Stock Analysis

- France

- /

- Aerospace & Defense

- /

- ENXTPA:HO

Exploring Undervalued Opportunities On Euronext Paris With Discounts Ranging From 22% To 41%

Reviewed by Simply Wall St

As France approaches a snap election, the French market has shown signs of volatility with the CAC 40 Index experiencing notable declines. Amidst this political uncertainty and mixed economic signals across Europe, investors may find potential in undervalued stocks that could be poised for recovery or growth as conditions stabilize. In such markets, discerning opportunities often involves looking for companies with solid fundamentals that are trading below their intrinsic values due to short-term pressures.

Top 10 Undervalued Stocks Based On Cash Flows In France

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Wavestone (ENXTPA:WAVE) | €55.90 | €93.37 | 40.1% |

| Lectra (ENXTPA:LSS) | €29.50 | €44.41 | 33.6% |

| Arcure (ENXTPA:ALCUR) | €6.06 | €7.71 | 21.4% |

| Vivendi (ENXTPA:VIV) | €9.896 | €16.00 | 38.1% |

| Figeac Aero Société Anonyme (ENXTPA:FGA) | €5.96 | €9.97 | 40.2% |

| Tikehau Capital (ENXTPA:TKO) | €21.65 | €32.42 | 33.2% |

| Esker (ENXTPA:ALESK) | €185.80 | €261.17 | 28.9% |

| Antin Infrastructure Partners SAS (ENXTPA:ANTIN) | €12.08 | €15.49 | 22% |

| Thales (ENXTPA:HO) | €155.10 | €263.09 | 41% |

| Groupe Airwell Société anonyme (ENXTPA:ALAIR) | €3.84 | €6.30 | 39% |

Let's take a closer look at a couple of our picks from the screened companies

Antin Infrastructure Partners SAS (ENXTPA:ANTIN)

Overview: Antin Infrastructure Partners SAS is a private equity firm focused on infrastructure investments, with a market capitalization of approximately €2.16 billion.

Operations: The firm generates revenue primarily through its asset management segment, totaling €282.87 million.

Estimated Discount To Fair Value: 22%

Antin Infrastructure Partners SAS, trading at €11.72, appears undervalued based on a DCF valuation of €15.29, marking a 23.4% discount to fair value. Despite recent profitability and a robust forecasted earnings growth of 22.4% per year, challenges persist with dividend coverage by earnings or cash flows. The company's strong projected revenue growth of 12.5% annually outpaces the French market's 5.7%, supported by high expected Return on Equity at 38.2%.

- Our growth report here indicates Antin Infrastructure Partners SAS may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Antin Infrastructure Partners SAS.

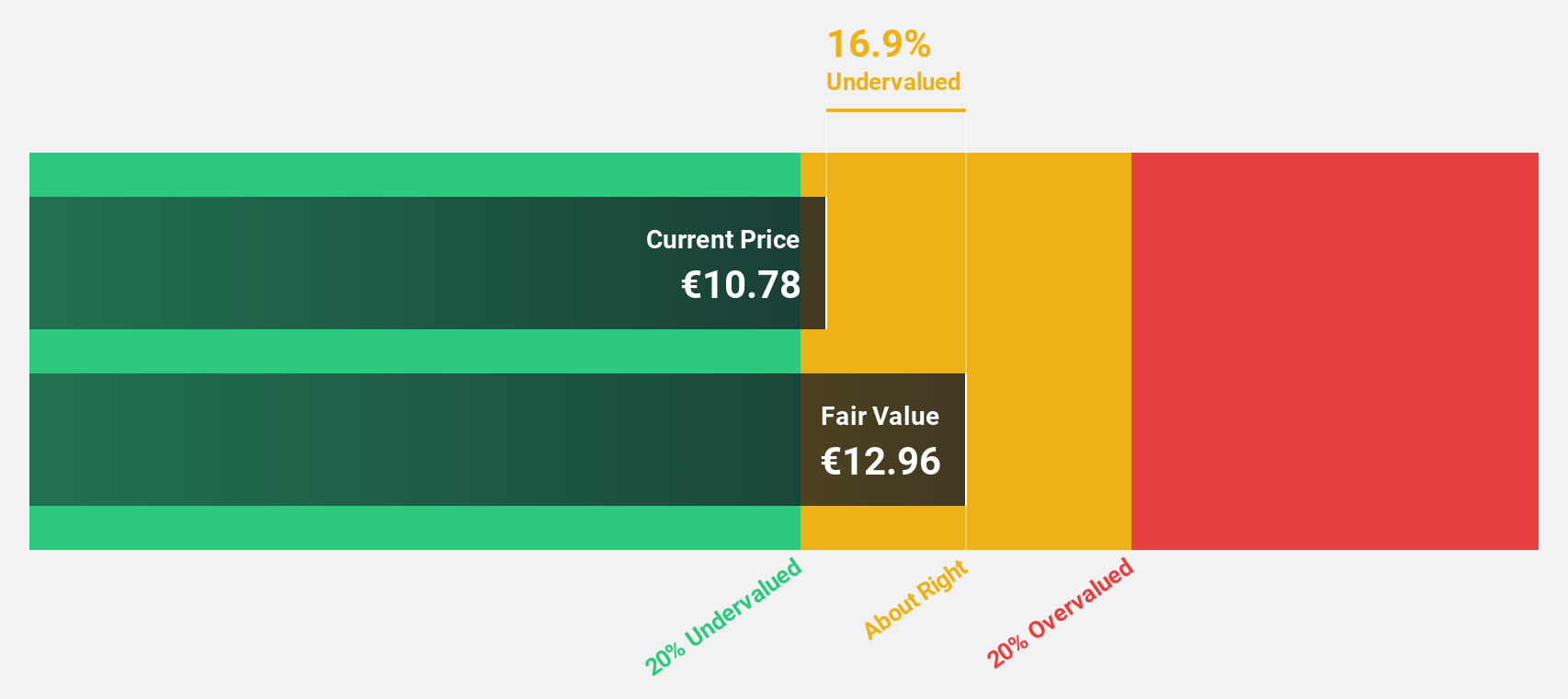

Thales (ENXTPA:HO)

Overview: Thales S.A. is a global company offering a range of solutions in defense, aerospace, digital identity and security, and transportation sectors, with a market capitalization of approximately €32.05 billion.

Operations: Thales generates revenue from several key segments: €10.18 billion in Defense & Security (excluding Digital I&S), €5.34 billion in Aerospace, and €3.42 billion in Digital Identity & Security.

Estimated Discount To Fair Value: 41%

Thales, valued at €151.5, is trading below its fair value of €263.69, indicating a significant undervaluation based on cash flows. Recent strategic alliances and product launches underscore its robust positioning in cybersecurity and aerospace, potentially boosting future revenues which are expected to grow at 6.3% annually—faster than the French market's 5.7%. However, concerns about its high debt levels and unstable dividend track record may temper investor enthusiasm despite a promising Return on Equity forecast of 23.3% in three years.

- The growth report we've compiled suggests that Thales' future prospects could be on the up.

- Dive into the specifics of Thales here with our thorough financial health report.

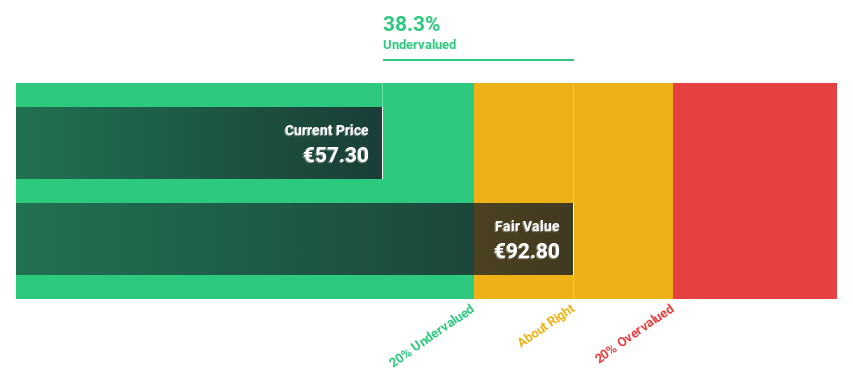

Wavestone (ENXTPA:WAVE)

Overview: Wavestone SA is a technology consulting firm operating mainly in France and globally, with a market capitalization of approximately €1.37 billion.

Operations: The firm generates its revenue through technology consulting services both domestically and globally.

Estimated Discount To Fair Value: 40.1%

Wavestone, priced at €54.6, trades significantly below its estimated fair value of €93.67, reflecting a deep undervaluation based on discounted cash flows. The company's earnings are poised to grow by 22% annually, outpacing the French market's 10.9%. Despite this robust growth projection and a recent increase in net income to €58.2 million from last year’s €50.07 million, concerns linger due to a low forecasted Return on Equity of 13.3% and recent shareholder dilution.

- Upon reviewing our latest growth report, Wavestone's projected financial performance appears quite optimistic.

- Get an in-depth perspective on Wavestone's balance sheet by reading our health report here.

Make It Happen

- Navigate through the entire inventory of 13 Undervalued Euronext Paris Stocks Based On Cash Flows here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Thales is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:HO

Thales

Provides various solutions in the defence and security, aerospace and space, digital identity and security, and transport markets worldwide.

Reasonable growth potential average dividend payer.