Stock Analysis

Clinuvel Pharmaceuticals Leads Three High Growth Companies With Significant Insider Ownership

Reviewed by Simply Wall St

As global markets navigate through a period of relative calm with anticipation for upcoming earnings reports and key economic indicators, investors continue to assess the landscape for robust investment opportunities. In this environment, growth companies with high insider ownership can be particularly compelling, as substantial insider stakes often signal confidence in the company's future prospects from those who know it best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.3% | 36.4% |

| Gaming Innovation Group (OB:GIG) | 26.7% | 36.9% |

| Seojin SystemLtd (KOSDAQ:A178320) | 27.9% | 48.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.6% |

| Calliditas Therapeutics (OM:CALTX) | 11.6% | 52.9% |

| Vow (OB:VOW) | 31.8% | 97.6% |

| UTI (KOSDAQ:A179900) | 34.1% | 122.7% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 74.3% |

We're going to check out a few of the best picks from our screener tool.

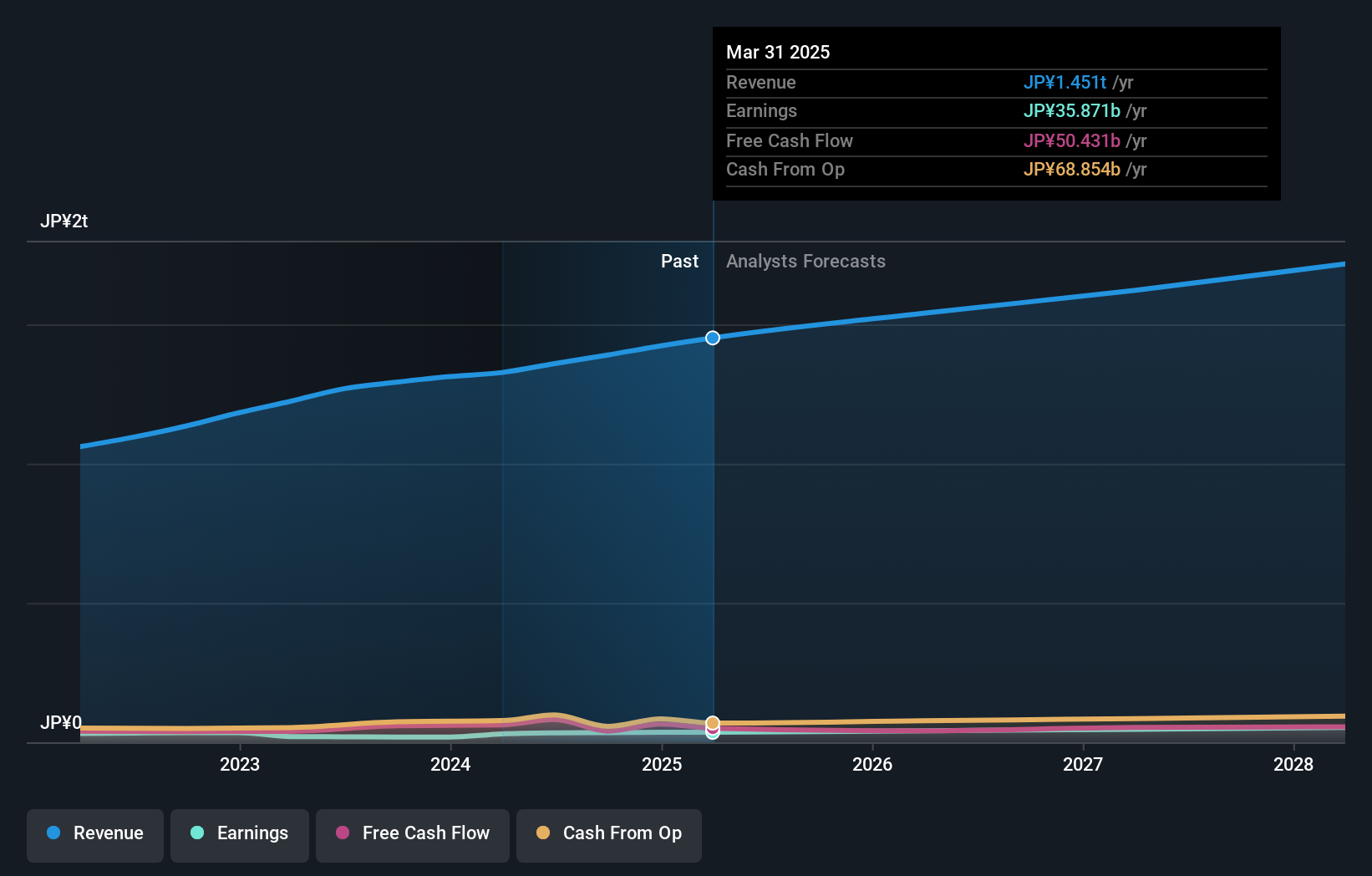

Clinuvel Pharmaceuticals (ASX:CUV)

Simply Wall St Growth Rating: ★★★★★★

Overview: Clinuvel Pharmaceuticals Limited is a biopharmaceutical company that specializes in developing and commercializing treatments for patients with genetic, metabolic, and life-threatening disorders across Australia, Europe, the U.S., and Switzerland, with a market capitalization of approximately A$0.76 billion.

Operations: The company generates revenue primarily from its biopharmaceutical sector, totaling A$81.76 million.

Insider Ownership: 13.6%

Clinuvel Pharmaceuticals, with high insider ownership, is poised for robust growth with expected annual profit and revenue increases outpacing the Australian market. Recent executive changes and innovative clinical trials in Parkinson’s Disease underscore its strategic direction. Despite these prospects, it's crucial to monitor the effectiveness of new health applications and management transitions closely to gauge future performance accurately.

- Navigate through the intricacies of Clinuvel Pharmaceuticals with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that Clinuvel Pharmaceuticals' share price might be on the expensive side.

Exclusive Networks (ENXTPA:EXN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Exclusive Networks SA is a global cybersecurity specialist for digital infrastructure with a market capitalization of approximately €1.93 billion.

Operations: The company generates revenue primarily from three geographical segments: APAC (€420 million), EMEA (€4.04 billion), and the Americas (€689 million).

Insider Ownership: 13.2%

Exclusive Networks SA, despite not leading in growth companies with high insider ownership, shows potential with earnings projected to increase by 28.4% annually, outpacing the French market's 10.9%. Revenue is expected to grow at 14.4% yearly, faster than the market average of 5.7%, though below the high-growth benchmark of 20%. Recent shifts include appointing KPMG as auditor and forecasting sales growth between 10-12% for FY2024, signaling strategic adjustments and steady fiscal expectations.

- Click here to discover the nuances of Exclusive Networks with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Exclusive Networks is priced higher than what may be justified by its financials.

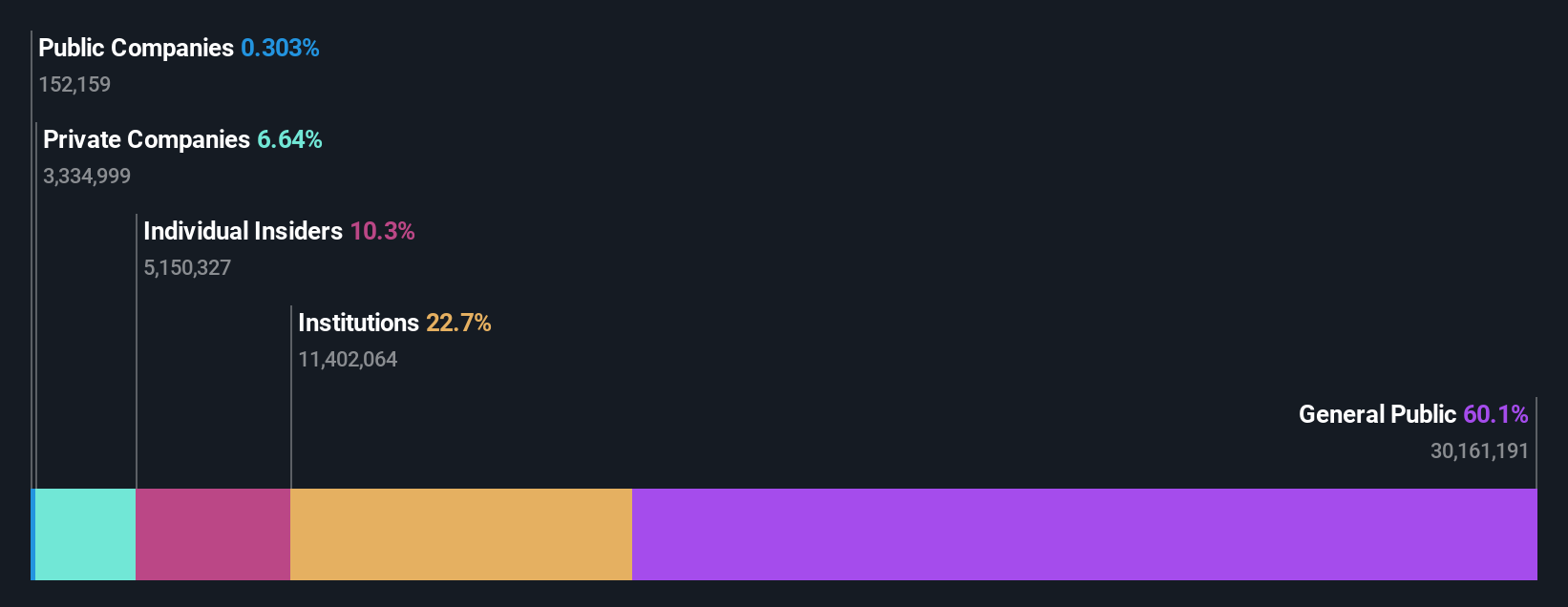

Persol HoldingsLtd (TSE:2181)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Persol Holdings Co., Ltd. operates globally, offering human resource services under the PERSOL brand, with a market capitalization of approximately ¥555.86 billion.

Operations: The company's revenue is primarily generated from staffing services (excluding BPO) at ¥575.80 billion, followed by its Asia Pacific operations at ¥412.77 billion, with additional contributions from career services and technology segments amounting to ¥128.28 billion and ¥102.38 billion respectively, alongside its BPO activities generating ¥110.80 billion.

Insider Ownership: 11.8%

Persol Holdings Ltd., while not a standout in growth companies with high insider ownership, displays promising aspects. The company's earnings are expected to rise by 12% annually, surpassing the Japanese market forecast of 8.9%. However, its revenue growth at 5.3% per year is modest compared to high-growth benchmarks but still exceeds the Japanese market's 4.2%. Recent strategic moves include a significant share buyback program valued at ¥20 billion, aiming to enhance shareholder returns by March 2025.

- Unlock comprehensive insights into our analysis of Persol HoldingsLtd stock in this growth report.

- Upon reviewing our latest valuation report, Persol HoldingsLtd's share price might be too pessimistic.

Key Takeaways

- Click here to access our complete index of 1450 Fast Growing Companies With High Insider Ownership.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Exclusive Networks is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:EXN

Exclusive Networks

Operates as a global cybersecurity specialist for digital infrastructure.

Flawless balance sheet with reasonable growth potential.