Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that ERYTECH Pharma S.A. (EPA:ERYP) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for ERYTECH Pharma

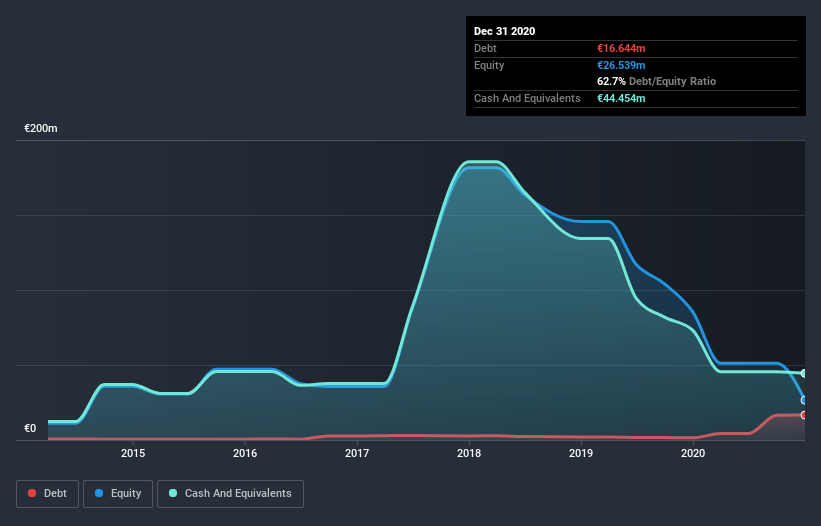

What Is ERYTECH Pharma's Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2020 ERYTECH Pharma had €16.6m of debt, an increase on €1.42m, over one year. But it also has €44.5m in cash to offset that, meaning it has €27.8m net cash.

How Healthy Is ERYTECH Pharma's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that ERYTECH Pharma had liabilities of €29.3m due within 12 months and liabilities of €24.5m due beyond that. On the other hand, it had cash of €44.5m and €4.33m worth of receivables due within a year. So its liabilities total €5.08m more than the combination of its cash and short-term receivables.

Of course, ERYTECH Pharma has a market capitalization of €129.6m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, ERYTECH Pharma also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine ERYTECH Pharma's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Since ERYTECH Pharma doesn't have significant operating revenue, shareholders may be hoping it comes up with a great new product, before it runs out of money.

So How Risky Is ERYTECH Pharma?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year ERYTECH Pharma had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through €53m of cash and made a loss of €73m. But at least it has €27.8m on the balance sheet to spend on growth, near-term. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example ERYTECH Pharma has 5 warning signs (and 1 which is a bit unpleasant) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade ERYTECH Pharma, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:PHXM

PHAXIAM Therapeutics

A biopharmaceutical company, focuses on developing solutions to combat severe and resistant bacterial infections in France and the United States.

Moderate and fair value.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor