Advertisement

Global markets have shown mixed results recently, with major indices like the S&P 500 and Nasdaq Composite closing the year with significant gains despite some volatility. Amidst these broader market movements, investors often turn their attention to lesser-known opportunities that might offer growth potential at a lower cost. Penny stocks, though sometimes seen as a throwback to earlier trading days, continue to attract interest for their affordability and potential upside. In this article, we explore three penny stocks that stand out due to their strong financial foundations and promising prospects.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.53 | MYR2.64B | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.775 | A$142.2M | ★★★★☆☆ |

| Datasonic Group Berhad (KLSE:DSONIC) | MYR0.425 | MYR1.18B | ★★★★★★ |

| Hil Industries Berhad (KLSE:HIL) | MYR0.90 | MYR298.75M | ★★★★★★ |

| Bosideng International Holdings (SEHK:3998) | HK$3.64 | HK$40.08B | ★★★★★★ |

| LaserBond (ASX:LBL) | A$0.56 | A$65.64M | ★★★★★★ |

| Lever Style (SEHK:1346) | HK$0.86 | HK$545.92M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.968 | £152.69M | ★★★★★★ |

| Stelrad Group (LSE:SRAD) | £1.46 | £185.93M | ★★★★★☆ |

| Secure Trust Bank (LSE:STB) | £3.58 | £68.28M | ★★★★☆☆ |

Click here to see the full list of 5,820 stocks from our Penny Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

Verimatrix (ENXTPA:VMX)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Verimatrix SA offers security solutions to safeguard digital content, applications, and devices globally, with a market cap of €26.87 million.

Operations: The company's revenue is primarily derived from its Software Strategic Activity, which generated $61.83 million.

Market Cap: €26.87M

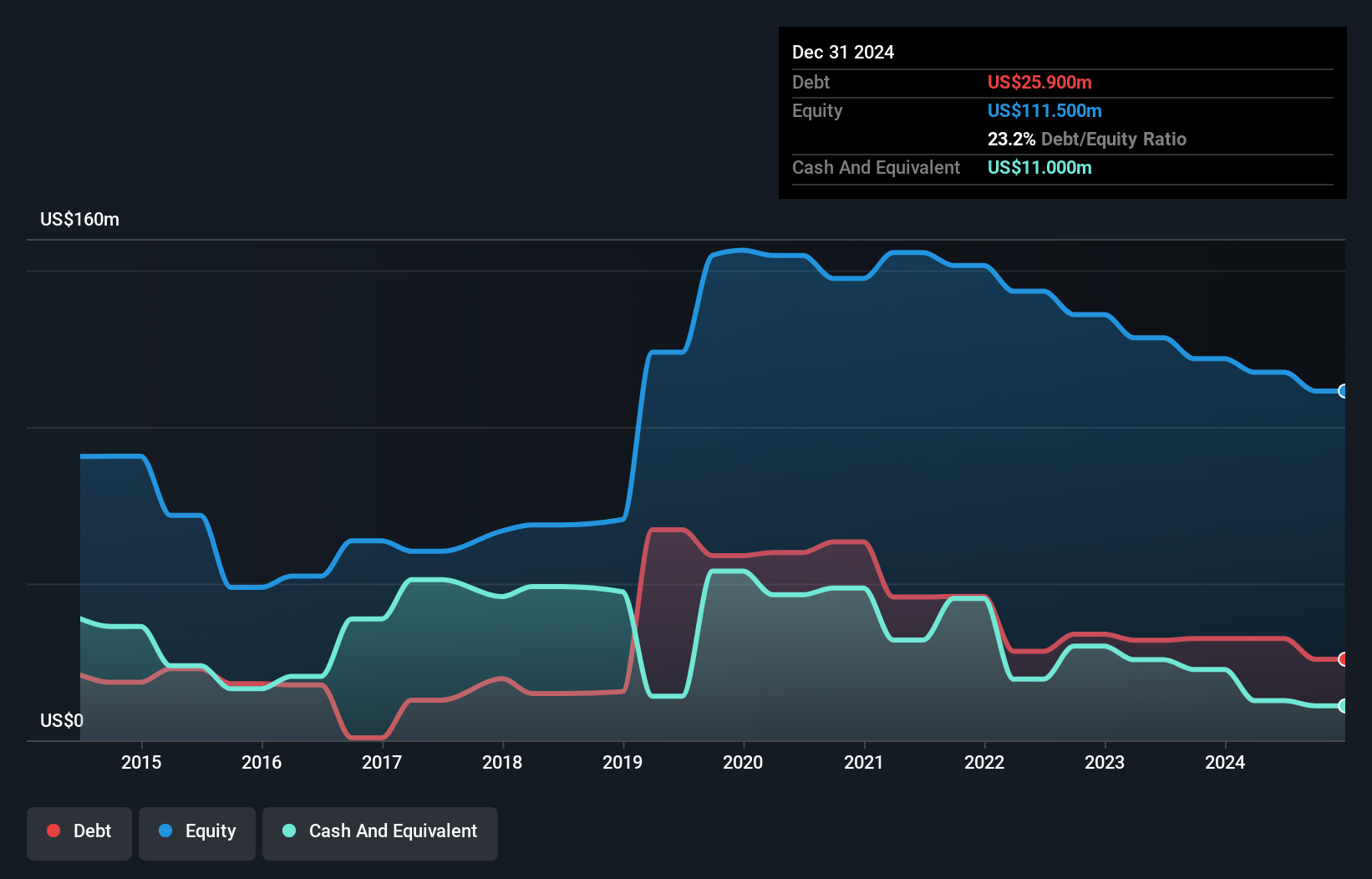

Verimatrix SA, with a market cap of €26.87 million, is trading at 69.3% below its estimated fair value, suggesting potential for investors seeking undervalued opportunities. Despite being unprofitable and not expected to reach profitability in the next three years, the company has managed to reduce its debt-to-equity ratio from 54.2% to 27.6% over five years and maintains a satisfactory net debt-to-equity ratio of 16.9%. Verimatrix's short-term assets ($52.9M) comfortably cover both short-term ($35.6M) and long-term liabilities ($32.9M), providing some financial stability amidst its challenges in achieving profitability.

- Click here to discover the nuances of Verimatrix with our detailed analytical financial health report.

- Review our growth performance report to gain insights into Verimatrix's future.

Be Friends Holding (SEHK:1450)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Be Friends Holding Limited is an investment holding company that offers all-media services in the People's Republic of China, with a market capitalization of HK$1.43 billion.

Operations: The company's revenue is primarily derived from New Media Services, contributing CN¥1.16 billion, and Television Broadcasting Business, which accounts for CN¥103.05 million.

Market Cap: HK$1.43B

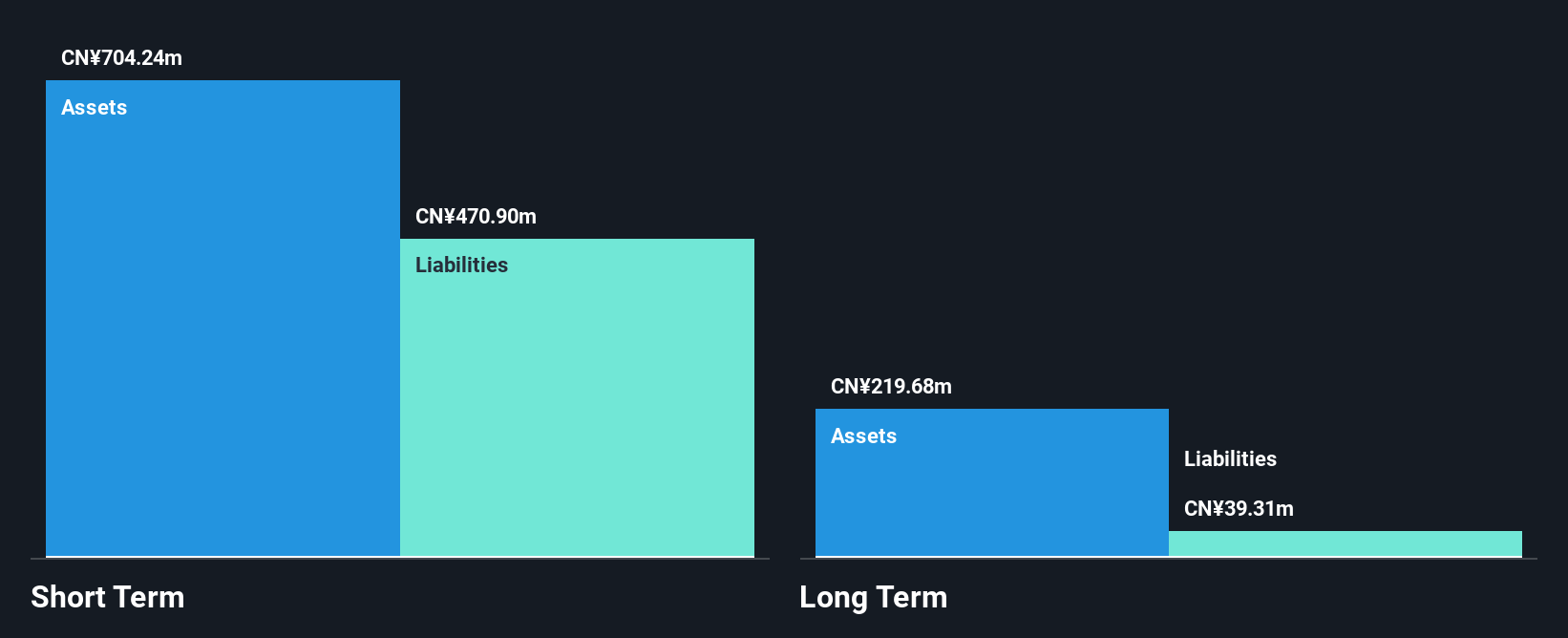

Be Friends Holding Limited, with a market capitalization of HK$1.43 billion, demonstrates financial stability through its substantial short-term assets (CN¥674.8M) exceeding both short-term (CN¥419.8M) and long-term liabilities (CN¥64.1M). The company has achieved significant earnings growth of 158.7% over the past year, surpassing the media industry average, and maintains high-quality earnings with a strong return on equity of 37.5%. Recent management changes include Mr. Li Liang's appointment as CEO and chairman of the investment committee, bringing extensive business management experience to guide future operations effectively.

- Get an in-depth perspective on Be Friends Holding's performance by reading our balance sheet health report here.

- Review our historical performance report to gain insights into Be Friends Holding's track record.

TK Group (Holdings) (SEHK:2283)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: TK Group (Holdings) Limited is an investment holding company involved in the manufacture, sale, subcontracting, fabrication, and modification of molds and plastic components with a market cap of HK$1.99 billion.

Operations: The company's revenue is primarily derived from two segments: Mold Fabrication, contributing HK$767.37 million, and Plastic Components Manufacturing, generating HK$1.47 billion.

Market Cap: HK$1.99B

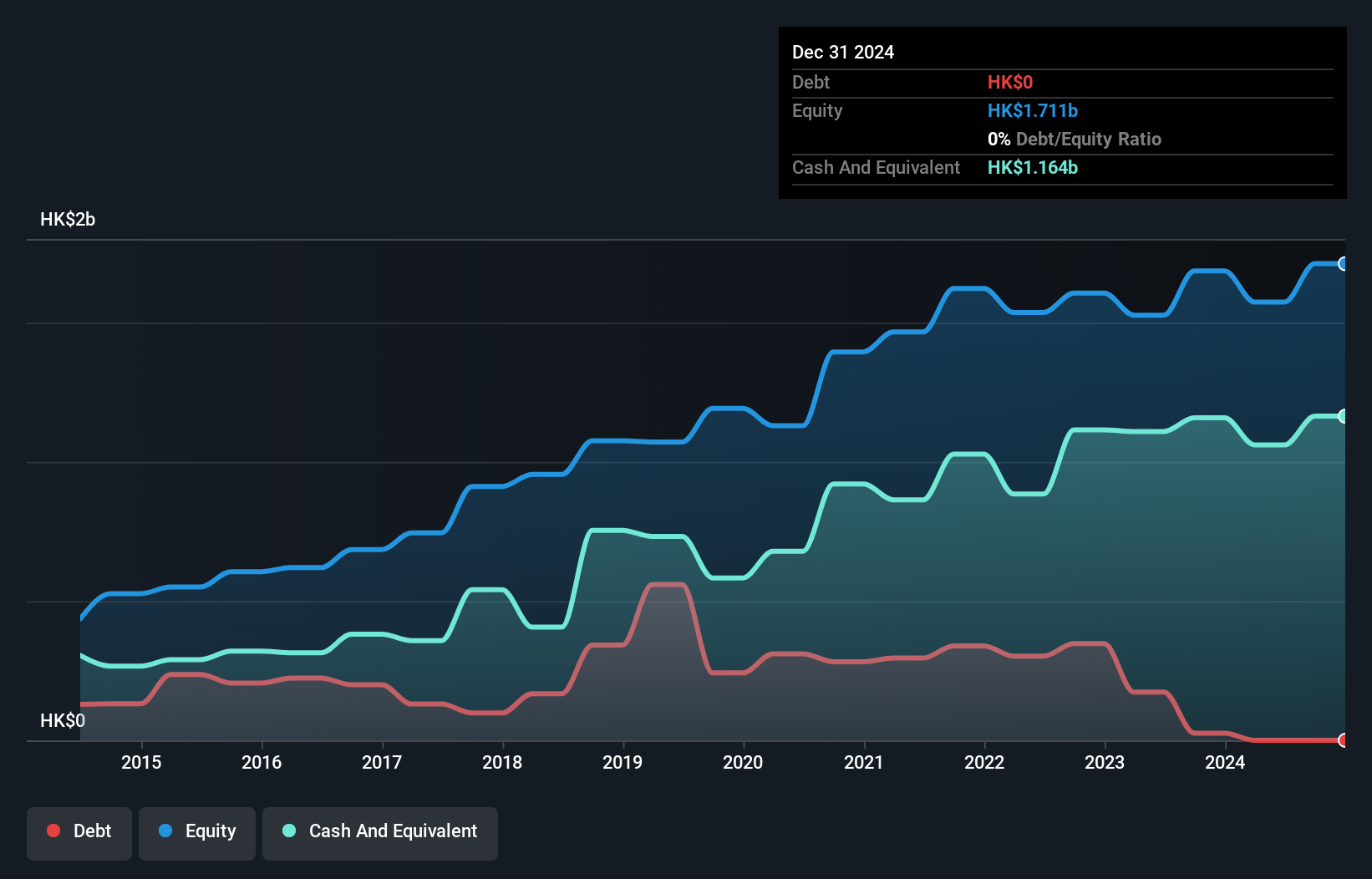

TK Group (Holdings) Limited, with a market cap of HK$1.99 billion, benefits from a strong financial position, having no debt and sufficient short-term assets of HK$2.0 billion to cover both its long-term and short-term liabilities. Despite stable weekly volatility at 7%, the company's earnings growth of 2.7% in the past year lags behind the broader machinery industry. While trading significantly below estimated fair value, TK Group's return on equity is low at 14.6%, and it has experienced a decline in profits over five years but forecasts suggest potential annual earnings growth of approximately 19%.

- Dive into the specifics of TK Group (Holdings) here with our thorough balance sheet health report.

- Examine TK Group (Holdings)'s earnings growth report to understand how analysts expect it to perform.

Key Takeaways

- Click through to start exploring the rest of the 5,817 Penny Stocks now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Be Friends Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1450

Be Friends Holding

An investment holding company, provides all-media services in the People’s Republic of China.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor