Advertisement

- France

- /

- Semiconductors

- /

- ENXTPA:STMPA

STMicroelectronics FY 2025 Margin Compression Challenges Bullish Earnings Growth Narrative

Simply Wall St

Reviewed by Simply Wall St

How STMicroelectronics (ENXTPA:STMPA) Just Shaped Its FY 2025 Story

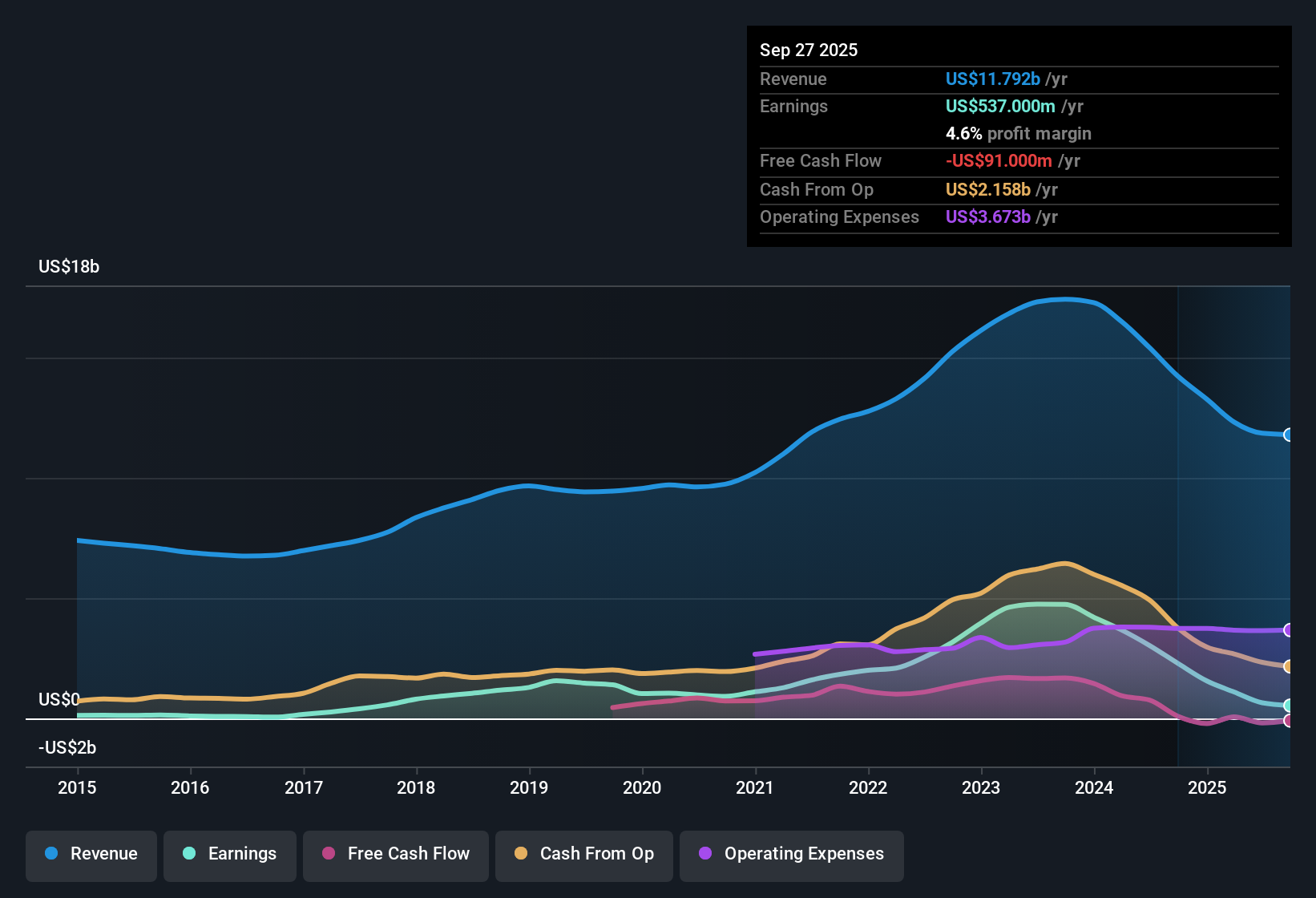

STMicroelectronics (ENXTPA:STMPA) closed FY 2025 with fourth quarter revenue of US$3.3b and a basic EPS loss of US$0.03, setting a mixed headline for investors digesting the latest print. Over the past six quarters, the company has seen quarterly revenue range from US$2.5b to US$3.3b, while basic EPS has swung between a profit of about US$0.39 and a loss of roughly US$0.11. This underscores how sensitive earnings have been to changes in profitability. With trailing 12 month net margins running at 1.4% after a sizeable one off loss, this set of results keeps the spotlight firmly on how durable the company’s margins really are.

See our full analysis for STMicroelectronics.With the latest numbers on the table, the next step is to see how this earnings profile lines up with the widely followed growth and risk narratives around STMicroelectronics and where those stories may need updating.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Hit By 1.4% Net Profit Level

- Over the last 12 months, STMicroelectronics generated about US$11.8b of revenue and US$166 million of net income, which works out to a 1.4% net profit margin compared with 11.7% in the prior year period mentioned in the risk summary.

- Bears point to the margin compression as a key concern, and the numbers give them material support:

- Net income for FY 2025 swung between a profit of US$237 million in Q3 and a loss of US$97 million in Q2, which sits uncomfortably next to the earlier trailing 12 month net income of US$1.6b reported for 2024 Q4.

- The risk summary also flags that earnings over the past five years declined about 6.4% per year, so the current 1.4% margin and recent losses in two of the last four quarters strengthen the bearish argument about earnings quality and consistency.

US$376m One Off Loss Distorts Profit Picture

- The analysis highlights a one off loss of US$376 million in the last 12 months, which had a large impact on reported profitability relative to the US$166 million of trailing net income.

- What is interesting for a more bullish angle is how this single item shapes the story:

- Without separating that US$376 million charge, the trailing figures fold it into the 1.4% margin, making the recent profitability look much weaker alongside the US$11.8b revenue base.

- Supporters arguing a bullish case could say that a one off of this size relative to trailing net income is masking the underlying run rate, but the mixed quarterly pattern, including losses in Q2 and Q4 2025, means the data does not give a clean read in their favor.

Revenue Stability Versus EPS Swings

- Quarterly revenue over FY 2025 stayed in a fairly tight band between US$2.5b and US$3.3b, while basic EPS moved from a profit of US$0.27 in Q3 2025 to a loss of US$0.11 in Q2 2025 and a small loss of US$0.03 in Q4 2025.

- Putting this alongside the AI generated growth oriented narrative creates a clear tension:

- The analysis references forecasts for earnings growth of about 37.2% a year and revenue growth of roughly 8.6% a year, yet the trailing 12 month basic EPS slipped from US$2.54 at 2024 Q3 to US$0.19 at 2025 Q4.

- That contrast between steady revenue in the US$11.8b range and much lower trailing EPS means any bullish view built around strong growth expectations has to square those forecasts with the recent pattern of earnings volatility and compressed profitability.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on STMicroelectronics's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

STMicroelectronics is facing thin 1.4% net margins, a sizeable US$376 million one off loss and uneven EPS, which all raise questions about earnings reliability.

If that kind of choppy profit profile makes you cautious, check out stable growth stocks screener (2166 results) to focus on companies with steadier revenue and earnings patterns that can help balance your ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:STMPA

STMicroelectronics

Designs, develops, manufactures, and sells semiconductor products in Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k7.1% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.122.6% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

BL

BlackGoat on Palantir Technologies ·

Palantir: Redefining Enterprise Software for the AI Era

Fair Value:US$107.0237.0% overvalued

193 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Microsoft ·

Microsoft - A Fundamental and Historical Valuation

Fair Value:US$437.171.6% undervalued

16 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Merck ·

The Oncology Anchor: Why Merck’s 46% Discount Defies the Keytruda Cliff

Fair Value:US$201.5645.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

70 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1044 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1342 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

HO

Holger on IREN ·

<b>Reported:</b> Revenue growth: 2024 → 2025 sharp increase of approx. 165%. Assuming moderate annual growth of 40%, a fair value in three years would be approx. $170. Given the customer base and the story, this should be possible. I find the most valuable “property” particularly interesting, as it solves the electricity problem.

1

|0

JA

jayhcee on Motorcar Parts of America ·

MPAA often has inventory and core-related timing issues. While this quarter’s problems may ease, similar issues have recurred historically and can persist for several quarters. It's not a one-off, it's a structural part of their business. Core returns are simply estimates: How many customers will actually return the original part; how quickly they'll do so; how many are useable; what they're worth, etc. MPAA predicts X sales in a quarter and Y core returns and its reserves, inventory values, etc. are based on that. If they expect a 90% core return rate and only 80% come back it doesn't change cash but they have to write down inventory and increase cost of goods sold which impacts EPS. They've also cited inventory buildup at key customers multiple times in the past. The assumption the latest backlog will all shift into future quarters this year with no impact on pricing, etc. seems more like wishful thinking. Retailer X was slated to buy $10m in parts this quarter but finds they have a lot more inventory on hand than they anticipated so they pushed the order. Realistically there are likely to be SKU cuts, reduction in safety stock on others, etc. Assuming that all $10m will come in this year plus the regular replenishment seems pretty unrealistic. MPAA also has a shaky track record when it comes to new lines and the supposed impact on business. If you look at the EV testing solutions hype back around 2020 that was supposed to diversify them beyond traditional reman and be a higher margin business that would grow with EV adoption. But it has never turned into a material contributor. The debt reduction and stock buy backs are meaningful but IMHO this narrative takes a very optimistic view of things.

0

|0