Advertisement

- Finland

- /

- Capital Markets

- /

- HLSE:TITAN

Titanium Oyj (HEL:TITAN) Just Reported And Analysts Have Been Cutting Their Estimates

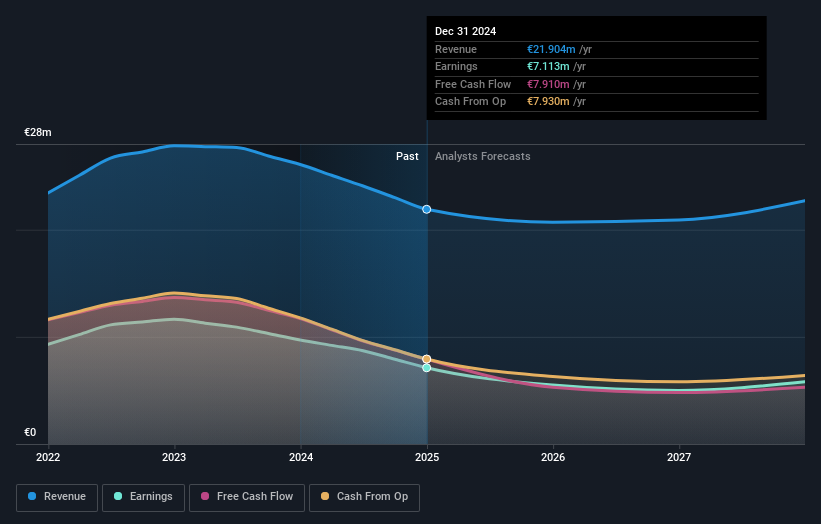

As you might know, Titanium Oyj (HEL:TITAN) recently reported its yearly numbers. It looks like the results were a bit of a negative overall. While revenues of €22m were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 2.8% to hit €0.69 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analyst is forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimate suggests is in store for next year.

See our latest analysis for Titanium Oyj

After the latest results, the consensus from Titanium Oyj's one analyst is for revenues of €20.7m in 2025, which would reflect a measurable 5.5% decline in revenue compared to the last year of performance. Before this earnings report, the analyst had been forecasting revenues of €21.9m and earnings per share (EPS) of €0.62 in 2025. Overall, while there's been a small dip in revenue estimates, the consensus now no longer provides an EPS estimate. This implies that the market believes revenue is more important following the latest results.

The average price target fell 6.3% to €7.50, withthe analyst clearly having become less optimistic about Titanium Oyj'sprospects following its latest earnings.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 5.5% by the end of 2025. This indicates a significant reduction from annual growth of 5.6% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 4.2% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Titanium Oyj is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analyst downgraded their revenue estimates for next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. The consensus price target fell measurably, with the analyst seemingly not reassured by the latest results, leading to a lower estimate of Titanium Oyj's future valuation.

One Titanium Oyj broker/analyst has provided estimates out to 2027, which can be seen for free on our platform here.

Even so, be aware that Titanium Oyj is showing 3 warning signs in our investment analysis , and 2 of those make us uncomfortable...

Valuation is complex, but we're here to simplify it.

Discover if Titanium Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:TITAN

Titanium Oyj

Provides investment and asset management services in Finland.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor