Atos (ENXTPA:ATO) shares have caught the attention of investors lately, returning nearly 95% over the past 3 months. The stock’s recent surge has sparked renewed conversations about its current valuation and future prospects.

Atos’s recent rally stands out, but zooming out reveals the bigger picture: while the past three months brought a remarkable 94.67% share price return, the one-year total shareholder return is just 8.7%, and losses over three and five years remain significant. This sharp uptick suggests momentum has returned, which likely reflects renewed optimism around the company’s turnaround and risk profile.

This recent price surge raises a key question for investors: is Atos still trading at a discount, or has the market already factored in all the potential upside from its ongoing turnaround?

Advertisement

Most Popular Narrative: 34.5% Overvalued

Compared to Atos’s last close price of €52.98, the most widely followed narrative sets fair value at just €39.40. This highlights a sizable gap in expectations. With the market price sitting well above the narrative's estimate, investors face a stark divergence in sentiment over the company's outlook.

"Despite management's optimism, Atos continues to face significant headwinds from increasing automation and adoption of AI, which is structurally reducing demand for its traditional IT outsourcing and managed services. This ongoing shift is likely to pressure both revenues and margins as clients transition toward more modern, self-service, and cloud-native solutions."

Curious what assumptions drive this valuation? The narrative’s conclusion rests on a clash between expectations for major margin shifts and forecasts of long-term revenue pressures. Want to see which pivotal financial projections play the biggest role in the gap between price and fair value? Find out which factors are moving the target in the full narrative.

However, stabilizing revenues and renewed customer confidence could improve Atos’s outlook. This may potentially strengthen its future earnings and support a more resilient turnaround.

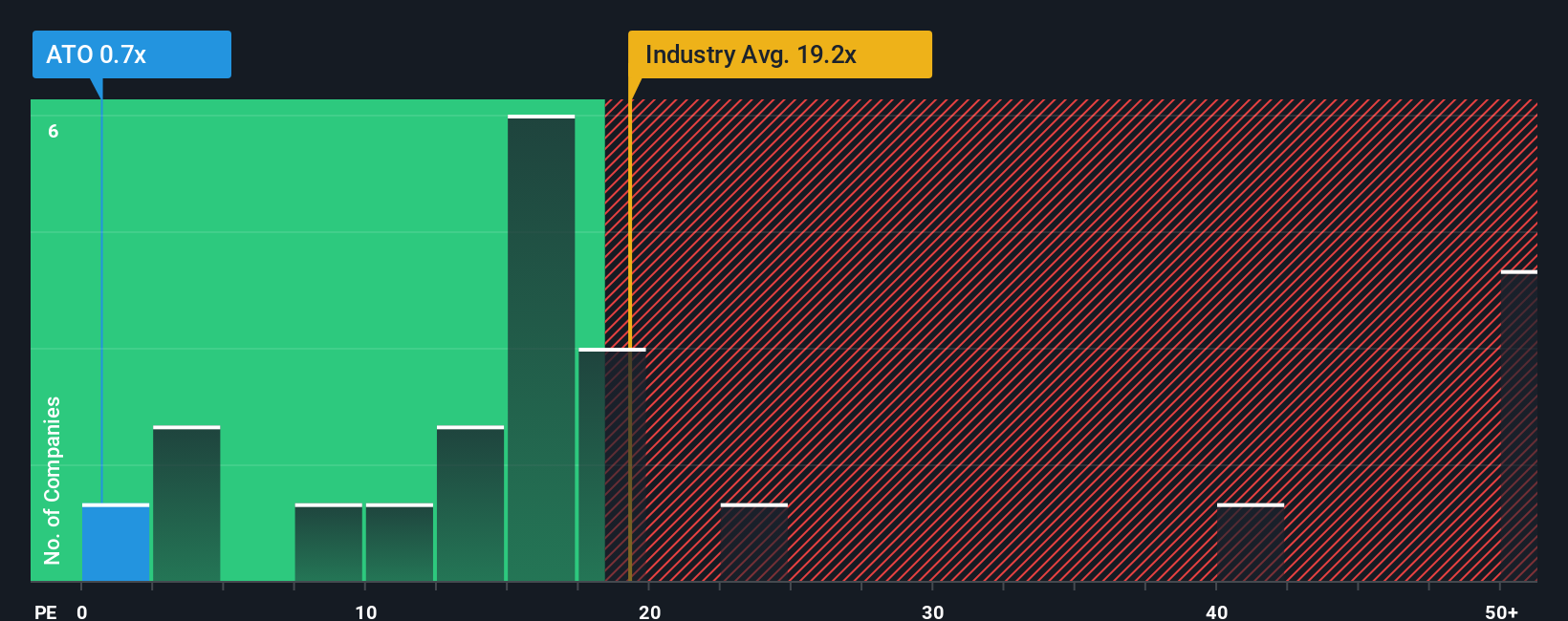

While the fair value estimate highlights downside risk, a closer look at Atos’s price-to-earnings ratio tells a very different story. Atos trades at just 0.7x earnings compared to 19.4x for the industry, 17x for peers, and a fair ratio of 4.8x. Such a large gap could mean the market is heavily discounting turnaround risks, but it also raises the question: are investors overlooking genuine value or rightly cautious about future challenges?

If the story so far doesn’t match your outlook, there’s always the option to check the numbers for yourself and shape your own view in just a few minutes. Do it your way

If you want to get ahead of the crowd, now’s the time to check out investment opportunities that most investors overlook. Don’t let the best ideas pass you by.

Unlock steady income by targeting companies with consistent payment history through these 21 dividend stocks with yields > 3%. This approach can help you build a more reliable portfolio.

Fuel your portfolio’s future growth by tapping into innovation-driven companies at the forefront of health and technology using these 34 healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks