French market average and earnings are expected to grow significantly at 81.77% annually, with profitability anticipated within three years and a high return on equity projected at 27.5%.

- Our expertly prepared growth report on VusionGroup implies its future financial outlook may be stronger than recent results.

- Get an in-depth perspective on VusionGroup's balance sheet by reading our health report here.

Norconsult (OB:NORCO)

Overview: Norconsult ASA is a consultancy firm specializing in community planning, engineering design, and architecture both in the Nordics and internationally, with a market cap of NOK12.37 billion.

Operations: The company generates revenue from various segments including Sweden (NOK1.75 billion), Denmark (NOK858 million), Norway Regions (NOK2.78 billion), Renewable Energy (NOK909 million), Norway Head Office (NOK2.99 billion), and Digital and Techno-Garden (NOK1.20 billion).

Estimated Discount To Fair Value: 34.3%

Norconsult is trading at NOK 42.9, significantly below its estimated fair value of NOK 65.27, suggesting it is undervalued based on cash flow analysis. Despite a decline in profit margins to 3.6% from last year's 5.4%, earnings are forecasted to grow significantly at over 30% annually, outpacing the Norwegian market's growth rate of 9.4%. Recent framework agreements with the Norwegian Defence Estates Agency could bolster future revenue streams.

- Insights from our recent growth report point to a promising forecast for Norconsult's business outlook.

- Dive into the specifics of Norconsult here with our thorough financial health report.

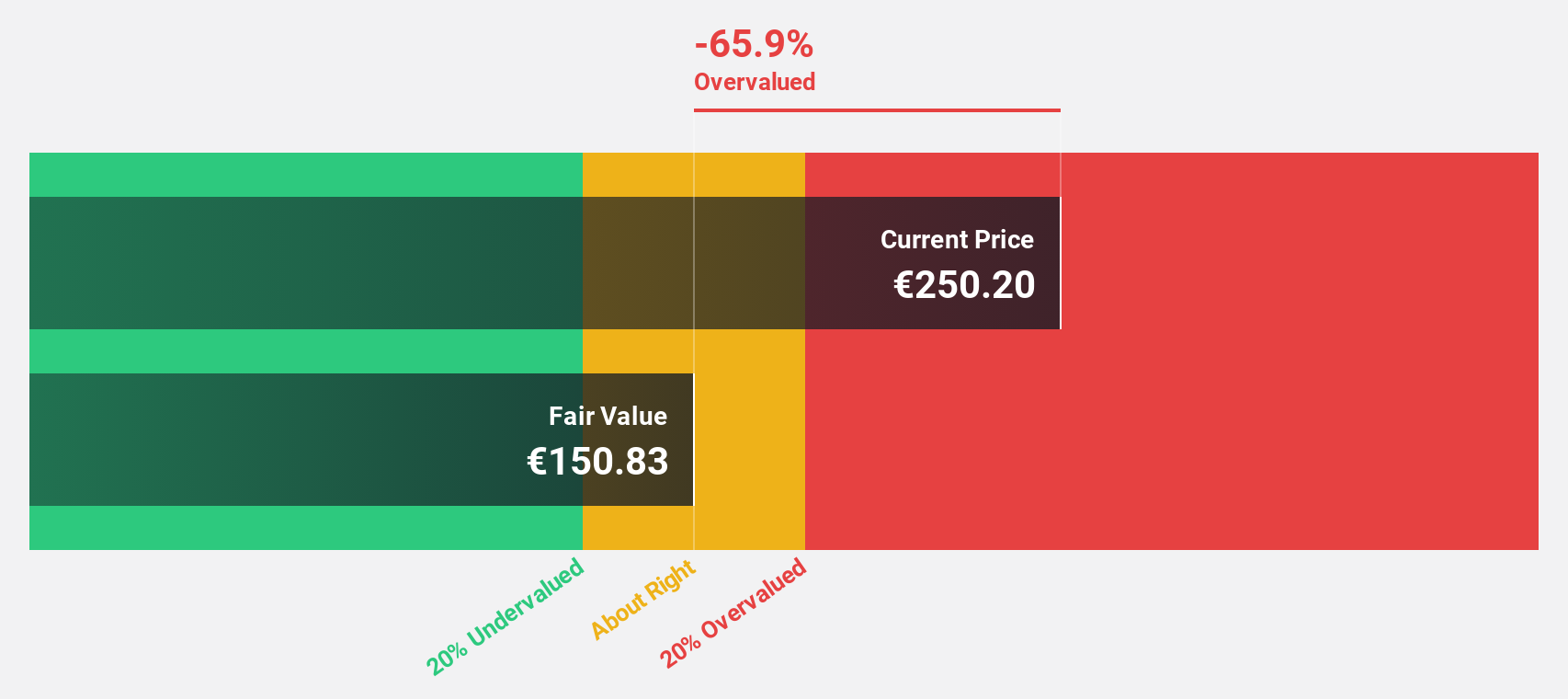

Accelleron Industries (SWX:ACLN)

Overview: Accelleron Industries AG develops, manufactures, sells, and services turbochargers and digital solutions globally with a market cap of CHF4.41 billion.

Operations: The company's revenue is segmented into High Speed, generating $245.87 million, and Medium & Low Speed, contributing $725.83 million.

Estimated Discount To Fair Value: 13.1%

Accelleron Industries, trading at CHF47.06, is undervalued with a fair value estimate of CHF54.13 based on cash flows. Although its earnings are forecasted to grow at 13.45% annually—outpacing the Swiss market's 11.6%—revenue growth is moderate at 5%. The company has a high debt level but boasts an impressive future return on equity of over 50%. Recent presentations highlight its focus on propulsion and future fuels innovation.

- Upon reviewing our latest growth report, Accelleron Industries' projected financial performance appears quite optimistic.

- Navigate through the intricacies of Accelleron Industries with our comprehensive financial health report here.

Seize The Opportunity

- Navigate through the entire inventory of 874 Undervalued Stocks Based On Cash Flows here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:ACLN

Accelleron Industries

Designs, manufactures, sells, and services turbochargers, fuel injection equipment, and digital solutions for heavy-duty applications worldwide.

Solid track record with reasonable growth potential.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion