Why DBV Technologies S.A. (EPA:DBV) Could Be Your Next Investment

DBV Technologies S.A. (EPA:DBV) is a company with exceptional fundamental characteristics. Upon building up an investment case for a stock, we should look at various aspects. In the case of DBV, it is a company with strong financial health as well as a buoyant growth outlook. Below is a brief commentary on these key aspects. If you're interested in understanding beyond my broad commentary, read the full report on DBV Technologies here.

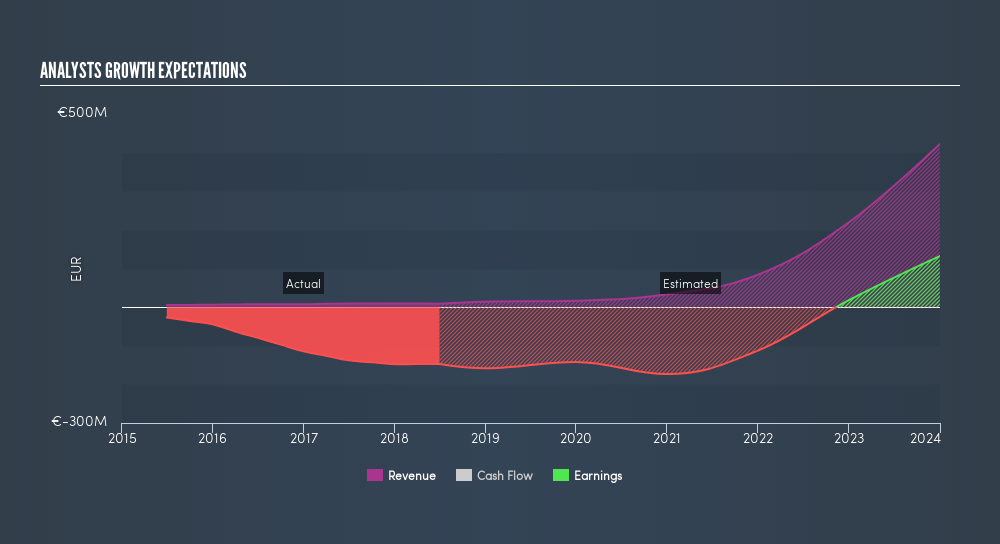

Flawless balance sheet with high growth potential

DBV is an attractive stock for growth-seeking investors, with an expected earnings growth of 33% in the upcoming year. The optimistic bottom-line growth is supported by a similarly outstanding revenue growth over the same time period, which indicates that earnings is driven by top-line activity rather than purely unsustainable cost-reduction initiatives. DBV's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This indicates that DBV has sufficient cash flows and proper cash management in place, which is a key determinant of the company’s health. With a debt-to-equity ratio of 1.8%, DBV’s debt level is relatively low. DBV has plenty of financial flexibility, without large debt obligations to meet in the short term, as well as the headroom to raise debt should it need to in the future.

Next Steps:

For DBV Technologies, I've compiled three key aspects you should further examine:

- Historical Performance: What has DBV's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Valuation: What is DBV worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether DBV is currently mispriced by the market.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of DBV? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:DBV

DBV Technologies

A clinical-stage biopharmaceutical company, engages in the research and development of epicutaneous immunotherapy products in France.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion