Advertisement

- Finland

- /

- Food and Staples Retail

- /

- HLSE:KESKOB

Kesko Oyj's (HEL:KESKOB) Shareholders Will Receive A Smaller Dividend Than Last Year

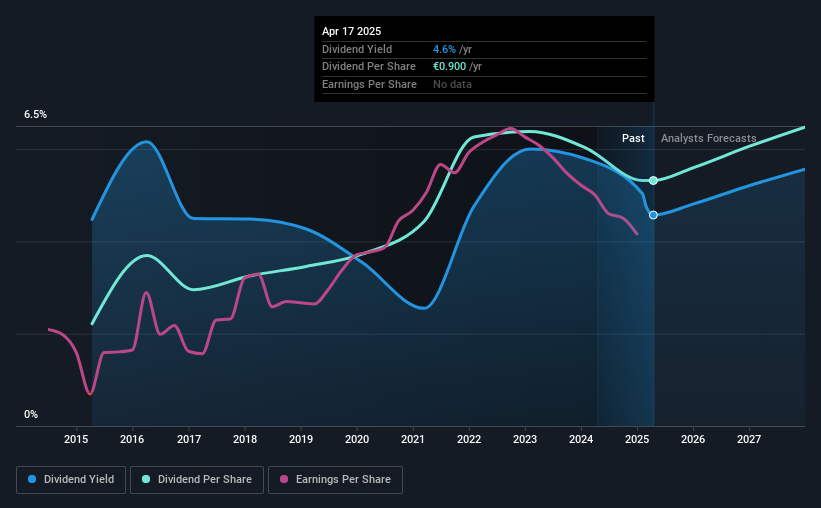

Kesko Oyj's (HEL:KESKOB) dividend is being reduced from last year's payment covering the same period to €0.22 on the 22nd of July. The dividend yield of 4.6% is still a nice boost to shareholder returns, despite the cut.

Our free stock report includes 1 warning sign investors should be aware of before investing in Kesko Oyj. Read for free now.Kesko Oyj's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, Kesko Oyj's dividend made up quite a large proportion of earnings but only 69% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

Earnings per share is forecast to rise by 47.0% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 76%, which is on the higher side, but certainly still feasible.

See our latest analysis for Kesko Oyj

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2015, the annual payment back then was €0.375, compared to the most recent full-year payment of €0.90. This implies that the company grew its distributions at a yearly rate of about 9.1% over that duration. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Kesko Oyj might have put its house in order since then, but we remain cautious.

Kesko Oyj May Find It Hard To Grow The Dividend

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Earnings per share has been crawling upwards at 2.9% per year. Earnings are not growing quickly at all, and the company is paying out most of its profit as dividends. When the rate of return on reinvestment opportunities falls below a certain minimum level, companies often elect to pay a larger dividend instead. This is why many mature companies often have larger dividend yields.

Our Thoughts On Kesko Oyj's Dividend

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 1 warning sign for Kesko Oyj that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Kesko Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:KESKOB

Kesko Oyj

Engages in the chain operations in Finland, Sweden, Norway, Estonia, Latvia, Lithuania, Denmark, and Poland.

Second-rate dividend payer and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor