Nokia Oyj (HLSE:NOKIA) shares have seen significant movement over the past month, gaining 41%. Investors may be taking notice of the company’s improving financials, including steady revenue growth and a surge in annual net income.

After a standout 40.6% one-month share price return, Nokia Oyj is grabbing attention again as momentum ramps up. The company is building on both steady fundamentals and renewed investor interest. The company’s 1-year total shareholder return sits at 43.1%, with a 5-year total return of 111.2%, highlighting a powerful longer-term performance recovery.

With shares climbing so quickly, the key question is whether Nokia Oyj’s recent gains leave room for further upside or if the market has already priced in its improving business. Is there still a buying opportunity left on the table?

Advertisement

Most Popular Narrative: 12% Overvalued

At €5.93, Nokia Oyj’s share price stands well above the €5.29 fair value from the most widely-followed narrative. This gap puts market optimism and analyst calculations in sharp contrast ahead of key milestones.

Scalable operational improvements, ongoing cost discipline, and rapid integration of recent acquisitions, such as Infinera, are positioned to enhance operating leverage and expand net margins over time as revenue mix shifts towards higher-margin portfolios. Investments in innovation, such as cybersecurity, AI network solutions, and next-gen optical technology, plus expanding monetization of IP and patents, should increase Nokia's high-margin revenue streams and support overall earnings growth.

Want to see what’s driving this valuation? The secret lies in bold growth forecasts, ambitious margin goals, and some surprising future earnings assumptions. Find out which financial leaps fuel this price target and how they shape Nokia Oyj’s outlook. Dive in to analyze the catalysts powering this unusually high valuation.

However, persistent currency volatility and flat revenue in the Mobile Networks segment could challenge Nokia’s profit outlook and put current optimism to the test.

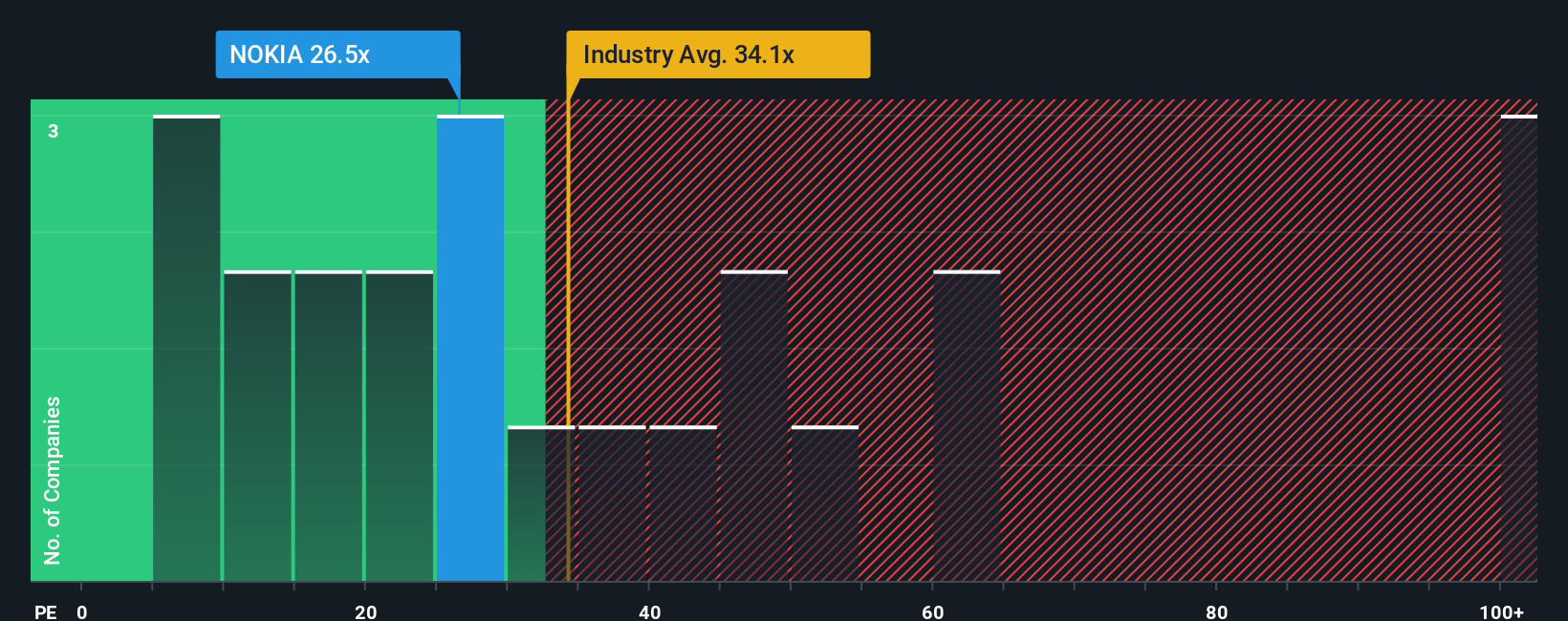

Looking at market valuation ratios offers a different perspective on Nokia Oyj. The company trades at a price-to-earnings ratio of 37.9x, just below the European Communications industry average of 38.1x and far lower than the peer average of 73.5x. However, this is still above the estimated fair ratio of 35.1x. This suggests the market might see more upside than fundamentals support and also opens room for valuation risk. Could investors be betting on Nokia’s turnaround, or are they overlooking caution signals?

Whether you see things differently or want to dig deeper into the numbers, you can shape your own view of Nokia Oyj in just minutes, your way with Do it your way.

Jump on the AI growth boom with these 26 AI penny stocks that are innovating across industries and reshaping the investing landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nokia Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Provides mobile, fixed, and cloud network solutions in North and Latin America, Greater China, India, rest of the Asia Pacific, Europe, the Middle East, and Africa.