Something is stirring at Carrefour (ENXTPA:CA), a global name that tends to fly under the radar unless big headlines break. While there has not been a major event driving attention this week, the stock’s latest moves might catch investors’ eyes and prompt questions about whether the market is sending a subtle signal about future prospects. Sometimes, seemingly quiet periods can be just as interesting, especially when they make us reassess what is priced into shares of a retail giant like this.

If you zoom out, Carrefour has not exactly delivered for long-term holders lately. Over the past year, its share price slipped 11%, with momentum fading further in recent months. Even so, the company posted a strong 31% jump in annual net income, suggesting improvements under the hood. Despite these shifts, the market’s mood around the stock remains cautious, reflected in both the lagging price action and muted buzz from recent news.

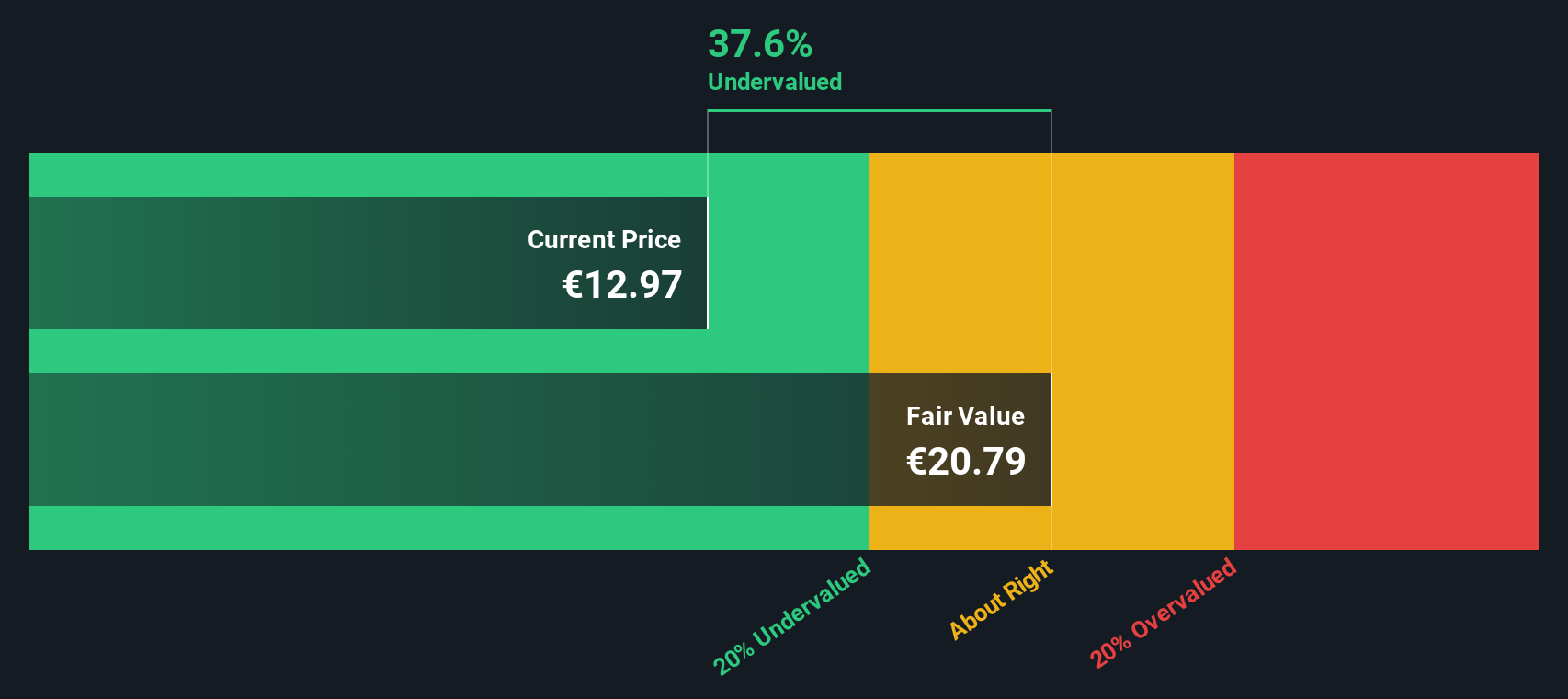

So after this year’s drop, is Carrefour a bargain hiding in plain sight, or does the stock market already see what is coming down the aisle?

Advertisement

Most Popular Narrative: 13.7% Undervalued

According to the most widely followed narrative, Carrefour appears to be undervalued by 13.7% versus its projected fair value, as calculated using a discount rate of 10.4%.

"Carrefour's digital transformation and focus on e-commerce, with an 18% growth to €6 billion in GMV, coupled with private label expansion, could drive higher margins due to the typically better profitability of online channels and private label products."

Looking for the inside track behind this valuation gap? There is a bold market assumption hidden at the heart of the narrative, with forecasts pegged on aggressive profit growth and a changed earnings structure. Want to see exactly which future milestones need to be hit and what analyst upgrades are driving the story? Do not miss the full breakdown of this valuation thesis. Discover which pivotal company shifts support these optimistic numbers.

However, ongoing competition in Europe and weak French market demand mean Carrefour could still face pressure on margins and overall profitability in the future.

While analysts argue Carrefour is undervalued based on future earnings expectations, our DCF model also suggests the shares might be trading below their intrinsic worth. However, this method raises the question of whether it fully accounts for the risks and momentum shifts that markets observe.

If you are not convinced by the prevailing narrative or want to dig into the numbers yourself, it only takes a few minutes to craft your own perspective. Do it your way.

Do not let standout opportunities pass you by. Expand your watchlist with stocks showing robust fundamentals, rising trends, or future-ready potential using these powerful screeners:

Unlock potential gains by focusing on profitable up-and-comers with penny stocks with strong financials already proving their financial strength on the market’s toughest stage.

Accelerate your search for tomorrow’s winners by targeting AI penny stocks at the forefront of artificial intelligence innovation and industry disruption.

Maximize value by zeroing in on hidden gems with undervalued stocks based on cash flows spotlighting companies whose cash flows suggest real upside many have overlooked.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.